02.04.26

Insurance customer self-service: boost engagement in 2026

85% of policyholders now value instant digital access to payments, ID cards, and policy details, yet many insurers still rely on phone queues and manual processes that frustrate rather than retain. The gap between what customers expect and what most carriers deliver is widening fast. For property and casualty (P&C) insurance leaders, closing that gap is no longer a future ambition. It is a present-day competitive necessity. This guide breaks down what insurance customer self-service actually means, why the business case is stronger than ever, what commonly goes wrong, and how to build something that genuinely works.

Table of Contents

- What is insurance customer self-service?

- Key benefits: Why insurers are prioritising self-service

- Risks, trade-offs, and what most self-service rollouts get wrong

- Best practices: Designing self-service that delivers results

- Why the real competitive edge is trust, not just automation

- Take customer engagement to the next level with IBApplications

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Digital self-service is essential | Modern insurance customers expect quick, flexible online access to their policy needs. |

| Empirical benefits are clear | Leading insurers achieve lower costs and higher satisfaction by digitising routine workflows. |

| Not a replacement for agents | Human guidance is still vital for complex situations and escalations. |

| Trust outpaces technology | Data quality, transparency, and balanced automation determine long-term success. |

| Actionable rollout steps | Prioritise high-ROI modules, benchmark against leaders, and ensure strong UX and compliance. |

What is insurance customer self-service?

Insurance customer self-service is the digital enablement of routine insurance tasks that policyholders complete on their own, without needing to call an agent or visit a branch. Think of it as giving your customers a well-organised control panel for their insurance relationship. They log in, do what they need, and move on with their day.

The range of interactions covered is broader than many executives initially assume. Core self-service capabilities typically include:

- Viewing and downloading policy documents and certificates

- Reporting First Notice of Loss (FNOL), the initial claim notification after an incident

- Tracking claim status in real time

- Accessing digital ID cards

- Updating contact and billing details

- Making payments and viewing payment history

- Requesting policy endorsements or coverage changes

72% of customers prefer digital self-service for policy changes, which signals a clear shift in how policyholders want to interact with their insurers. This is not a niche preference. It is mainstream behaviour.

Critically, self-service is not about replacing agents. It is a choice model. Complex queries, sensitive claims, and relationship-driven conversations still benefit enormously from skilled human involvement. What self-service does is free your agents to focus on those high-value interactions, while routine tasks are handled efficiently by the customer themselves. When built on modern insurance platforms, self-service becomes the foundation for improved customer experience (CX), meaningful cost efficiency, and genuine competitive differentiation.

Pro Tip: Map your current inbound call types before investing in self-service features. If 40% of calls are payment queries, that is your first digitisation priority, not the most technically exciting feature on your roadmap.

