What a P&C insurer licence permits in Central Europe

A property and casualty insurer licence — the formal authorisation under Directive 2009/138/EC (Solvency II) — permits a company to underwrite, administer, settle claims, accept reinsurance, and operate across EU Member States for the specific non-life classes named in the authorisation. This is a corporate authorisation, not a personal sales licence.

Key boundaries to understand from the outset:

- Scope is granular: the licence covers only the non-life classes (1–18 under Solvency II Annex I) explicitly requested and approved, not insurance broadly.

- Passporting is included: a single authorisation from one EU home supervisor, such as Hungary’s MNB or Austria’s FMA, is valid across all Member States.

- Home-state prudential responsibility applies: the home supervisor owns solvency oversight; host supervisors retain conduct supervision.

- EIOPA sets the single rulebook and coordinates supervisory convergence across the EU.

- The licence does not authorise life insurance, nor does it grant individual producer rights to employees.

Key takeaways

A P&C insurer licence under Solvency II authorises underwriting, policy administration, claims handling, and cross-border activity for specified non-life classes — but only within the capital, governance, and reporting framework the three pillars impose.

| Point | Details |

|---|---|

| Licence scope is granular | Authorisation covers only the specific non-life classes requested and approved; expanding classes requires a revised scheme of operations. |

| EUR 5m threshold matters | Very small undertakings with gross premium income below a regulatory threshold may opt out of full Solvency II but lose passporting rights across the EU. |

| IT pilot is a hard requirement | Supervisors expect a working pilot of policy admin and Pillar 3 reporting systems before granting authorisation; a description of planned capability is insufficient. |

| Passporting has conduct limits | Home-state prudential control and host-state conduct supervision run in parallel; local AML/CFT and IDD compliance applies in every market entered. |

| IBSuite supports licence readiness | Ibapplications’ IBSuite provides audit trails, regulatory reporting, and policy admin in a single platform designed for P&C supervisory requirements. |

Table of Contents

- What activities does a P&C licence actually authorise your company to do?

- How do Solvency II’s three pillars constrain what the licence lets you do?

- How do you obtain and maintain a P&C licence?

- What does passporting actually enable, and where do limits remain?

- What systems and controls must IT and compliance teams have in place?

- What options do very small insurers have under Solvency II?

- What red flags will supervisors look for?

- Executive checklist: what to decide before you file

- A practitioner’s view on sequencing in Central Europe

- IBSuite can reduce the operational friction supervisors check for

- Useful primary sources

- Sources

- FAQ

What activities does a P&C licence actually authorise your company to do?

The authorisation must specify which of the 18 non-life classes the undertaking may write. Supervisors expect applicants to request only the classes they can demonstrate they can underwrite and capitalise for — a broad request without class-level capital modelling is a common reason for rejection, as the FMA licensing guidance makes clear.

Within the approved classes, the licence covers:

- Underwriting — accepting risk, setting terms, and issuing policies for approved classes.

- Policy administration — maintaining policy records, endorsements, renewals, and cancellations.

- Claims settlement — receiving, assessing, and paying claims, including cross-border claims coordination within the EU.

- Reinsurance acceptance — carrying reinsurance business where the authorisation includes it.

- Investment of technical provisions — managing assets backing policyholder liabilities within regulatory limits.

- Branch establishment and freedom to provide services — operating in other Member States without a separate local licence, subject to notification.

Expanding into new classes after authorisation requires a revised scheme of operations and supervisor approval. Product innovation that materially changes the risk profile from the approved business plan typically triggers prior notification, even within existing classes.

Pro Tip: Draft your initial class list conservatively. Requesting fewer classes with strong capital evidence is faster to approve than a broad request with thin modelling. You can expand later once the operational track record supports it.

