Why scalable insurance platforms matter for growth

Insurers across Central Europe are sitting on a problem that gets more expensive every year. 90% of current operating models do not support future business needs, with inadequate infrastructure and lack of scalability cited as the primary constraints. A scalable insurance platform is one that handles growing volumes of policies, claims, and data without degrading performance or requiring a complete system rebuild each time the business expands. The benefits are concrete and measurable:

- Faster product launches and shorter time-to-market cycles

- Lower IT costs through reusable components and cloud economics

- Real-time data access for contact centre operators and underwriters

- Compliance with regulations such as GDPR, DORA, and IVASS requirements

- Consistent customer experience across digital and traditional channels

- Geographic and product-line expansion without proportional cost increases

Trusted platforms such as IBSuite, built by Ibapplications, and the architecture adopted by Helvetia Italy Group demonstrate what these benefits look like in practice. The rest of this article explains how they are achieved, what can go wrong, and what the evidence from European insurers actually shows.

What does scalability really mean in insurance systems?

Scalability in insurance is the ability of a platform to handle more work, more products, and more users without a drop in reliability or speed. That sounds straightforward, but the insurance context makes it genuinely complex. A single policy administration system may need to process renewals, mid-term adjustments, claims notifications, and regulatory reports simultaneously, across multiple product lines and jurisdictions.

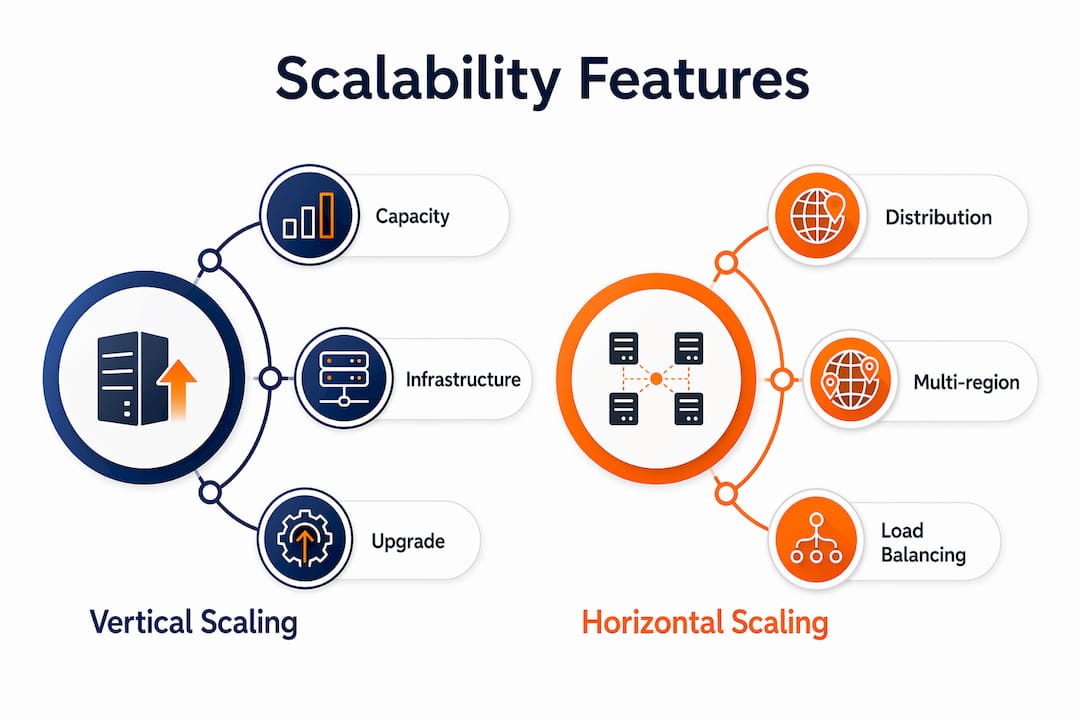

There are two dimensions worth separating. Vertical scalability means upgrading the capacity of existing infrastructure, adding processing power or memory to handle heavier loads. Horizontal scalability means adding more instances of a service in parallel, so the system distributes load rather than concentrating it. Cloud-native platforms favour horizontal approaches because they are more cost-efficient and more resilient under sudden demand spikes.

