20.11.25

The Real Cost of Doing Nothing: Insurance Core Replacement

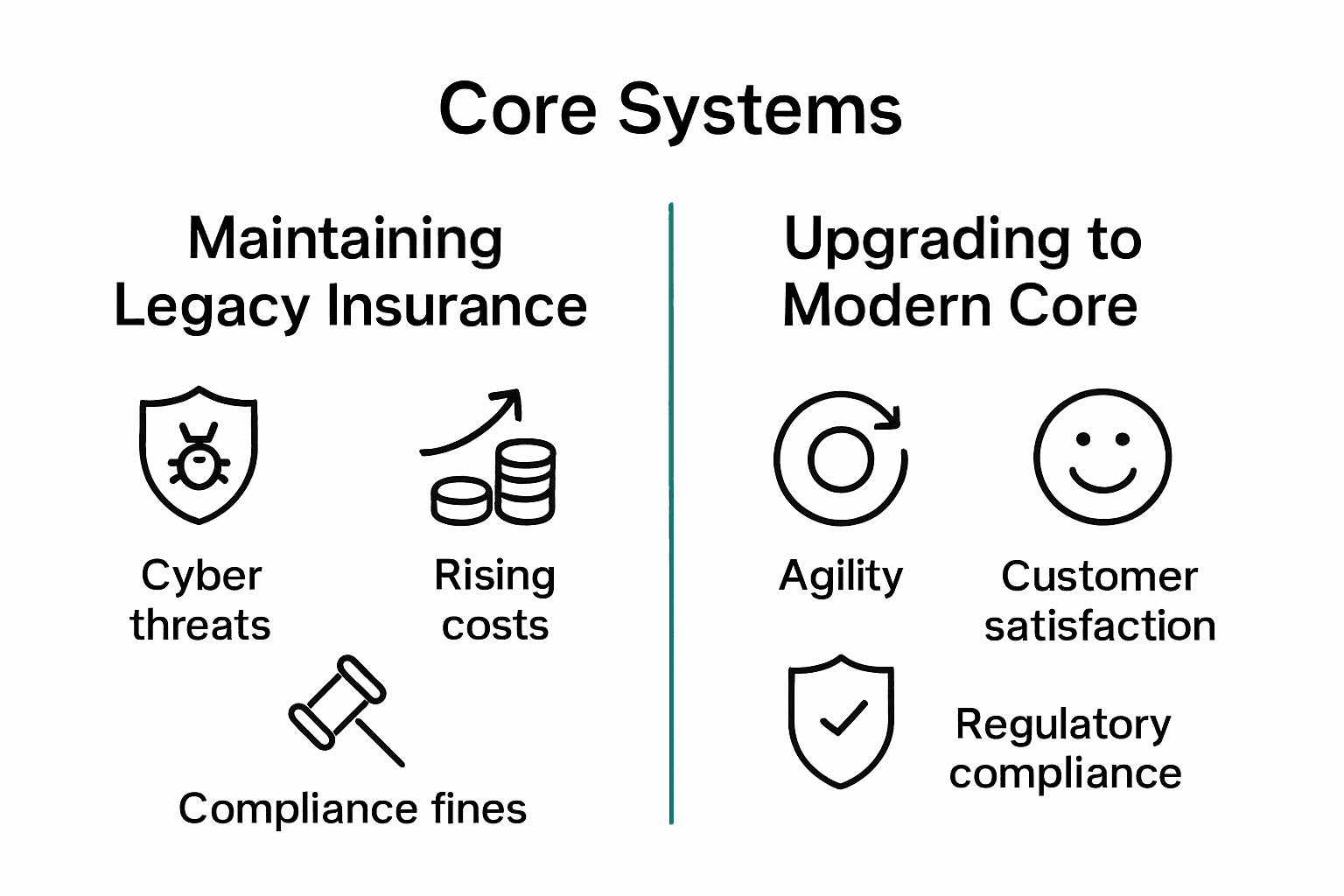

Legacy insurance systems are leaving many providers at a disadvantage, with over 60 percent of executives citing outdated technology as a barrier to growth. Navigating complex regulations, rising customer demands, and a shortage of skilled IT professionals makes the need for core system transformation more pressing than ever. Understanding what drives core replacement and the risks of standing still helps insurers make choices that protect business value while preparing for future innovation.

Table of Contents

- Defining Insurance Core Replacement Needs

- Opportunity Cost Of System Stagnation

- Regulatory Change And Compliance Risks

- IT Talent Scarcity And Operational Impact

- Customer Expectations And Market Relevance

- Practical Pathways To Minimizing Business Risk

Key Takeaways

| Point | Details |

|---|---|

| Core System Replacement is Strategic | Insurers must view core system modernization as a comprehensive initiative to enhance operational efficiency and customer experience, while aligning with business objectives. |

| Opportunity Cost of Stagnation | Failing to modernize leads to greater long-term risks and costs associated with outdated technologies and missed opportunities for innovation. |

| Regulatory Compliance is Critical | Outdated systems hinder an insurer’s ability to adapt to evolving regulations, which may result in significant financial penalties and operational limitations. |

| Talent Scarcity Impacts Transformation | A shortage of skilled IT professionals can delay core system replacements and hinder operational effectiveness, requiring strategic investment in talent development. |

Defining Insurance Core Replacement Needs

Insurance core replacement represents a strategic transformation process where insurers modernize their foundational technology infrastructure to improve operational efficiency, customer experience, and competitive responsiveness. According to internationalinsurance.org, property and casualty insurers must critically evaluate their existing systems to determine whether building, buying, or upgrading core systems will best serve their organizational goals.

