Underwriting process explained: mastering risk in 2026

Over 30% of life insurance applications now leverage accelerated underwriting programmes, yet many insurance professionals still view underwriting through a traditional lens. The underwriting process has evolved dramatically, integrating predictive analytics, automation, and sophisticated data sources to balance risk selection with operational efficiency. This article clarifies modern underwriting essentials for 2026, exploring fundamental principles, technological advances, regulatory frameworks, and workflow optimisation strategies. You’ll gain actionable insights to enhance your underwriting practice and strengthen your organisation’s competitive position in an increasingly digital insurance landscape.

Table of Contents

- Understanding The Fundamentals Of Underwriting

- Modern Underwriting Practices: Automation And Data Integration

- Regulatory Framework And Risk Management Essentials In Underwriting

- Comparing Underwriting Approaches And Optimising Workflows

- Enhance Your Underwriting With IBSuite’s Claims Management

Key takeaways

| Point | Details |

|---|---|

| Underwriting balances growth and risk | Setting eligibility criteria, pricing, and terms achieves organisational growth without untenable risk exposure. |

| Automation transforms efficiency | Accelerated underwriting programmes reduce manual review time whilst maintaining accuracy through predictive models and external data integration. |

| Regulatory compliance guides decisions | NAIC valuation manual updates establish consistent standards for policy valuation, risk assessment, and pricing across the industry. |

| Workflow optimisation improves outcomes | Streamlined processes deliver faster policy issuance, better risk selection, and enhanced claims handling capabilities. |

| Data integration enhances accuracy | Combining internal historical data with external sources enables more precise risk evaluation and competitive pricing strategies. |

Understanding the fundamentals of underwriting

Underwriting forms the cornerstone of insurance risk management, serving as the critical evaluation process that determines whether to accept, modify, or decline coverage applications. At its core, underwriting involves setting eligibility criteria, pricing, documentation requirements, and terms to achieve organisational growth without untenable risk. This process directly impacts an insurer’s profitability, solvency, and market competitiveness.

The underwriting function delivers three essential outcomes. First, it establishes appropriate risk terms that reflect the true exposure level of each applicant. Second, it determines accurate pricing that covers expected claims costs whilst remaining competitive. Third, it enables informed selection decisions that build a balanced, profitable portfolio across diverse risk categories.

Effective underwriting creates a strategic balance between portfolio growth and risk management. Underwriters must evaluate applications rigorously enough to protect the insurer’s financial stability whilst approving sufficient business to meet growth targets. This balance requires deep industry knowledge, analytical skills, and understanding of both market dynamics and regulatory requirements. When executed properly, quality underwriting facilitates smooth policy issuance and simplifies claims handling by ensuring clear terms and appropriate risk classification from the outset.

Core underwriting activities encompass several interconnected responsibilities:

- Risk evaluation through comprehensive analysis of applicant information, loss history, and exposure characteristics

- Pricing determination based on actuarial models, competitive positioning, and individual risk factors

- Documentation review to verify accuracy, completeness, and compliance with regulatory standards

- Terms and conditions specification including coverage limits, exclusions, and endorsements

- Portfolio monitoring to identify emerging trends, concentration risks, and performance patterns

Modern underwriting extends beyond simple accept or reject decisions. You’ll often negotiate terms, recommend risk improvements, and collaborate with agents, brokers, and policyholders to structure coverage that meets needs whilst maintaining acceptable risk levels. Understanding insurance underwriting types helps you apply appropriate evaluation methods across different lines of business.