The business implications go beyond raw throughput. A platform that cannot scale forces insurers into maintenance windows, restricts channel expansion, and slows the launch of new products. Helvetia Italy Group experienced this directly: before modernising, integrating a new channel took 6–9 months. After adopting a cloud-native architecture, that time-to-market was reduced by 30%.

Key attributes that define a genuinely scalable insurance platform:

- Modular architecture that allows individual components to be updated independently

- API-first design enabling integration with external partners and distribution channels

- Cloud deployment that adjusts capacity automatically to match demand

- Event-driven processing that handles real-time data flows without bottlenecks

- Multi-jurisdiction support covering different regulatory and currency requirements

Which architectural features actually enable platform scalability?

The architecture underneath a platform determines whether scalability is real or just a marketing claim. Three patterns consistently appear in platforms that deliver on the promise.

Microservices design breaks the platform into small, independently deployable services. Each service handles a specific function, such as rating, claims intake, or billing, and can be scaled, updated, or replaced without touching the rest of the system. This is the opposite of the monolithic architecture that still underpins many legacy core systems, where a change to one module risks destabilising everything else.

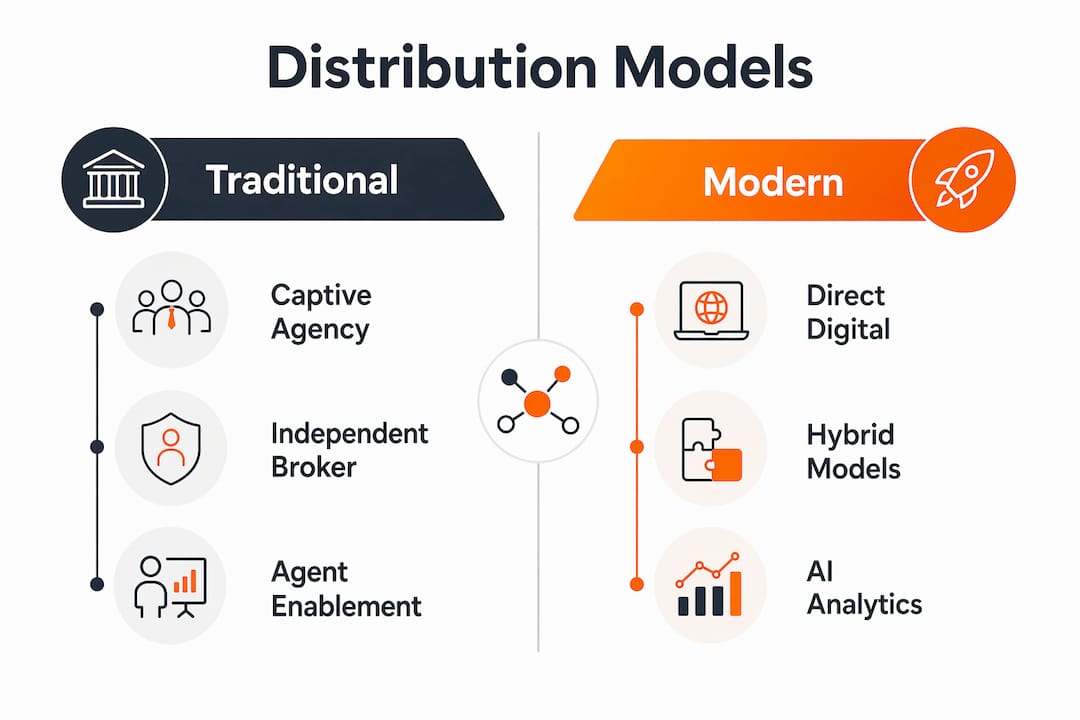

API-first strategy treats every function as an accessible service. External partners, digital channels, and internal tools all connect through documented APIs rather than bespoke point-to-point integrations. Cloud-native and API-first platforms enable flexible integration, real-time data access, and modular updates. Helvetia Italy Group’s implementation exposed customer data, policies, claims, and payments through dedicated APIs, making that information immediately available to every touchpoint.

Event-driven architecture processes data as events occur rather than in scheduled batches. This is what enables sub-second response times. Helvetia achieved data refresh times of under 2 seconds for contact centre operators, compared with the overnight batch cycles common in legacy environments.