Core system replacement involves comprehensively upgrading multiple interconnected technological components that support critical insurance functions. These typically include policy administration, underwriting, claims processing, billing, and customer relationship management systems. The complexity of this undertaking requires insurers to conduct thorough assessments that examine current technological limitations, future scalability requirements, and potential business impact.

Research from ijcttjournal.org emphasizes that successful core system modernization is not merely a technological upgrade but a multifaceted organizational transformation. Key considerations for insurance organizations include:

- Alignment with strategic business objectives

- Compatibility with existing technological ecosystems

- Potential for integrating emerging technologies like AI and advanced analytics

- Total cost of implementation and long-term return on investment

- Minimizing operational disruptions during transition

By approaching core system replacement as a holistic strategic initiative, insurers can unlock significant operational improvements and position themselves competitively in an increasingly digital insurance landscape.

Opportunity Cost of System Stagnation

System stagnation in the insurance industry represents a critical strategic risk that extends far beyond technological obsolescence. According to green.org, maintaining outdated legacy systems exposes insurers to significant vulnerabilities, including escalating cybersecurity threats, innovation constraints, and mounting operational costs.

Opportunity costs emerge when insurers delay modernization, creating a cascading effect of missed strategic advantages. These hidden expenses manifest through reduced operational agility, limited product innovation capabilities, and decreased competitive responsiveness. While immediate system replacement might seem financially daunting, the long-term consequences of technological inertia can be substantially more expensive.

Interestingly, research from scholarworks.waldenu.edu suggests that financial performance metrics alone may not fully justify system replacements. This nuanced perspective underscores the need for insurers to evaluate modernization through a comprehensive lens that considers:

- Cybersecurity resilience

- Operational efficiency gains

- Customer experience enhancement

- Technological adaptability

- Future innovation potential

Ultimately, system stagnation is not just a technological challenge but a strategic inflection point where insurers must decide between incremental preservation and transformative growth. The opportunity cost of maintaining legacy infrastructure extends beyond immediate financial considerations, potentially compromising an organization’s long-term market positioning and innovation capacity.

Regulatory Change and Compliance Risks

Regulatory landscapes in the insurance industry are increasingly complex, demanding unprecedented adaptability from insurers. According to imf.org, insurance regulation now encompasses comprehensive frameworks covering micro- and macroprudential supervision, corporate governance, and intricate market conduct requirements that challenge traditional operational models.

Compliance risks have become a critical strategic concern, extending far beyond simple regulatory adherence. Outdated core systems create significant vulnerabilities in meeting evolving regulatory mandates, potentially exposing insurers to substantial financial penalties, reputational damage, and operational restrictions. The rapid pace of regulatory changes demands technological infrastructure that can quickly adapt and integrate new compliance requirements.

Research from cambridge.org highlights the critical role of integrated project management frameworks in navigating regulatory complexities. Key compliance challenges for insurers include:

- Rapid interpretation of new regulatory requirements

- Seamless integration of compliance mechanisms

- Real-time reporting and documentation capabilities

- Proactive risk management strategies

- Maintaining data privacy and security standards

Insurers who view regulatory compliance as a strategic opportunity rather than a mere administrative burden can transform potential risks into competitive advantages, leveraging advanced technological infrastructures to demonstrate agility and commitment to robust governance.

IT Talent Scarcity and Operational Impact

The insurance industry faces a critical challenge in securing specialized IT talent capable of navigating complex core system transformations. According to mplassociation.org, successful legacy system migrations depend on a sophisticated intersection of technical expertise, strategic understanding, and nuanced vendor management skills that are increasingly rare in the current talent market.

IT talent scarcity represents more than a recruitment challenge—it’s a strategic vulnerability that directly impacts an organization’s technological resilience and innovation potential. Modern insurance core system replacements require professionals who understand both intricate technological architectures and complex business processes. The limited pool of professionals with these specialized skills creates significant operational bottlenecks, potentially delaying critical transformation initiatives and exposing organizations to competitive risks.

Research from theclm.org highlights the multifaceted challenges of system upgrades, emphasizing the critical role of skilled IT professionals. Key operational impacts of talent scarcity include:

- Prolonged system migration timelines

- Increased project implementation costs

- Higher risk of technological implementation failures

- Reduced capacity for innovative solution development

- Compromised system integration capabilities

Insurers must adopt comprehensive strategies to mitigate talent scarcity, including targeted recruitment, robust training programs, strategic partnerships with technology providers, and creating compelling professional development environments that attract top-tier technological talent.