Modern underwriting practices: automation and data integration

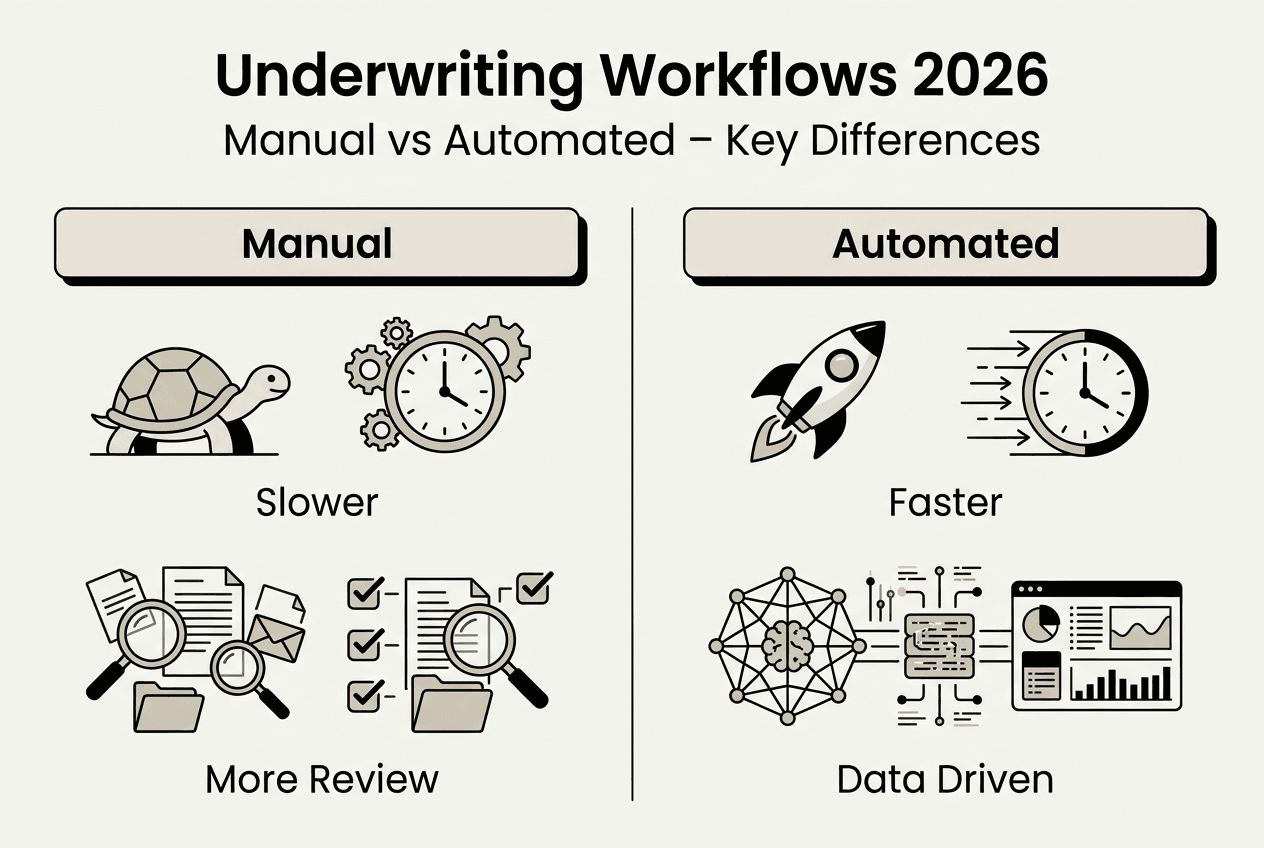

Technological advances have fundamentally transformed how insurers evaluate and price risk in 2026. Accelerated underwriting represents one of the most significant innovations, with 30% of life insurance applications now processed through programmes that integrate predictive models to reduce manual review requirements and eliminate traditional medical examinations for qualified applicants.

Predictive analytics leverage vast datasets to identify patterns and correlations that human underwriters might miss. These systems analyse historical claims data, demographic information, credit scores, prescription histories, and other relevant factors to generate risk scores and recommendations. Machine learning algorithms continuously improve accuracy by learning from outcomes, enabling more precise risk classification over time.

Data integration has become crucial for competitive advantage. Leading insurers combine internal historical data with external sources including motor vehicle records, property databases, weather patterns, and social media indicators. This comprehensive view enables more nuanced risk assessment and identifies opportunities for favourable pricing on lower risk applicants who might appear average under traditional evaluation methods.

| Aspect | Manual underwriting | Automated underwriting |

|---|---|---|

| Processing speed | Days to weeks for complex cases | Minutes to hours for most applications |

| Data sources | Limited to application and basic reports | Comprehensive integration of multiple databases |

| Consistency | Varies by underwriter experience and judgement | Standardised rules applied uniformly |

| Scalability | Requires proportional staff increases | Handles volume spikes without additional resources |

| Cost per policy | Higher due to labour intensity | Significantly reduced operational expenses |

| Flexibility | Easily adapts to unique situations | Requires rule updates for exceptions |

The shift towards automated underwriting doesn’t eliminate the need for human expertise. Complex cases, unusual risks, and high-value policies still benefit from experienced underwriter review. The optimal approach combines automation’s efficiency and consistency with human judgement for nuanced decision making.

