19.03.26

What is insurance billing in P&C? A clear 2026 guide

Insurance billing in property and casualty insurance is more than sending invoices. It transforms policies into revenue whilst ensuring compliance across multiple jurisdictions. For billing specialists and financial managers, mastering this process means balancing complex premium calculations, payment reconciliations, and regulatory requirements. This guide clarifies the core mechanics, technologies, challenges, and financial impacts of insurance billing in P&C. You’ll discover how modern automation reshapes workflows, why payment failures occur, and how effective billing drives profitability. Whether you’re optimising current systems or evaluating new platforms, this roadmap delivers practical insights for 2026 and beyond.

Table of Contents

- Understanding Insurance Billing In Property And Casualty Insurance

- Technologies And Automation Transforming Insurance Billing

- Key Challenges And Nuanced Considerations In P&C Insurance Billing

- The Impact Of Insurance Billing On Profitability And Financial Management

- Discover Modern Insurance Billing Solutions

Key takeaways

| Point | Details |

|---|---|

| Billing converts policies into revenue | Insurance billing encompasses premium calculation, invoicing, payment processing, and reconciliation to turn policies into paid premiums. |

| Technology drives efficiency | Modern platforms automate workflows, reduce manual errors, and integrate with policy administration systems for seamless operations. |

| Challenges require expert handling | Legacy systems, regulatory variations, complex endorsements, and payment failures demand precise management and real-time analytics. |

| Effective billing supports profitability | Streamlined billing improves cash flow predictability, controls expense ratios, and helps maintain combined ratios under 100%. |

| Self-service portals enhance recovery | Customer portals and automated workflows improve payment recovery rates and strengthen retention through better experiences. |

Understanding insurance billing in property and casualty insurance

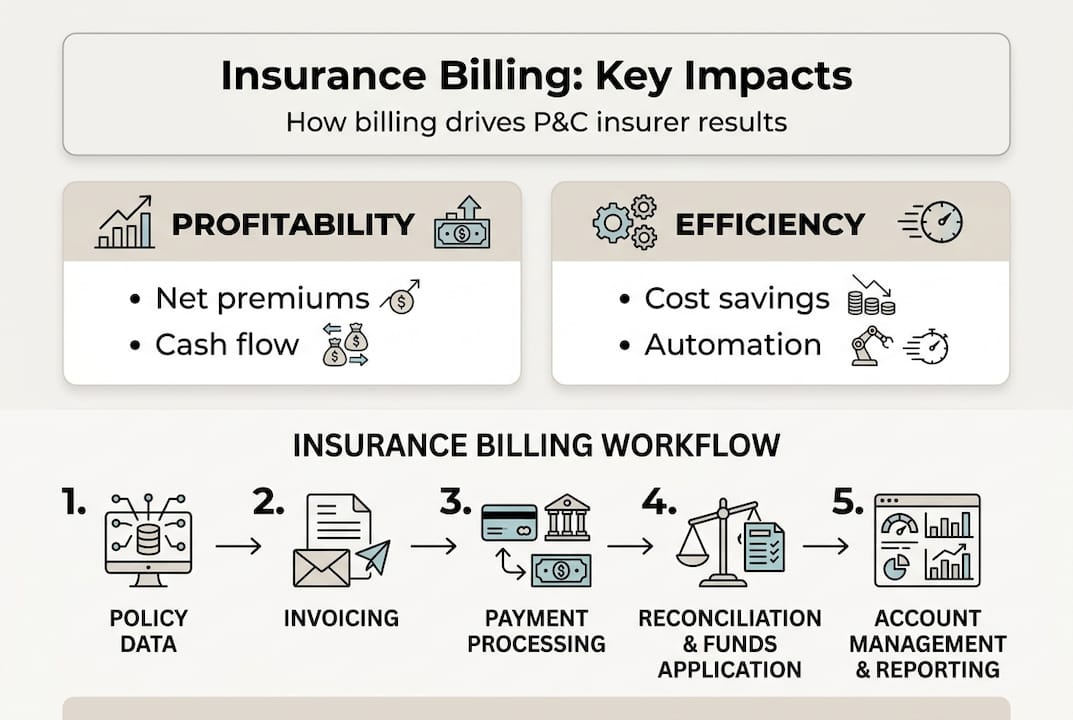

Insurance billing in property and casualty insurance is the process of calculating, generating, delivering invoices for premiums, processing payments, reconciling records, and handling follow-ups to convert policies into paid premiums whilst ensuring regulatory compliance and revenue recognition. This definition captures the full scope of what billing specialists manage daily. The insurance billing process for P&C insurers involves multiple interconnected steps that must execute flawlessly to maintain revenue flow and compliance.

