17.07.26

What is self-service insurance? A guide for insurers

Self-service insurance is the provision that allows policyholders to manage routine insurance tasks directly through digital platforms, without contacting an agent or broker. Think of it as the online banking equivalent for insurance: customers log in, update their details, file a claim, or download a certificate at any time they choose. A 2026 European market survey found that 75% of insurance customers expect digital solutions for routine tasks. That figure signals a structural shift, not a passing preference, and it has direct consequences for how insurers design their platforms and service models.

What is self-service insurance and how does it work?

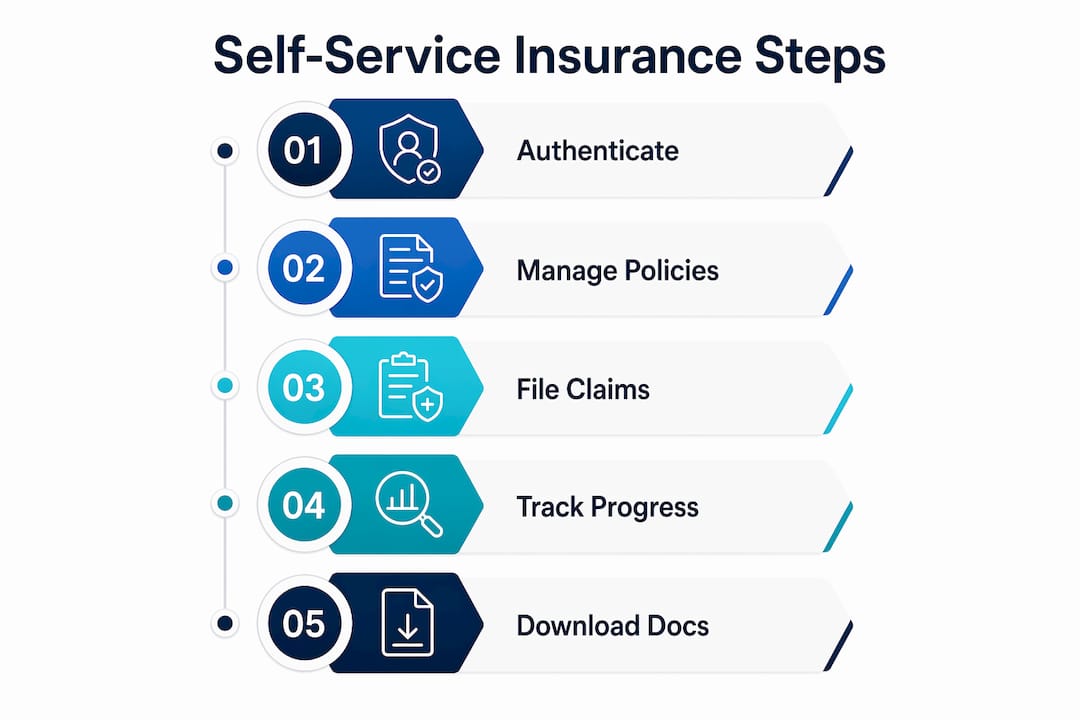

Self-service insurance, known in the industry as digital customer self-service, refers to any web or mobile channel through which policyholders complete tasks that once required agent involvement. Common tasks include updating personal details, requesting policy documents, submitting first notice of loss, tracking claim status, and renewing cover. The industry term “customer self-service portal” describes the technology layer that makes this possible.

The mechanism is straightforward. A policyholder authenticates through a web or mobile application, which connects via APIs to the insurer’s core systems: policy administration, claims management, billing, and document storage. When a customer changes their address, the request writes directly to the policy record in real time. No email, no call centre queue, no manual re-keying.

AI components add a further layer. Chatbots handle first-line queries, automated workflows route claims to the correct handler, and natural language processing can pre-populate claim forms from a short description. The result is a faster, more consistent service for routine interactions, freeing human agents to focus on complex cases.