AI in P&C insurance extends beyond initial underwriting to continuous risk monitoring throughout the policy lifecycle. Advanced systems flag changes in risk profiles, identify cross-selling opportunities, and recommend proactive risk management interventions that reduce claims frequency and severity.

Pro Tip: When integrating new data sources into your underwriting process, start with a parallel testing phase where automated recommendations run alongside traditional methods. Compare outcomes over several months to validate accuracy before fully transitioning, ensuring you maintain underwriting quality whilst gaining efficiency benefits.

Regulatory framework and risk management essentials in underwriting

Regulatory compliance forms a non-negotiable foundation for sound underwriting practice. The NAIC’s Valuation Manual has been updated annually with amendments through 2025, providing comprehensive guidance on policy valuation consistent with regulatory standards that directly influence underwriting decisions across all insurance lines.

These regulatory frameworks impact every aspect of the underwriting process. Eligibility criteria must align with anti-discrimination laws whilst allowing appropriate risk differentiation. Pricing structures need actuarial justification and often require regulatory approval before implementation. Documentation requirements ensure transparency and enable regulatory examination of underwriting practices.

The valuation manual particularly affects life and annuity underwriting through principle-based reserving requirements. These standards mandate that insurers hold reserves reflecting the actual risk characteristics of their portfolios rather than applying uniform formulas. Underwriters must therefore consider not just immediate profitability but also long-term capital requirements when evaluating applications and setting terms.

Key risk management considerations in underwriting include:

- Portfolio concentration limits to prevent excessive exposure to single risks, geographic areas, or industry sectors

- Reinsurance programme alignment ensuring underwriting guidelines support treaty terms and retention strategies

- Emerging risk identification including climate change impacts, cyber exposures, and evolving liability trends

- Quality control processes with regular file reviews, audit trails, and performance metrics tracking

- Regulatory reporting accuracy to maintain compliance and avoid penalties or market conduct issues

Effective risk management extends beyond individual policy decisions to portfolio-level strategy. You need visibility into aggregate exposures, correlation risks, and potential accumulation scenarios that could threaten solvency during catastrophic events. Modern underwriting systems provide dashboards and analytics tools that enable real-time monitoring of these portfolio characteristics.

Regulatory compliance in underwriting isn’t merely about avoiding penalties. It establishes the foundation for sustainable business practices, protects policyholders, and maintains market stability. Insurers that view compliance as a competitive advantage rather than a burden position themselves for long-term success.

Understanding insurance product management helps you recognise how underwriting guidelines must evolve alongside product development to maintain profitability whilst meeting market demands. Regulatory frameworks provide guardrails that enable innovation within acceptable risk parameters.

Comparing underwriting approaches and optimising workflows

Selecting the appropriate underwriting approach depends on your business objectives, risk appetite, and operational capabilities. Different scenarios call for varying levels of automation, data integration, and human oversight to achieve optimal results.

| Feature | Traditional manual approach | Hybrid approach | Fully automated approach |

| — | — | — |

| Best suited for | Complex commercial risks, high-value policies | Standard policies with exception handling | High-volume personal lines |

| Decision speed | Slowest but most thorough | Balanced efficiency and oversight | Fastest processing times |

| Underwriter role | Primary decision maker | Exception handler and quality reviewer | System designer and monitor |

| Technology requirements | Basic systems for documentation | Integrated platforms with workflow tools | Advanced AI and predictive analytics |

| Adaptability to change | Highly flexible for unique situations | Moderate with rule updates | Requires significant system modifications |

Optimising your underwriting workflows requires systematic evaluation and continuous improvement. Follow these steps to enhance efficiency whilst maintaining accuracy:

- Map current processes to identify bottlenecks, redundancies, and opportunities for automation or elimination of non-value-adding activities.

- Establish clear performance metrics including processing time, accuracy rates, loss ratios by underwriter, and customer satisfaction scores.

- Implement tiered authority levels enabling straight-through processing for low-risk applications whilst reserving senior underwriter review for complex cases.

- Integrate data sources to eliminate manual data entry, reduce errors, and provide underwriters with comprehensive information at initial review.