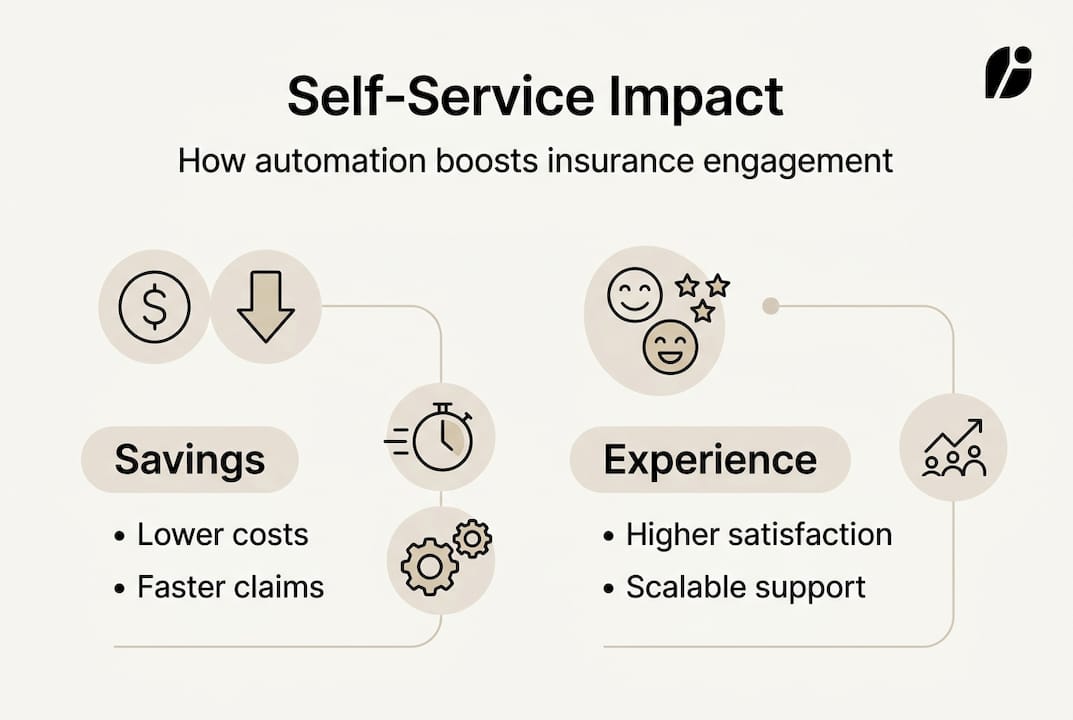

Key benefits: Why insurers are prioritising self-service

The drivers of digital transformation in insurance are well documented, but the financial and operational case for self-service specifically is compelling enough to stand on its own.

The headline figure: digitisation and automation can reduce operating expenses by up to 40%, alongside a 30 to 50% reduction in inbound call volumes. For a mid-sized P&C insurer handling tens of thousands of routine interactions monthly, that is a transformational cost reduction.

| Benefit | Impact |

|---|---|

| Reduced cost per interaction | Digital self-service costs a fraction of agent-handled calls |

| Higher customer satisfaction | Fast resolution drives loyalty and reduces churn |

| Scalability during peak events | Portals absorb catastrophe claim surges without staffing spikes |

| Competitive differentiation | Leaders set benchmarks that peers scramble to match |

| Agent productivity | Frees staff for complex, high-value conversations |

Beyond cost, customer satisfaction scores rise sharply when policyholders can resolve issues quickly and independently. Loyalty is built not in the moment of purchase but in the moments of need. A customer who files a FNOL at 11pm from their phone and receives instant confirmation is far less likely to shop around at renewal.

Scalability deserves special attention. Catastrophe events create sudden, massive claim surges that overwhelm traditional service models. A well-built self-service portal absorbs that volume without a corresponding spike in staffing costs. Knowing how to digitise insurance processes effectively is what separates insurers who thrive during those events from those who simply survive them.

Forward-thinking insurers are also recognising self-service as a competitive signal. When your portal is faster, cleaner, and more capable than a competitor’s, that becomes part of your value proposition at the point of sale.

Risks, trade-offs, and what most self-service rollouts get wrong

The case for self-service is strong. But the path to getting it right is littered with expensive mistakes. Clunky UX, data quality issues, lack of human fallback, and underinsurance risk remain the most cited concerns from insurers who have invested heavily and seen disappointing results.

Here is what typically goes wrong, in order of frequency:

- Poor user experience leads to abandonment. If your self-service portal requires more than three steps to find a policy document, customers will call instead. Every unnecessary click is a failure point.

- Data quality errors undermine trust. If a customer sees incorrect coverage details or an outdated payment record, they lose confidence in the entire platform, and in your brand.

- No clear escalation path. Self-service must always offer a visible, frictionless route to human support. Customers who feel trapped in a digital loop become your most vocal detractors.

- Underinsurance risk. Without guided prompts or advisory nudges, customers making self-service coverage changes may inadvertently reduce protection. This creates liability exposure and poor outcomes at claim time.

“The insurers who struggle most with self-service are not the ones who built too little. They are the ones who automated too fast without designing for the moments when customers genuinely need a human.”

Data privacy is another non-negotiable. Robust insurance data privacy controls are mandatory, not optional. GDPR compliance, secure authentication, and transparent data handling are table stakes for any self-service deployment in 2026.

Pro Tip: Before launch, run your self-service flows through usability testing with real policyholders across different age groups and digital literacy levels. What feels intuitive to your development team may be completely opaque to a 65-year-old filing their first FNOL. The role of AI in P&C insurance is growing, but human-centred design remains the foundation.