Customer Expectations and Market Relevance

Customer expectations in the insurance industry are evolving at an unprecedented pace, driven by digital transformation and heightened technological experiences across other consumer sectors. According to internationalinsurance.org, property and casualty insurers must leverage cloud-based platforms, generative AI, and real-time analytics to deliver the instantaneous, personalized experiences modern consumers demand.

Digital expectations now transcend traditional service models, requiring insurers to provide seamless, intuitive interactions that mirror the convenience of digital-first industries. Outdated core systems create significant friction, preventing insurers from implementing innovative features like real-time policy adjustments, predictive risk assessments, and personalized coverage recommendations. This technological lag directly undermines an organization’s ability to attract and retain digitally sophisticated customers who increasingly view insurance through a technology-enabled lens.

Research from green.org emphasizes the critical importance of technological modernization in maintaining market relevance. Key customer expectation challenges include:

- Instantaneous quote and policy generation

- Personalized risk assessment and pricing

- Seamless omnichannel communication

- Transparent and configurable coverage options

- Predictive and proactive risk management

Insurers who view technological transformation as a strategic customer engagement tool—rather than a mere operational upgrade—can differentiate themselves in an increasingly competitive marketplace, turning technological investment into a powerful customer acquisition and retention strategy.

Practical Pathways to Minimizing Business Risk

Effective business risk mitigation in insurance core system replacement requires a strategic, methodical approach that balances technological innovation with operational stability. According to mplassociation.org, successful digital transformation hinges on a comprehensive roadmap that carefully addresses both technological and business challenges, emphasizing the need for meticulous planning and vendor selection.

Risk management in core system transitions demands a holistic perspective that extends beyond technical implementation. Organizations must develop comprehensive strategies that anticipate potential disruptions, create robust contingency plans, and maintain continuous operational capabilities during complex technological transformations. This approach requires deep alignment between IT capabilities, business objectives, and strategic risk mitigation frameworks.

Research from theclm.org underscores the importance of strategic development planning. Key practical pathways for minimizing business risk include:

- Comprehensive requirements gathering and validation

- Phased implementation strategies

- Rigorous vendor and solution evaluation

- Continuous stakeholder engagement

- Robust testing and validation protocols

- Comprehensive change management processes

- Ongoing performance monitoring and optimization

Successful risk mitigation requires insurers to view core system replacement not as a singular technological project, but as a strategic organizational transformation that demands continuous adaptation, clear communication, and a proactive approach to identifying and addressing potential vulnerabilities.

Unlock Growth and Reduce Risk with Modern Core Insurance Systems

The article highlights the real cost of doing nothing when it comes to insurance core replacement. Legacy systems create hidden risks like regulatory noncompliance, cybersecurity vulnerabilities, and missed opportunities for innovation. If your organization faces challenges such as IT talent scarcity, operational disruptions, or falling short of evolving customer expectations, these pain points demand immediate strategic action. Modernizing your core infrastructure is essential to enhance agility, streamline operations, and stay competitive.

Insurance Business Applications (IBA) offers a proven solution with IBSuite, a cloud-native, API-first platform designed to support the full insurance value chain securely and efficiently. With IBSuite, insurers can achieve rapid product innovation, maintain regulatory compliance, and improve customer engagement without the typical complexity and risk of legacy upgrades. See how IBSuite drives transformational growth while minimizing operational disruptions by booking a personalized demo today. Take the first step to future-proof your business and reduce the opportunity cost of system stagnation by visiting Book a Demo. Learn more about empowering your organization with insurance core modernization solutions and embrace the digital future the industry demands.

Frequently Asked Questions

What is insurance core replacement?

Insurance core replacement is a strategic transformation process where insurers modernize their foundational technology infrastructure to enhance operational efficiency, customer experience, and competitive responsiveness. It involves upgrading multiple interconnected systems that support key insurance functions like underwriting and claims processing.

What are the risks of system stagnation in the insurance industry?

System stagnation poses several risks, including escalating cybersecurity threats, increased operational costs, and limited innovation capabilities. Delaying modernization can result in significant opportunity costs and may compromise an organization’s long-term market positioning.

How do regulatory changes affect insurance core systems?

Regulatory changes create complex compliance risks for insurers, especially if they rely on outdated core systems. These systems may struggle to adapt to evolving requirements, exposing insurers to potential financial penalties and operational restrictions.

How can insurers mitigate the impact of IT talent scarcity during core system transformation?

To mitigate IT talent scarcity, insurers should adopt comprehensive strategies that include targeted recruitment, robust training programs, strategic partnerships with tech providers, and creating professional development environments that attract skilled experts.

Recommended

- The benefits of a multi-core strategy for insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Core Insurance Systems: What They Are and Why They Matter – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Replacing the Core – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Why modernize? – Pressure from the market – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Does a Rebuilt Title Affect Insurance? Complete Guide | ReVroom

- Understanding Insurance Claim Total Loss: What You Need to Know | ReVroom