Cloud adoption in insurance: efficiency and growth guide

The property and casualty insurance sector stands at a crossroads. Whilst global cloud services in insurance will grow at 14.5% CAGR through 2034, many insurers still rely on legacy infrastructure that limits their ability to compete. Market leaders are already leveraging cloud platforms to accelerate claims processing, enhance underwriting accuracy, and deliver customer-centric experiences. This guide reveals how cloud adoption drives operational efficiency and customer engagement, equipping you to navigate implementation challenges and select the deployment model that aligns with your strategic goals.

Table of Contents

- Trends shaping cloud adoption in insurance

- Business case: operational gains and customer value

- From legacy to cloud: overcoming adoption barriers

- Choosing the right deployment: SaaS, multi-cloud, and hybrid models

- The future: AI and cloud synergy in insurance operations

- Accelerate your cloud journey with the right partner

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cloud adoption is accelerating | P&C insurers face industry-wide urgency as cloud investment surges and competitors modernise. |

| Efficiency and growth gains | Cloud-based analytics and AI drive lower costs, premium growth, and improved customer experience. |

| Barriers can be overcome | Careful planning around integration, security, and talent makes cloud transition achievable. |

| Choosing the right model | Deployments such as SaaS, multi-cloud and hybrid should align with each insurer’s needs and strategy. |

| AI is the next frontier | Cloud is the foundation for rapid AI advances in claims, pricing, and operational innovation. |

Trends shaping cloud adoption in insurance

Understanding what drives cloud momentum in P&C insurance helps you position your organisation for success. Investment priorities reveal where the industry is heading and why cloud infrastructure has become essential.