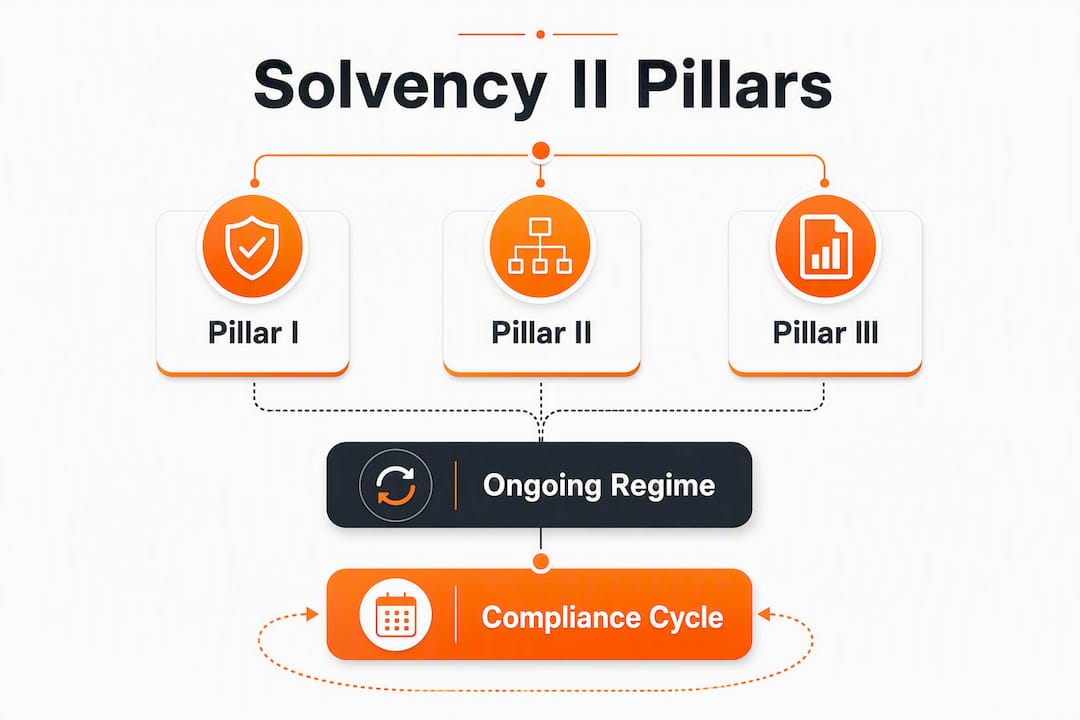

How do Solvency II’s three pillars constrain what the licence lets you do?

The European Commission’s Solvency II overview describes the framework as three interlocking pillars, each of which imposes practical limits on how freely you can use the licence.

Pillar 1 — Capital: Eligible own funds must cover both the Minimum Capital Requirement (MCR) and the Solvency Capital Requirement (SCR), modelled per the requested classes. Regulators can and do reject applications where capital evidence is weak or the modelling methodology is unconvincing.

Pillar 2 — Governance and ORSA: The Own Risk and Solvency Assessment must be embedded in operations, not produced as a one-off document. Governance requirements include fit-and-proper management, a risk management function, an actuarial function, and an internal audit function. These are prerequisites for licence validity, not post-approval niceties.

Pillar 3 — Reporting and disclosure: Quarterly and annual supervisory reporting (QRT templates), the Solvency and Financial Condition Report (SFCR), and the Regular Supervisory Report (RSR) are mandatory. The EIOPA single rulebook specifies the technical standards that govern all three.

Small undertakings threshold: Under Directive 2009/138/EC, very small undertakings that meet specific conditions including a low gross premium income may be excluded from the full Solvency II scope. They remain subject to national rules but lose passporting rights unless they opt into the full Directive.

| Pillar | Core requirement | Practical licence constraint |

|---|---|---|

| Pillar 1 | MCR and SCR coverage by eligible own funds | Limits class breadth; weak capital blocks approval |

| Pillar 2 | Governance, ORSA, four key functions | Governance gaps trigger refusal or conditions |

| Pillar 3 | QRT, SFCR, RSR reporting | Inadequate IT/reporting systems delay or block launch |

How do you obtain and maintain a P&C licence?

The MNB licensing overview and the MNB licensing guide together give the clearest picture of what Central European supervisors expect. The required submission includes:

- Incorporation documents in the chosen Member State

- A detailed business plan covering classes, premium projections, reserving methodology, and reinsurance arrangements

- Proof of eligible own funds sufficient to cover MCR and SCR from day one

- Governance documents: organisational structure, key function holders, fit-and-proper evidence

- IT pilot results demonstrating that policy admin, claims, and reporting systems are operational

- Proof of premises and operational readiness

The review focuses on business plan realism, governance substance, solvency evidence, and IT readiness. Supervisors are not looking for aspirational documents; they want evidence that the undertaking can operate safely from the first day of trading.

Common rejection reasons:

- Insufficient eligible own funds or unconvincing capital modelling

- Incomplete or immature governance and risk framework

- IT and reporting systems that cannot demonstrate a working pilot

- Business plan assumptions that are unrealistic against market benchmarks

- Fit-and-proper concerns about proposed senior managers

Capital buffer note: The MNB expects applicants to demonstrate not just MCR/SCR coverage at point of application but a credible plan for maintaining buffers under stress scenarios.

What does passporting actually enable, and where do limits remain?

A single authorisation under Article 15 of Directive 2009/138/EC permits the undertaking to establish branches or provide services across all EU Member States without a separate local licence. Slovakia’s Národná banka Slovenska confirms this principle explicitly in its authorisation framework.