The billing cycle comprises seven core steps that transform underwritten policies into collected premiums. First, premium calculation determines the amount owed based on policy terms, coverage limits, and rating factors. Second, invoice generation creates formal billing documents with payment terms and due dates. Third, bill delivery sends invoices through postal mail, email, or customer portals. Fourth, payment initiation occurs when policyholders submit payments via cheque, electronic transfer, or automatic deduction. Fifth, payment authorisation validates funds availability and processes the transaction. Sixth, payment posting updates policy records and financial ledgers. Seventh, reconciliation matches payments to invoices and identifies discrepancies requiring follow-up.

Each step integrates compliance checkpoints and revenue recognition rules. Billing systems must track premium earned versus premium written, applying accounting standards that recognise revenue over policy periods. Regulatory requirements vary by jurisdiction, affecting notice periods, cancellation procedures, and refund calculations. Statutory accounting principles govern how insurers report premium income, with billing data feeding directly into financial statements and regulatory filings.

Turning policies into paid premiums directly impacts company cash flow and operational stability. Delays in any billing step create revenue timing gaps that affect loss ratio calculations and investment income projections. Precise management of each phase prevents premium leakage, where uncollected amounts erode profitability. Billing specialists must coordinate with underwriting, claims, and finance teams to ensure data accuracy across systems.

Challenges emerge at every stage, requiring vigilant oversight. Premium calculations grow complex with mid-term endorsements that adjust coverage and rates. Invoice generation must accommodate instalment plans, down payments, and agency commission structures. Payment processing encounters failed transactions, insufficient funds, and disputed charges. Reconciliation identifies posting errors, duplicate payments, and unapplied cash that demands investigation. These operational realities make billing far more intricate than simple invoicing.

Technologies and automation transforming insurance billing

Modern technologies supporting P&C billing include core billing platforms, policy and billing integration, recurring billing and autopay, payments infrastructure, customer self-service portals, automation and workflow engines, reconciliation and financial controls, analytics and reporting, and security and fraud controls. These tools work together to streamline operations and reduce manual interventions. Core billing platforms serve as the central hub, managing premium schedules, instalment plans, and payment tracking across thousands of policies simultaneously.

Integration with policy administration systems ensures billing data remains synchronised with coverage changes, endorsements, and cancellations. When underwriters modify policy terms, billing systems automatically recalculate premiums and generate adjusted invoices. This real-time connectivity eliminates the lag that legacy systems experience, where manual data entry creates delays and errors. Modern insurance platforms features include API-first architectures that enable seamless data flow between billing, policy, claims, and financial modules.

Automation transforms premium calculation, invoicing, and reconciliation steps that previously consumed hours of manual work. Workflow engines trigger invoice generation based on policy effective dates, send payment reminders before due dates, and escalate overdue accounts through defined collection sequences. Automated reconciliation matches incoming payments to outstanding invoices, posts transactions to correct accounts, and flags exceptions for human review. Insurance billing automation benefits extend beyond speed, improving accuracy by eliminating transcription errors and calculation mistakes.

Customer self-service portals revolutionise bill delivery and payment collection. Policyholders access current balances, view payment history, download invoices, and submit payments without contacting service representatives. These portals support multiple payment methods, including credit cards, bank transfers, and digital wallets. Self-service reduces operational costs whilst improving customer satisfaction through 24/7 access and instant payment confirmation.

Recurring billing and autopay features reduce missed payments and manual processing overhead. Policyholders authorise automatic deductions from bank accounts or credit cards, ensuring premiums are collected on schedule without intervention. Systems handle payment retries when initial attempts fail, applying intelligent logic to optimise success rates. Autopay enrolment drives payment consistency, lowering cancellation rates from non-payment.

Security and fraud controls protect sensitive billing data throughout the payment lifecycle. Encryption safeguards payment credentials, tokenisation replaces actual card numbers with secure references, and fraud detection algorithms identify suspicious transaction patterns. Compliance with payment card industry standards and data protection regulations is non-negotiable for insurers handling financial information.

Analytics and reporting provide real-time visibility into receivables, payment failure rates, and collection effectiveness. Dashboards display key metrics like days sales outstanding, payment method distribution, and autopay enrolment percentages. Predictive analytics identify accounts at risk of non-payment, enabling proactive outreach before policies lapse. These insights support data-driven decisions about collection strategies and payment plan offerings.

Pro Tip: Implement workflow automation to reduce manual interventions and payment delays. Configure rules that automatically send reminders, process standard endorsements, and escalate exceptions only when human judgement is required. This approach frees billing specialists to focus on complex cases whilst routine tasks execute flawlessly.