Typical feature categories and their operational value

| Feature category | Operational value |

|---|---|

| Policy updates and endorsements | Reduces inbound call volume and manual processing time |

| Digital claims submission | Accelerates first notice of loss and speeds settlement cycles |

| Document retrieval and e-signature | Eliminates paper handling and postal delays |

| AI chatbot and virtual assistant | Provides 24/7 first-line support without staffing costs |

| Payment and billing management | Reduces late payments and improves cash flow visibility |

Pro Tip: Design your self-service portal around customer tasks, not internal process steps. Portals built around back-office workflows create fragmented experiences that push customers back to the call centre.

What are the benefits of self-service insurance?

The financial case for self-service insurance is well established. Insurers that have deployed digital self-service platforms report cost reductions of 20–40% alongside measurable improvements in service speed. Those savings come from reduced call centre volume, lower manual processing costs, and faster straight-through processing on routine transactions.

Customer satisfaction gains are equally significant. The same 2026 European survey that recorded 75% digital expectation also found that 47% of customers prefer digital channels over traditional advisors for routine tasks. Among customers aged 18–39, that preference rises to 67%. Younger policyholders do not see digital self-service as a convenience. They see it as the baseline expectation.

Key benefits for insurers

- Reduced cost per transaction on routine policy and claims tasks

- Faster processing cycles with fewer manual touchpoints

- Higher data accuracy through direct customer input

- Freed agent capacity for complex, high-value interactions

- Richer behavioural data from digital interaction logs

Key benefits for customers

- 24/7 access to policy information and documents

- Faster claims acknowledgement and status updates

- No waiting times for routine requests

- Greater transparency over policy terms and billing

- Consistent experience across web and mobile channels

Digital distribution in insurance is not uniform across product lines. Motor and travel insurance lead digital sales in Europe, while life insurance still depends heavily on personal advisory. That distinction matters when deciding which products to route through self-service channels and which to protect with human support.

What are the challenges and limitations of self-service insurance?

Self-service insurance does not work equally well across all scenarios. The most significant limitation is trust. Customers facing a major claim, a complex product question, or a life event such as bereavement or serious illness consistently prefer human contact. EIOPA’s third IDD report confirms that digital distribution in Europe remains concentrated in simple product lines. Complex products still require face-to-face or telephone advice to meet both regulatory standards and customer confidence thresholds.

The renewal rate data makes the business case for human involvement impossible to ignore. Online-only sales and service yield approximately 30% policy renewal rates. When personal engagement is integrated into the model, that figure rises to 80%. A 50-percentage-point gap in retention is not a nuance. It is a strategic risk for any insurer that treats self-service as a complete replacement for human contact.

Regulatory complexity adds a further constraint. The Insurance Distribution Directive (IDD) requires that customers receive appropriate advice for certain product categories. Fully automated journeys for products such as payment protection or unit-linked life cover may not satisfy IDD requirements without a documented advisory step. Compliance teams need to map every self-service journey against product classification before launch.

Common pitfalls to avoid

- Building portals around internal process logic rather than customer task flows

- Launching self-service for complex products without a clear escalation path to human agents

- Underestimating the usability bar: poor usability drives customers back to call centres and erodes trust in digital channels

- Failing to test with real customers before go-live, resulting in low adoption rates

- Treating self-service as a cost-cutting exercise rather than a customer experience investment

Pro Tip: Map every self-service journey to a product complexity tier before launch. Simple products like motor and travel can go fully digital. Products with significant financial or emotional stakes need a visible, easy escalation route to a human adviser.

How should insurers implement self-service insurance effectively?

Effective implementation starts with architecture. Self-service portals must connect to core systems through reusable, well-documented APIs rather than point-to-point integrations. Portals built on brittle integrations break when core systems are updated, creating service outages that damage customer trust precisely when it matters most.

The second principle is channel orchestration. A customer who starts a claim on a mobile app should be able to continue it with a telephone agent without repeating information. That continuity requires a shared data layer across channels, not separate systems for digital and human touchpoints. Insurers that achieve this report the highest satisfaction scores in hybrid service models.

A 2026 customer centricity study found that the hybrid model combining digital efficiency with human advisory is the most successful approach for both customer trust and operational efficiency. The practical implication is that self-service platforms should be designed with escalation built in, not bolted on as an afterthought.

Implementation steps for insurance decision-makers

- Audit current customer journeys. Identify which tasks generate the highest call centre volume and are low in complexity. These are your first candidates for self-service.