Best practices: Designing self-service that delivers results

Given these risks, what actually works? The most successful self-service rollouts in P&C insurance share a consistent set of priorities.

- Start with high-ROI workflows. Policy documents, FNOL, and payments deliver the highest return when digitised first. These are the interactions customers need most frequently and where digital resolution creates the greatest satisfaction uplift.

- Integrate AI thoughtfully. Personalisation through AI-powered customer engagement can surface relevant coverage recommendations, flag anomalies in claims data, and guide customers through complex flows. But every AI touchpoint must have a clear human fallback. Explainability matters too: customers should understand why they are seeing a particular prompt or recommendation.

- Benchmark against leaders, not just peers. The best P&C self-service portals are now being compared to retail and banking apps by customers. Your benchmark should be the best digital experience your customer uses daily, not the industry average.

- Build on cloud-native, API-first core systems. Scalability, integration flexibility, and the ability to iterate quickly all depend on your underlying technology. Approaches to API-first personalisation demonstrate how modern architecture enables insurers to tailor experiences at scale without rebuilding from scratch.

- Measure continuously. Track abandonment rates, task completion rates, and post-interaction satisfaction scores. Use that data to prioritise your next iteration.

Pro Tip: Do not treat self-service as a one-time project. The insurers who win are those who treat their digital portal as a living product, releasing improvements regularly and responding to customer behaviour data. Modernising insurance operations is an ongoing discipline, not a destination.

Why the real competitive edge is trust, not just automation

Here is the uncomfortable truth that most self-service guides skip over: automation is a commodity. Every insurer will eventually have a portal, a mobile app, and some form of digital FNOL. The technology itself will not separate winners from losers for long.

What will separate them is trust. Customers who encounter a data error, a confusing flow, or a dead end when they need help do not just abandon the task. They abandon the insurer. Trust, once broken in a digital interaction, is extraordinarily difficult to rebuild.

The insurers who will genuinely outpace their competitors are those who design self-service with human fallback built in from day one, not bolted on as an afterthought. They are transparent about how data is used. They offer flexibility for customers who want digital and for those who still want a phone call. They build modern insurance platforms that empower both policyholders and intermediaries, creating lifetime relationships rather than transactional touchpoints.

Automation delivers scale. Trust delivers loyalty. The smartest investment you can make in self-service is designing for both simultaneously.

Take customer engagement to the next level with IBApplications

The self-service principles covered in this guide, from high-ROI workflow prioritisation to AI integration and human fallback design, require a core platform that can actually deliver them. IBApplications’ IBSuite is built precisely for this. As a cloud-native, API-first platform, IBSuite Insurance Platform supports the full P&C insurance value chain, giving you the technical foundation to launch and iterate self-service capabilities at speed. Explore sales and underwriting solutions and policy administration features to see how IBApplications helps insurers build the digital experiences that today’s policyholders expect and tomorrow’s market will demand.

Frequently asked questions

What are the most common self-service features in P&C insurance?

Policy document access, payments, FNOL, and policy changes are the most used self-service features. 85% of users value quick access to payments, ID cards, and policy details above all other digital capabilities.

Does self-service mean customers never need a human agent?

No. Complex claims and disputes still require skilled human intervention for the best outcomes. Complex claims require human escalation, with AI flagging issues for agents rather than replacing their judgement.

How does self-service impact customer loyalty?

Fast, easy access to policy information and quick resolutions increase loyalty, while friction or errors drive customers away. 60% consider switching after a poor claims experience, making seamless self-service a direct retention tool.

Can digital self-service help handle claim surges during catastrophes?

Yes. Robust self-service portals help insurers scale up and manage high claim volumes efficiently. Digital self-service handles surges during catastrophe events without requiring proportional increases in staffing.

What are critical best practices for launching self-service in insurance?

Prioritise high-ROI workflows, ensure strong UX and data quality, and always provide clear escalation to human support. Prioritising high-ROI features alongside robust human fallback is what consistently separates successful rollouts from costly failures.

Recommended

- Customer Experience Improvement Guide for P&C Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance Customer Experience 2025: Shaping Engagement and Growth

- Insurance Customer Experience: Complete Guide for 2025 – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Use Cases – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- How to optimize customer engagement with AI in 2026 | Artificial Intelligence