Key challenges and nuanced considerations in P&C insurance billing

Legacy systems cause delays and duplicates, manual interventions increase errors, regulatory variations by jurisdiction, payment failures, data visibility gaps, complex endorsements trigger recalculations, and commercial policies have multiple locations that complicate billing operations. These obstacles create operational friction that impacts revenue collection and customer satisfaction. Legacy systems often lack integration capabilities, forcing staff to manually transfer data between billing, policy, and accounting platforms. This duplication introduces transcription errors and version control problems.

Manual interventions multiply error rates, particularly during high-volume periods like renewal seasons. Staff calculating premium adjustments by hand risk misapplying rating factors or overlooking endorsement impacts. Data entry mistakes create billing disputes that require time-consuming research and correction. As transaction volumes grow, manual processes become bottlenecks that delay invoice delivery and payment posting.

Regulatory variations by region affect notice and cancellation handling in ways that demand system flexibility. Some jurisdictions require 30-day cancellation notices, others mandate 45 or 60 days. Refund calculations follow different rules depending on whether cancellations are insurer-initiated or policyholder-requested. Systems must accommodate these variations without creating compliance gaps or manual workarounds.

Complex endorsements, cancellations, and reinstatements require recalculation and precise adjustment of premium schedules. Mid-term coverage changes alter the remaining premium due, necessitating pro-rata calculations and revised instalment amounts. Cancellations trigger refund processing, whilst reinstatements demand back-premium collection and payment plan restructuring. Each scenario introduces calculation complexity that automated systems must handle accurately.

Commercial policies entail more complex billing due to multiple locations, varying exposures, and layered coverage structures. A single commercial policy might cover dozens of properties with different risk profiles, each requiring separate premium calculations. Audit provisions adjust final premiums based on actual payroll or sales figures, creating retrospective billing adjustments months after policy inception. Insurance billing process exceptions in commercial lines demand sophisticated systems and experienced specialists.

| Payment Failure Cause | Typical Resolution |

|---|---|

| Insufficient funds | Retry payment after 3-5 days, contact policyholder for alternative payment method |

| Expired payment method | Request updated card details through portal or phone, offer payment plan if needed |

| Disputed charge | Investigate billing accuracy, provide documentation, adjust invoice if error confirmed |

| Technical processing error | Resubmit transaction, verify payment gateway connectivity, escalate to IT if persistent |

| Account closed | Contact policyholder immediately, collect replacement payment details, prevent policy lapse |

Payment failures stem from multiple causes, each requiring specific recovery workflows. Insufficient funds often result from timing mismatches between policyholder cash flow and payment due dates. Expired payment methods occur when autopay relies on outdated card information. Disputed charges arise from billing errors, unclear invoice descriptions, or policyholder confusion about coverage changes. Technical processing errors reflect payment gateway issues or system integration problems. Account closures happen when policyholders change banks without updating payment information.

Data visibility gaps prevent billing teams from accessing real-time information about payment status, outstanding balances, and collection progress. Siloed systems create situations where billing staff cannot see recent policy changes that affect premium calculations. Lack of integrated dashboards forces manual report compilation, delaying decision-making and problem identification.

Pro Tip: Prioritise payment failure recovery workflows and real-time analytics to improve cash flow and customer retention. Configure automated retry logic that attempts collection at optimal times, send targeted communications explaining failure reasons, and offer flexible payment solutions before policies lapse. Analytics identifying failure patterns enable proactive system improvements and policyholder education.

The impact of insurance billing on profitability and financial management

Billing supports net premiums written and cash flow predictability by ensuring policies convert to collected revenue on schedule. Net premiums written reached $934 billion in 2024, with efficient billing processes directly influencing this figure. Timely premium collection accelerates cash flow, enabling insurers to invest funds sooner and generate additional income. Predictable billing cycles allow financial managers to forecast revenue with confidence, supporting accurate budgeting and strategic planning.

Maintaining combined ratios under 100% is essential for profitability, with the industry achieving 96.9% in 2024. The combined ratio measures total losses and expenses against earned premiums, with figures below 100% indicating underwriting profit. Billing efficiency directly impacts this metric by controlling expense ratios and minimising premium leakage from uncollected accounts. Every pound of premium that goes uncollected due to billing failures increases the combined ratio and erodes profitability.

Expense ratio control through automation and efficient billing reduces operational costs significantly. The industry expense ratio stood at 25.2% in 2024, with slight improvement expected in 2025 as automation adoption expands. Billing automation eliminates manual processing costs, reduces staffing requirements for routine tasks, and minimises error correction expenses. Insurance billing optimisation tips focus on leveraging technology to drive down per-policy billing costs whilst maintaining service quality.