What passporting does not eliminate:

- Host-state conduct supervision remains with the local authority. Consumer protection rules, policy wording requirements, and claims handling standards vary by market.

- Notification obligations apply before establishing a branch or commencing services in a host state. The FMA, for example, notifies EIOPA and the relevant host supervisor where planned activities are material for that market.

- Local claims handling arrangements are practically necessary even when prudential reporting stays centralised.

- Country-specific AML/CFT compliance applies in each host market under EU Anti-Money Laundering directives, regardless of where the home licence sits.

Pro Tip: Build your product configuration and reporting architecture to be country-parameterisable from day one. Retrofitting local conduct rules into a monolithic system after launch is significantly more expensive than designing for it upfront. See the customer onboarding playbook for Central Europe for practical conduct considerations.

What systems and controls must IT and compliance teams have in place?

Supervisors will inspect or depend on the following core systems during the application review and throughout the licence lifecycle:

- Policy administration system — must support full audit trails, endorsement history, and product configuration per class.

- Underwriting and rating engine — must reflect the approved risk appetite and class-level pricing assumptions from the business plan.

- Claims management system — must handle first notification of loss through settlement, with documented workflows and reserve tracking.

- Finance sub-ledger — must produce the figures that feed QRT templates accurately and on time.

- Regulatory reporting pipeline — must generate Pillar 3 outputs (QRTs, SFCR, RSR) to EIOPA technical standards.

ORSA workflows need to be embedded in operations, not run as an annual exercise disconnected from live data. Supervisors increasingly expect near-real-time data transparency from core systems to satisfy Pillar 2 and 3 expectations. Audit trails, data lineage, and business continuity plans are explicit attachments in the MNB application.

IBSuite by Ibapplications is one example of a platform designed around this architecture: API-first, with built-in audit trails and configurable regulatory reporting. For teams assessing regulatory compliance readiness, the key question is whether your current stack can produce a clean, traceable data lineage from policy inception to QRT submission.

Pro Tip: Run a full pilot of your Pillar 3 reporting before submitting the licence application. Supervisors treat a working pilot as evidence of operational readiness; a description of planned capability is not equivalent.

What options do very small insurers have under Solvency II?

Undertakings with gross premium income below EUR 5 million may be excluded from the full Solvency II framework under the Directive’s small-undertaking provisions. The practical consequences split into two paths:

- Remain under national rules: lighter prudential burden, lower capital and reporting overhead, but no single EU licence and no passporting. Cross-border activity requires separate national authorisations in each target market.

- Opt into Solvency II voluntarily: full compliance cost, but access to the single authorisation and the ability to write business across the EU from one home licence.

The choice is strategic. A small insurer targeting a single domestic market may find national oversight proportionate and sufficient. One with cross-border ambitions, even at modest premium volumes, will typically find the passporting benefit worth the compliance investment. National rules vary across Central Europe, so the cost differential between the two paths depends heavily on the home Member State chosen.

What red flags will supervisors look for?

Supervisory intervention, licence conditions, or outright refusal typically follow from a recognisable set of weaknesses:

- Capital shortfalls: eligible own funds that do not credibly cover MCR and SCR under stress, or modelling that cannot withstand actuarial scrutiny.

- Governance gaps: absent or nominal key functions, fit-and-proper concerns, or a risk framework that exists on paper but not in practice.

- IT and reporting immaturity: systems that cannot produce a working pilot of Pillar 3 outputs, or that lack documented audit trails and business continuity arrangements.

- Unrealistic business plan: premium projections that diverge materially from market benchmarks, or reserving assumptions that are optimistic without actuarial support.

- Outsourcing control weaknesses: material functions outsourced without documented oversight, escalation rights, and exit plans.

- AML/CFT gaps: P&C insurers are subject to EU Anti-Money Laundering obligations. Supervisors expect documented customer due diligence procedures, transaction monitoring where relevant (particularly for high-value property lines), and a named money laundering reporting officer. Missing AML/CFT controls are increasingly a standalone ground for licence conditions.

Consequences range from a request for additional information (which delays the timeline) through to formal licence conditions restricting product launches or passporting, and in serious cases, refusal.

Executive checklist: what to decide before you file

Work through these decisions in sequence before submitting an application:

- Choose the home Member State — consider supervisor accessibility, national legal form requirements, and the tax and operational environment.

- Select legal form — stock company, mutual, or SE; national rules constrain the options.

- Confirm the class list — request only classes you can capitalise and operationalise from day one.

- Build the capital plan — model MCR and SCR per class, stress-test against conservative scenarios, and confirm the buffer above minimum requirements.

- Appoint fit-and-proper senior managers — start fit-and-proper assessments early; this is frequently on the critical path.

- Commit to IT and reporting build — select or configure policy admin, claims, and reporting systems and run a pilot before filing.