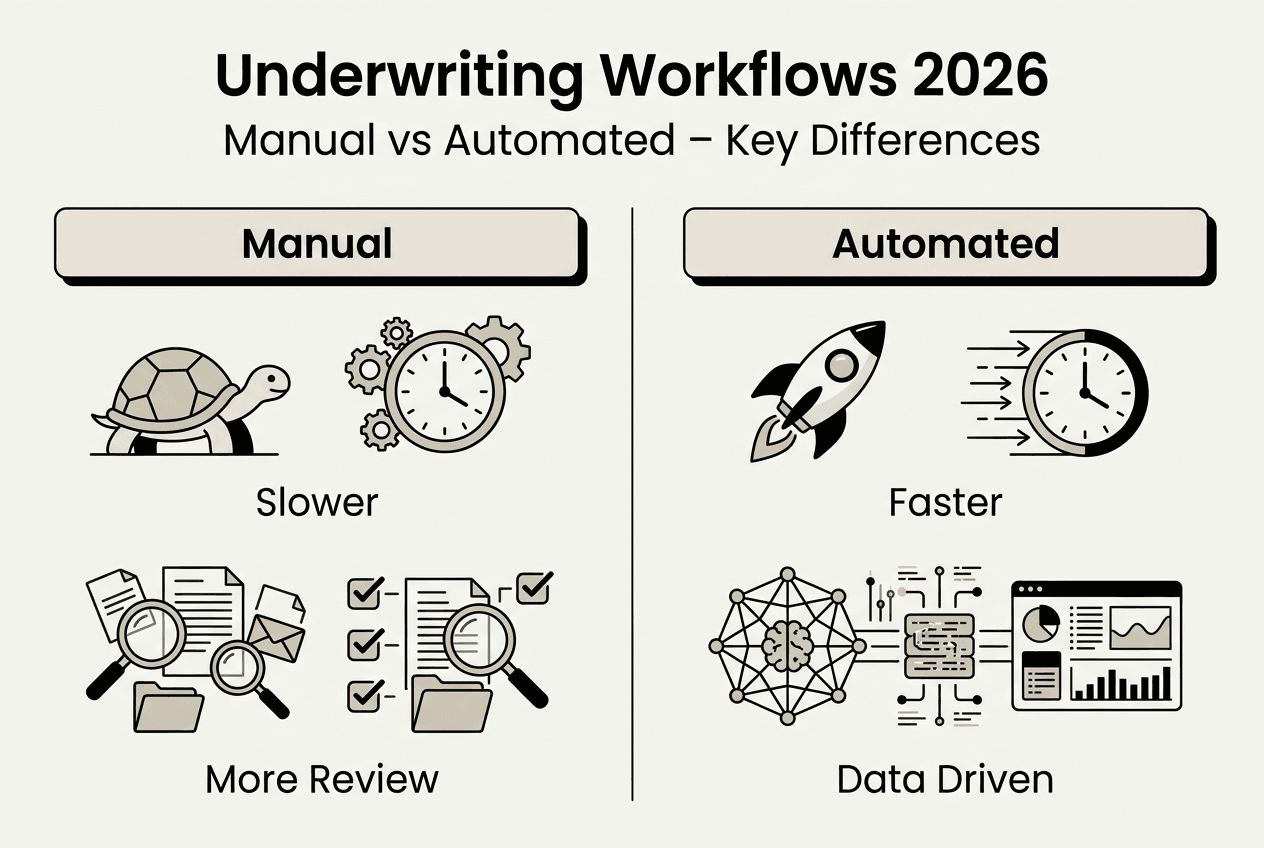

Investment is concentrated in three critical areas. Forty-four per cent of insurers are boosting investments in data and analytics in 2026, making it the top spending category. Core system upgrades and distribution channels follow closely, with modernisation considered essential for two-thirds of P&C core insurance firms. These priorities directly support digital transformation drivers that separate market leaders from laggards.

Cloud platforms enable rapid scaling across your entire value chain. Claims management benefits from elastic computing resources during catastrophe events. Underwriting teams access real-time data feeds for more accurate risk assessment. Distribution partners integrate seamlessly through API-first architectures, launching new products in weeks rather than months.

Geographic adoption patterns reveal market maturity levels:

- North American insurers lead global adoption, driven by competitive pressure and regulatory support for innovation

- European markets follow closely, with strong emphasis on data sovereignty and GDPR compliance

- Asian markets show slower uptake due to regulatory complexity and preference for on-premises infrastructure

- Emerging markets leapfrog legacy systems entirely, adopting cloud-native platforms from inception

The cloud services market growth trajectory suggests that hesitation carries real competitive risk. Insurers who delay cloud adoption face mounting technical debt and diminishing ability to meet customer expectations shaped by digital-first experiences in other industries.

Business case: operational gains and customer value

With adoption drivers established, what do insurers actually gain from robust cloud strategies? The answer lies in measurable improvements to your combined ratio and premium growth.

Analytics and AI deliver quantifiable financial results. Insurers who invest in advanced analytics achieve 6-point lower combined ratios and 3-point higher premium growth compared to peers. These gains stem from better risk selection, more accurate pricing, and faster claims resolution. Cloud infrastructure provides the computational power and data accessibility that make these analytics possible at scale.

Customer-facing capabilities depend entirely on cloud flexibility. Self-service portals that let policyholders update coverage or file claims require always-available infrastructure. Dynamic pricing engines that adjust rates based on real-time risk factors need instant access to multiple data sources. Personalised product recommendations rely on machine learning models that process vast datasets.

| Operational area | Cloud benefit | Typical improvement |

|---|---|---|

| Claims processing | Automated workflows and document analysis | 40-60% faster resolution |

| Underwriting | Real-time data integration and risk scoring | 30-50% productivity gain |

| Policy administration | Self-service and instant quotes | 70% reduction in manual tasks |

| Customer service | Omnichannel access and chatbots | 50% lower contact centre volume |

These improvements translate directly to cloud value for insurers through reduced operational costs and enhanced customer retention. Policyholders who experience fast, digital-first service are significantly more likely to renew and purchase additional products.

“Cloud platforms don’t just host applications—they fundamentally change how insurers operate, enabling capabilities that were economically impossible with legacy infrastructure.”

Pro Tip: When evaluating cloud solutions, insist on reliable API integration capabilities, not just cloud hosting. True efficiency gains come from seamless data flow between systems, not simply moving existing applications to remote servers. Core system modernisation requires rethinking processes, not just rehosting technology.