Additional architectural features that support scalability:

- Data fabric layers that aggregate information from multiple source systems into unified views

- Security-by-design using standards such as OpenID and OAuth2

- Packaged Business Capabilities (PBCs) that can be assembled into new products without custom development

- Evergreen update mechanisms that keep the platform current without disruptive upgrade projects

- Built-in compliance tooling for GDPR, DORA, and NIS2 requirements

Pro Tip: When evaluating a platform’s architecture, ask specifically whether microservices are independently deployable and whether the API catalogue is versioned. A platform that bundles all services into a single release cycle is not truly modular, regardless of how it is described in vendor documentation.

How do vertical and horizontal scalability affect insurance operations?

The choice between vertical and horizontal scaling has direct consequences for how an insurer can grow. Vertical scaling is simpler to implement initially but hits a ceiling. At some point, a single server or database instance cannot be made large enough to handle the load, and the cost of each incremental upgrade rises steeply. Horizontal scaling distributes the work across many instances, which is why cloud platforms built on AWS or equivalent infrastructure can handle traffic spikes during renewal seasons or catastrophe events without degrading service.

For insurers expanding geographically across Central Europe, horizontal scalability is particularly relevant. Adding a new country or distribution partner does not require a separate system build. The platform adds capacity and configuration for the new market while the existing infrastructure continues to serve other regions.

The Helvetia Italy Group case illustrates both dimensions. The insurer needed to comply with IVASS Regulation 41/2018 while simultaneously launching new digital products. A vertically scaled legacy system could not have absorbed both demands without significant disruption. The Digital Integration Hub approach allowed Helvetia to add new channels and meet regulatory requirements concurrently, completing 8 new channel integrations over two years.

Key business impacts of scalability by type:

- Horizontal: supports geographic expansion, multichannel distribution, and partner onboarding without proportional cost increases

- Vertical: useful for short-term capacity increases but creates single points of failure and cost unpredictability

- Combined cloud approach: hybrid and multi-cloud strategies deliver an average 4.15% revenue benefit for European insurers

Pro Tip: For insurers operating across multiple Central European markets, prioritise platforms that support multi-jurisdiction configuration natively rather than through separate instances. Managing five country deployments as five separate systems eliminates most of the cost and speed advantages that scalability is supposed to deliver.

What challenges do insurers face when implementing scalable platforms?

Legacy system integration is the most common obstacle. Most established European insurers run core systems that were built decades ago, often with proprietary database logic and no API layer. Connecting a modern scalable platform to these backends without disrupting live operations requires careful architecture. 84% of insurers prioritise automation and integration when transforming core systems, which reflects how central this challenge is.

The Digital Integration Hub (DIH) pattern addresses this directly. Rather than replacing legacy systems immediately, a DIH sits between old and new, decoupling front-end channels from backend complexity. Helvetia Italy Group deployed its DIH within the required six months, with the legacy portfolio systems remaining in place while the new layer handled all channel interactions. This approach enables rapid deployment within 6 months with low operational risk.

Cost and organisational complexity are the other two significant hurdles. Cloud migration and platform modernisation require sustained investment, and 100% of European insurers expect IT costs to increase over the next three years. Managing that investment while maintaining business continuity demands close collaboration between IT and business units.

Risks and mitigating practices:

- Legacy integration risk: use a DIH to decouple new services from existing backends before decommissioning

- Cost overrun: adopt phased deployment with defined milestones and reusable component libraries

- Regulatory complexity: choose platforms with built-in compliance tooling for GDPR, DORA, and NIS2

- Organisational resistance: involve business stakeholders from the outset, not just IT teams

- Vendor lock-in: prioritise open API standards and avoid proprietary data formats

Smaller European insurers tend to navigate these challenges more quickly. Smaller insurers adopting SaaS report fewer internal bottlenecks and less process duplication than their larger counterparts, partly because they carry less legacy complexity and can commit to a single platform strategy without managing competing internal systems.

What do real results from Central European insurers look like?

The Helvetia Italy Group implementation is the most thoroughly documented example of scalable platform benefits in the Central European market. The outcomes are specific enough to be useful as benchmarks.