- Create feedback loops connecting claims outcomes to underwriting decisions, enabling continuous learning and guideline refinement.

- Invest in training programmes ensuring underwriters understand both technological tools and fundamental risk evaluation principles.

Optimising underwriting workflows delivers multiple benefits beyond speed improvements. Better risk selection reduces claims costs and improves combined ratios. Accurate pricing enhances competitiveness on desirable risks whilst ensuring adequate premium on higher exposures. Faster processing improves customer experience and agent satisfaction, supporting business retention and growth.

The concept that well-executed underwriting leads to smooth policy issuance and easier claims handling emphasises the downstream impacts of quality underwriting work. Clear terms, appropriate coverage limits, and accurate risk classification prevent disputes during claims and reduce the likelihood of coverage gaps that disappoint policyholders.

Pro Tip: Monitor your straight-through processing rate as a key performance indicator. If this metric drops, investigate whether guidelines need updating, data quality has declined, or submission quality from distribution partners requires attention. Regular analysis of exception reasons reveals opportunities for rule refinement.

Adopting underwriting best practices positions your organisation to adapt quickly as market conditions, regulatory requirements, and competitive dynamics evolve. Flexibility built into your processes and systems enables rapid response without compromising risk management principles.

Enhance your underwriting with IBSuite’s claims management

Transforming underwriting insights into operational excellence requires integrated technology that connects risk evaluation, policy administration, and claims handling. IBSuite’s claims management solution provides underwriting teams with real-time visibility into claims patterns, enabling data-driven guideline refinements and more accurate risk assessment. The platform streamlines workflows through automated routing, comprehensive documentation, and regulatory compliance tracking that reduces administrative burden whilst improving accuracy.

Key benefits include enhanced risk selection through claims analytics integration, faster processing times with straight-through capabilities for qualifying submissions, and seamless collaboration between underwriting and claims teams. The cloud-native architecture ensures your systems scale effortlessly as volume grows, whilst API-first design enables integration with existing data sources and third-party tools.

Experience how IBSuite transforms underwriting operations by exploring the platform’s capabilities firsthand. Book a demo to see how leading insurers leverage integrated technology to accelerate digital transformation, reduce IT complexity, and achieve competitive advantage through superior underwriting performance.

FAQ

What is accelerated underwriting and how does it work?

Accelerated underwriting uses predictive models and external data sources to evaluate risk without traditional medical examinations or lengthy manual reviews. 30% of life insurance applications now process through these programmes, which analyse prescription histories, motor vehicle records, credit data, and other indicators to generate risk scores. Qualified applicants receive instant or same-day decisions, dramatically improving customer experience whilst maintaining accurate risk classification.

How does the NAIC valuation manual affect underwriting decisions?

The NAIC’s valuation manual establishes regulatory standards for policy valuation that directly influence underwriting guidelines, particularly for life and annuity products. Principle-based reserving requirements mean underwriters must consider long-term capital implications, not just immediate profitability, when evaluating applications. These standards ensure solvency protection whilst enabling appropriate risk differentiation and competitive pricing within regulatory frameworks.

What are the main benefits of optimising underwriting workflows?

Optimised workflows deliver improved risk selection through better data integration and consistent application of guidelines, leading to lower loss ratios and enhanced profitability. Processing speed increases dramatically, with many standard applications receiving same-day decisions rather than week-long reviews. Well-executed underwriting leads to smooth policy issuance and easier claims handling by establishing clear terms and appropriate coverage from the outset.

How do underwriters balance automation with human judgement?

Successful underwriting programmes use automation for routine decisions whilst reserving human expertise for complex cases, unusual risks, and high-value policies. Tiered authority structures enable straight-through processing for low-risk applications that meet predefined criteria, freeing experienced underwriters to focus on nuanced situations requiring judgement. Regular monitoring of automated decisions ensures accuracy, with feedback loops enabling continuous improvement of rules and algorithms based on actual outcomes.

What data sources improve underwriting accuracy in 2026?

Modern underwriting integrates internal historical claims data with external sources including credit bureaus, motor vehicle records, property databases, prescription histories, and weather pattern analytics. Telematics data from connected devices provides real-time risk insights for motor insurance, whilst IoT sensors in properties enable proactive risk management for homeowners coverage. Social media and public records offer additional context for complex commercial risks, though privacy regulations govern appropriate use of these sources.