- Prepare governance documentation — risk management framework, ORSA methodology, internal audit charter, and actuarial function terms of reference.

- Plan distribution — confirm whether you will use tied agents, brokers, or direct channels, and ensure IDD compliance is built into the distribution model.

Workstream ownership: legal (incorporation, class selection, governance docs), actuarial (capital modelling, reserving, ORSA), IT (systems build and pilot), compliance (AML/CFT, IDD, fit-and-proper), finance (own funds evidence and reporting).

If the capital buffer disappears under that scenario, the supervisor will find it. Better to find it first and adjust the plan or the capital structure before filing.*

A practitioner’s view on sequencing in Central Europe

The instinct of most executive teams is to spend the early months on product design. That is usually the wrong order of operations.

Regulators in Central Europe, whether the MNB in Budapest or the FMA in Vienna, prioritise policyholder protection and operational realism. A beautifully designed product range sitting on an immature reporting stack will not get a licence. Capital modelling and a minimum viable operational stack for pilot reporting should come first, before the product catalogue is finalised.

Early engagement with the home supervisor, before the formal application, is consistently undervalued. Most national supervisors in Central Europe will take a pre-application meeting. Use it. The feedback on capital methodology and governance structure is worth more than months of internal iteration.

Spend scarce budget on governance and reporting tooling. The insurance risk management framework and the Pillar 3 reporting pipeline are what supervisors inspect most closely. Cosmetic product features can wait.

IBSuite can reduce the operational friction supervisors check for

Ibapplications built IBSuite specifically for P&C insurers navigating exactly this kind of regulatory environment. The platform covers policy administration, underwriting, claims management, billing, and financial sub-ledger in a single cloud-native architecture on AWS, with full audit trails and configurable regulatory reporting built in from the ground up.

For teams preparing a licence application, that matters because supervisors want to see a working pilot, not a roadmap. IBSuite’s API-first design means it can connect to existing actuarial and reporting tools without a full rip-and-replace, which keeps the pilot timeline realistic. If your current stack cannot produce a clean data lineage from policy inception to QRT submission, that is the gap worth addressing before you file.

Book a demo to see how IBSuite maps to the supervisory checkpoints your application will face.

Useful primary sources

Bookmark these authoritative documents when preparing your application and board materials:

- Directive 2009/138/EC (Solvency II) — EUR-Lex: the primary legal text covering authorisation, classes, passporting, MCR/SCR, and the three-pillar structure.

- MNB licensing guide (PDF): the detailed document checklist and rejection grounds used by the MNB.

- FMA Insurance Supervision Act and licensing materials: Austria’s licensing framework, illustrating national practice for Central European applicants.

- European Commission — Insurance regulation: policy overview of Solvency II objectives and the three-pillar rationale.

- Národná banka Slovenska — authorisation framework: Slovakia’s authorisation provisions, confirming cross-border validity and class rules.

This article is general information, not a substitute for advice from a qualified financial advisor. Consult a qualified financial professional about your own circumstances before acting on anything here.

Sources

- Directive 2009/138/EC (Solvency II) — Eur-Lex

- Licensing guide — authorisation of the commencement of the insurance or reinsurance activity — MNB (PDF)

- Legislation

- Insurance Supervision Act 2016 and licensing details — FMA (PDF)

- Finance

FAQ

What does a P&C insurer licence permit a company to do?

It authorises the undertaking to underwrite, administer policies, settle claims, and accept reinsurance for the specific non-life classes named in the authorisation, and to operate across EU Member States via passporting under Directive 2009/138/EC.

What is the EUR 5 million threshold in Solvency II?

Undertakings with gross premium income below EUR 5 million may be excluded from the full Solvency II framework and remain under lighter national rules, but they lose the right to passport across the EU unless they voluntarily opt into the full Directive.

What are the most common reasons a P&C licence application is refused?

The MNB licensing guide identifies insufficient eligible own funds, inadequate governance or risk framework, and immature IT and reporting systems as the leading grounds for refusal or a request for additional information.

Does a single EU authorisation remove the need for local compliance in host markets?

No. Passporting removes the need for a separate local licence, but host-state conduct supervision, AML/CFT obligations, and IDD requirements apply in every market where the insurer operates.

How does IBSuite support the supervisory requirements for a P&C licence?

IBSuite by Ibapplications provides policy administration, claims management, underwriting, and Pillar 3 reporting in a single cloud-native platform with full audit trails, supporting the IT pilot evidence and data lineage that supervisors inspect during and after the authorisation process.

Recommended

- What you can do with a P&C licence in Central Europe – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurtech Ecosystem: How It Shapes P&C Insurance

- Insurance modernisation explained: a guide for Central European insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Embedded Insurance: Transforming P&C Distribution Models