The measurable results from that programme:

- A 30% reduction in time-to-market for new commercial products and services

- A notable reduction in average project costs through asset reuse from the platform catalogue

- Data refresh time below 2 seconds via Single Customer Views, down from near-real-time targets of under 10 seconds

- Over 4 million customers aggregated within unified Single Views

- 9 AI use cases implemented across Claims, Non-Life, and Life sectors once the platform was AI-ready

- 24/7 system availability achieved, replacing maintenance windows that previously caused weekend and overnight outages

European insurers using hybrid cloud strategies report measurable revenue benefits from cloud adoption. When combined with AI and robotic process automation applied to claims administration and underwriting, the operational gains compound further. The digital insurance platform market is forecast to reach USD 156–329 billion in premium revenue by 2028–2029, which reflects how central platform ecosystems are becoming to insurer growth strategies.

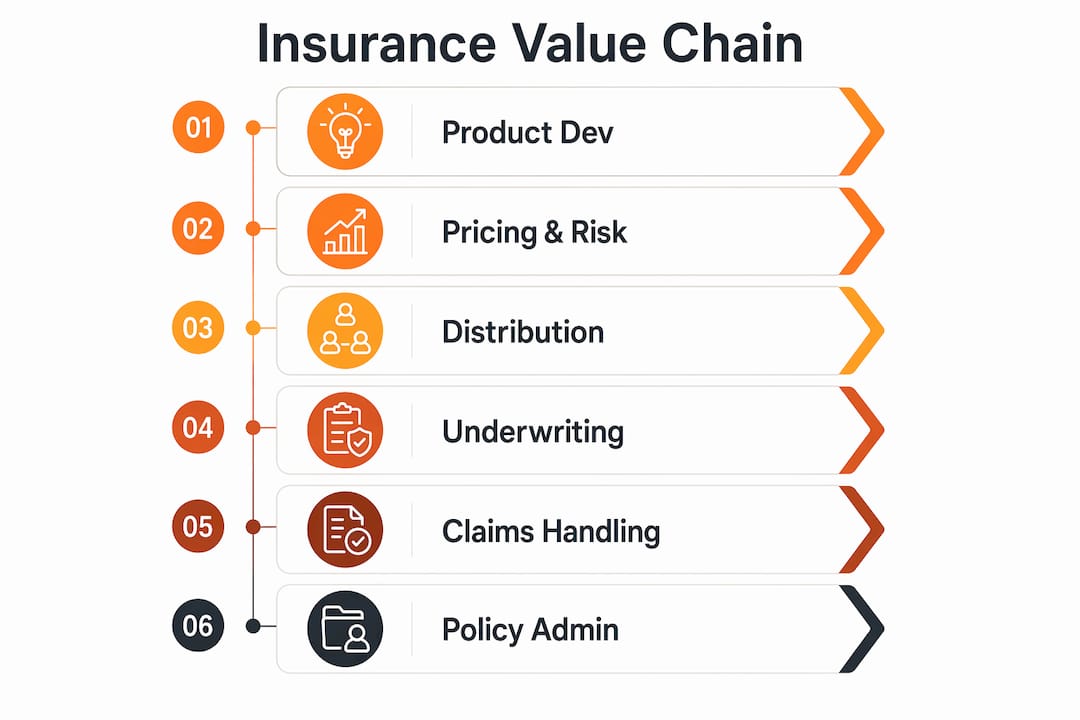

IBSuite, the platform built by Ibapplications, supports the full insurance value chain including policy administration, claims, billing, rating, and CRM. It is built on AWS and designed to deliver the same architectural properties that produced Helvetia’s results: API-first design, microservices, and Evergreen updates that keep the platform current without disruptive upgrade cycles.

How do scalable platforms support regulatory compliance in Central Europe?

Regulatory pressure in Central Europe is intensifying. EIOPA’s digitalisation report identifies the Artificial Intelligence Act, the Digital Operational Resilience Act (DORA), and the Financial Data Act as frameworks that will reshape how insurers build and operate their technology. Platforms that treat compliance as an afterthought create significant risk; those that build it into the architecture reduce it to a configuration exercise.

DORA, which applies directly to insurers operating in EU markets, requires demonstrable operational resilience, incident reporting, and third-party risk management. A microservices platform with independent service deployment can isolate a failing component without taking down the entire system, which is exactly the kind of resilience DORA demands. Helvetia Italy Group’s implementation achieved drastic reductions in compliance times for GDPR, DORA, and NIS2 through its microservices infrastructure.