- Define product tiers. Classify products by complexity and regulatory requirement. Simple products go digital first; complex products retain human advisory with digital support.

- Choose a composable architecture. Select a policy administration platform that exposes APIs for every core function, so self-service features can be added or updated without rebuilding the core.

- Design from the customer context outward. Build task flows around what the customer is trying to achieve, not around how your back office is organised.

- Build escalation into every journey. Every self-service screen should offer a clear, low-friction route to a human agent for customers who need it.

- Measure and iterate. Track completion rates, drop-off points, and post-interaction satisfaction scores. Use that data to refine journeys continuously.

Pro Tip: Treat your first self-service launch as a pilot, not a finished product. Release to a defined customer segment, measure behaviour, and iterate before scaling. Insurers that skip this step typically spend more fixing usability problems post-launch than the pilot would have cost.

Key takeaways

Self-service insurance delivers measurable operational gains only when digital channels are designed around customer tasks and supported by clear escalation to human advisers for complex cases.

| Point | Details |

|---|---|

| Digital expectation is high | 75% of European insurance customers expect digital solutions for routine tasks. |

| Hybrid models retain customers | Online-only service yields 30% renewal rates; integrating human contact raises this to 80%. |

| Product complexity sets the boundary | Simple products like motor and travel suit full digital self-service; complex products require human advisory. |

| Architecture determines success | Composable, API-first platforms prevent the brittle integrations that cause self-service failures. |

| Usability is non-negotiable | Poor portal design drives customers back to call centres and undermines the business case for digital investment. |

The case for getting the balance right

The insurers I see struggling with self-service share a common mistake: they treat it as a cost reduction project rather than a customer experience project. The cost savings are real, and the 20–40% reduction in transaction costs is compelling. But the moment a customer hits a confusing screen, a broken journey, or a dead end with no human in sight, the economics reverse. Call centre volumes spike, complaints rise, and renewal rates fall.

What I find genuinely interesting about the 2026 data is the renewal rate gap. A 50-percentage-point difference between digital-only and hybrid models is not a marginal finding. It tells you that customers are willing to use digital channels for convenience, but they want to know a human is available when the stakes are high. The insurers winning in this space are not the ones with the most features. They are the ones who have thought carefully about when to hand off from digital to human and made that handoff feel natural.

The digital transformation drivers shaping European insurance right now all point in the same direction: composable platforms, open APIs, and AI-assisted workflows. But the underlying principle has not changed. Insurance is a promise made under uncertainty. Customers need to trust that promise. Self-service is the delivery mechanism for routine interactions. Human advisers are the guardians of trust when it matters most. Getting that balance right is the defining challenge for insurance leaders in 2026.

— Tuna

How IBSuite supports self-service insurance capabilities

Ibapplications built IBSuite as an API-first, cloud-native platform specifically for property and casualty insurers who need to move quickly on digital distribution. The policy administration system within IBSuite exposes every core function through open APIs, which means self-service portals can connect directly to policy records, claims workflows, billing, and document management without custom integration work. Insurers using IBSuite can configure new self-service journeys without rebuilding their core systems. For decision-makers evaluating how to modernise their customer-facing operations, IBSuite provides the technical foundation that makes hybrid digital and human service models practical rather than aspirational.

FAQ

What is self-service insurance in simple terms?

Self-service insurance lets policyholders manage routine tasks such as updating details, filing claims, and downloading documents through a digital portal, without contacting an agent.

How does self-service insurance affect renewal rates?

Online-only service models produce approximately 30% renewal rates. Integrating personal engagement alongside digital channels raises renewal rates to around 80%.

Which insurance products are best suited to self-service?

Motor and travel insurance lead digital self-service adoption in Europe. Complex products such as life insurance and payment protection still require human advisory to meet regulatory and customer confidence standards.

What technology underpins a self-service insurance platform?

Self-service platforms rely on API connections to core policy administration, claims, and billing systems, supported by AI chatbots, automated workflows, and secure customer authentication.

What is the biggest risk when launching self-service insurance?

Poor usability is the most common failure point. Customers who encounter confusing or broken journeys revert to call centres, which eliminates the cost and efficiency gains the platform was designed to deliver.