Billing integrates with reserving under actuarial standards, with cash flow projections discounting long-tail liabilities, but statutory rules limit discounting except in certain cases. Actuaries rely on billing data to project premium collection timing, which affects reserve calculations and loss development patterns. Accurate billing records enable precise measurement of premium earned, a critical input for loss ratio analysis. The relationship between billing and reserving extends to reinsurance accounting, where premium cessions and recoveries must align with billing cycles.

| Financial Metric | 2024 Industry Benchmark | Billing Impact |

| — | — |

| Net premiums written | $934 billion | Billing efficiency determines collection rates and revenue realisation timing |

| Combined ratio | 96.9% | Uncollected premiums increase ratio; billing costs affect expense component |

| Expense ratio | 25.2% | Automation reduces billing operational costs and staffing requirements |

| Premium collection rate | 97-99% typical | Effective billing workflows maximise collection and minimise write-offs |

Cash flow projections incorporate billing data to forecast investment income and liquidity needs. Insurers invest premium funds before paying claims, generating significant investment returns that supplement underwriting income. Billing delays reduce the investment period and corresponding income. Financial managers use billing analytics to predict cash receipts, optimise investment strategies, and maintain adequate liquidity for claim payments.

Revenue recognition principles require insurers to match premium income with policy periods, creating deferred revenue liabilities for unearned premium. Billing systems must track earned versus unearned premium, adjusting financial statements as policies progress. Mid-term cancellations and endorsements complicate these calculations, requiring precise proration and adjustment logic. Statutory accounting principles differ from generally accepted accounting principles in premium recognition timing, demanding dual reporting capabilities.

Pro Tip: Align billing and reserving teams to improve financial accuracy and forecasting. Regular coordination meetings ensure billing data feeds reserving models correctly, endorsement impacts are communicated promptly, and collection assumptions match actual payment patterns. This alignment reduces forecast errors and supports more accurate financial planning.

Discover modern insurance billing solutions

Modern insurance billing demands integrated platforms that automate workflows, ensure compliance, and deliver real-time visibility into receivables and payment performance. IBA’s IBSuite provides cloud-native billing capabilities designed specifically for property and casualty insurers seeking to streamline premium collection and reduce operational costs. The platform integrates billing with policy administration, claims, and financial systems, eliminating data silos and manual reconciliation. Automation handles premium calculations, invoice generation, payment processing, and exception management, freeing your team to focus on strategic initiatives rather than routine tasks. Schedule a demo of insurance billing platform to explore how IBSuite’s billing module can transform your operations, improve cash flow predictability, and enhance customer payment experiences through self-service portals and flexible payment options.

What is insurance billing?

What is insurance billing in simple terms?

Insurance billing is the complete process of calculating premiums owed, creating and sending invoices, collecting payments, and reconciling accounts to convert insurance policies into received revenue. It encompasses everything from initial premium calculation through final payment posting and exception handling.

How does technology improve billing accuracy and speed?

Technology automates premium calculations using rating engines, generates invoices instantly when policies are issued, processes payments electronically in real-time, and reconciles transactions automatically by matching payments to outstanding balances. Automation eliminates manual calculation errors and accelerates every billing step from days to minutes.

What are common causes of payment failures in billing?

Payment failures typically result from insufficient funds in policyholder accounts, expired or invalid payment methods like outdated credit cards, disputed charges where policyholders question billing accuracy, technical processing errors in payment gateways, or closed bank accounts when policyholders change financial institutions. Each cause requires specific recovery workflows to collect the premium and prevent policy cancellation.

How does billing affect insurer profitability?

Effective billing directly improves profitability by maximising premium collection rates, reducing operational expenses through automation, accelerating cash flow for investment income generation, and maintaining combined ratios below 100% by minimising uncollected premium write-offs. Every percentage point improvement in collection rates flows directly to the bottom line.

Why is compliance critical in billing processes?

Compliance ensures insurers meet regulatory requirements for notice periods, cancellation procedures, refund calculations, and premium reporting that vary by jurisdiction. Non-compliance risks regulatory penalties, licence restrictions, and legal disputes with policyholders. Billing systems must accommodate these variations whilst maintaining audit trails that demonstrate regulatory adherence during examinations.

Recommended

- What is insurance billing automation? P&C benefits 2026

- Insurance Billing Processes – Impact on P&C Insurers

- Insurance Billing Processes Explained: Complete Guide – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Step-by-Step P&C Insurer Modernization Guide for Success