Data security follows the same logic. Security-by-design, using OpenID and OAuth2 protocols, means access controls are standardised across every service rather than implemented inconsistently across a patchwork of legacy modules. For insurers handling sensitive personal data across multiple Central European jurisdictions, that consistency is not optional.

The benefits of cloud-native insurance extend to audit trails and reporting. Cloud platforms log every transaction and configuration change automatically, which simplifies the evidence gathering that regulators increasingly require. Insurers still running on-premise systems often spend weeks assembling audit data that a cloud-native platform can produce in hours. Understanding how digital transformation drivers interact with compliance requirements is increasingly a prerequisite for technology leaders in the region.

IBSuite by Ibapplications: built for insurers who need to grow

Ibapplications has been building cloud-native insurance platforms since 2010, and IBSuite reflects that experience directly. For P&C insurers in Central Europe facing the combination of legacy debt, regulatory pressure, and growth ambitions, IBSuite offers a concrete path forward rather than a theoretical one.

The platform covers the full value chain: policy administration, underwriting, claims, billing, rating, CRM, and financial sub-ledger, all within a single API-first architecture built on AWS. Evergreen updates mean the platform stays current with regulatory changes without requiring disruptive upgrade projects. Insurers can launch new products faster, connect new distribution channels without months of integration work, and expand into new markets without rebuilding their core systems.

For decision-makers evaluating options, the practical question is whether a platform can deliver the kind of results Helvetia Italy Group achieved, at a pace and cost that fits your organisation. Book a demo with Ibapplications to see how IBSuite maps to your specific growth and compliance requirements.

FAQ

What are scalable insurance platforms?

Scalable insurance platforms are cloud-native core systems that handle growing volumes of policies, claims, and data without performance degradation. They use microservices, API-first design, and event-driven architecture to support product expansion, geographic growth, and regulatory compliance simultaneously.

What is the benefit of digital transformation for insurance companies?

Digital transformation reduces time-to-market for new products, lowers operational costs through automation, and improves customer experience through real-time data access. Helvetia Italy Group achieved a 30% reduction in time-to-market and a notable reduction in average project costs after modernising its core platform.

How does DORA affect insurance platform requirements in Central Europe?

DORA requires insurers to demonstrate operational resilience, manage third-party technology risk, and report incidents to regulators. Cloud-native platforms with microservices architecture meet these requirements more readily than monolithic legacy systems, because individual services can fail and recover without system-wide outages.

Why do smaller European insurers adopt scalable platforms faster?

Smaller insurers carry less legacy complexity and fewer competing internal systems, which means they can commit to a SaaS or cloud-native platform strategy more quickly. Research on EU insurers shows they report fewer internal bottlenecks and less process duplication than larger counterparts once they make the transition.

What is an API-first insurance platform?

An API-first platform exposes every function, including policy data, claims status, and billing, through documented APIs. This allows insurers to connect new distribution channels, partner systems, and digital products without bespoke integrations, reducing channel onboarding from months to weeks.

Key takeaways

Scalable insurance platforms are the single most important infrastructure decision for European insurers seeking growth, because inadequate scalability is the primary reason 90% of current operating models cannot support future business needs.

| Point | Details |

|---|---|

| Scalability drives growth | Most EU insurers report their current operating models cannot support future business needs due to infrastructure and scalability gaps. |

| Architecture determines outcomes | Microservices, API-first design, and event-driven processing are the features that make scalability real rather than theoretical. |

| Helvetia Italy Group benchmark | A 30% time-to-market reduction and data refresh times below 2 seconds show what a well-implemented scalable platform delivers. |

| Compliance is built in, not bolted on | Cloud-native platforms with security-by-design reduce GDPR, DORA, and NIS2 compliance times significantly compared with legacy approaches. |

| Ibapplications IBSuite | IBSuite provides an API-first, AWS-built platform covering the full P&C value chain, designed for European insurers modernising core systems. |

Recommended

- Insurance Platform Scalability Explained: Key Success Factors – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Cloud Scalability in Insurance: Enabling Rapid Growth

- Modern Insurance Platforms: What to look for – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Modern Insurance Platform Benefits – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System