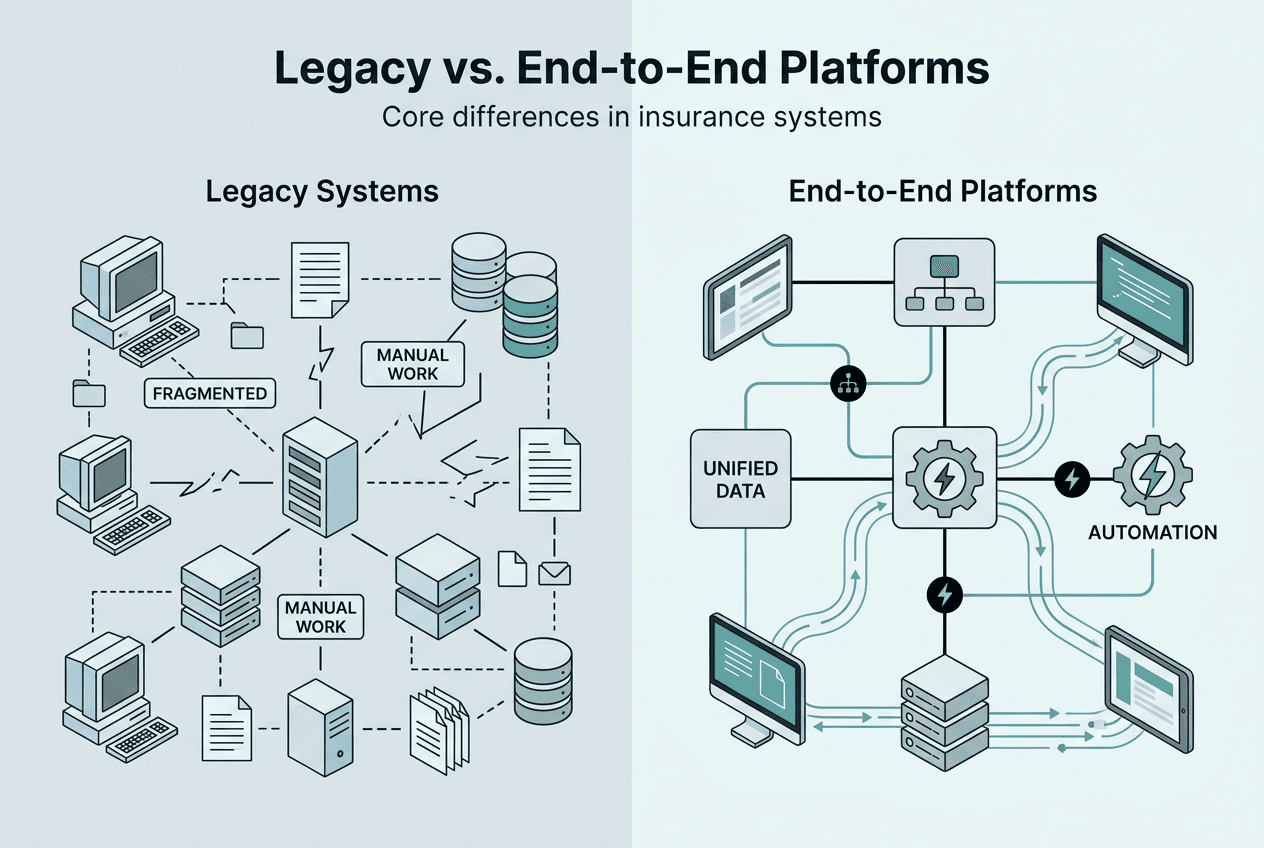

From legacy to cloud: overcoming adoption barriers

Whilst the advantages are clear, the journey from legacy infrastructure to cloud isn’t seamless. Understanding common obstacles helps you build realistic implementation plans.

Executive resistance often centres on cost and control concerns. Initial cloud investments appear substantial when compared to maintaining existing systems. Data sovereignty worries persist, particularly for insurers operating across multiple jurisdictions with varying privacy regulations. These concerns are valid but often overestimate risk whilst underestimating the cost of inaction.

Skills gaps present immediate practical challenges. Your IT teams need expertise in APIs, microservices architecture, cloud security, and integration patterns. Interest in APIs in P&C insurance doubled to 68%, yet satisfaction with analytics capabilities remains low. This gap between interest and execution reflects the learning curve organisations face.

Common pitfalls that derail cloud initiatives include:

- Underestimating process change requirements—technology migration alone doesn’t deliver value

- Inadequate security planning that creates vulnerabilities during transition periods

- Attempting to replicate legacy workflows in cloud environments rather than redesigning for cloud-native patterns

- Neglecting change management and user training, leading to poor adoption

- Selecting vendors based solely on price rather than insurance industry expertise

Successful insurers address cloud adoption challenges through phased approaches. Start with non-critical workloads to build team capabilities. Establish clear governance frameworks that address integration challenges before they become blockers. Invest in training programmes that upskill existing staff rather than relying entirely on external hires.

Pro Tip: Prioritise cloud partners with insurance-specific security certifications and proven compliance track records. Generic cloud providers lack understanding of regulatory requirements unique to insurance. Look for vendors who demonstrate expertise in insurance cloud security and can guide you through jurisdiction-specific compliance requirements.

The cloud adoption obstacles that seem insurmountable often reflect lack of clear strategy rather than genuine technical limitations. Organisations that succeed treat cloud adoption as business transformation, not IT projects.

Choosing the right deployment: SaaS, multi-cloud, and hybrid models

Understanding your obstacles is key, but choosing the right deployment model can be a real differentiator. Each approach offers distinct advantages depending on your organisation’s priorities.

SaaS solutions accelerate time-to-market dramatically. Pre-built insurance platforms eliminate months of development work. Vendors handle infrastructure management, security patches, and feature updates. Your teams focus on configuration and business rules rather than technical maintenance. More insurers now prefer buying SaaS over building custom solutions, reflecting the maturity of available platforms.

Multi-cloud and hybrid approaches provide flexibility and risk management. Distributing workloads across providers prevents vendor lock-in. Hybrid models let you keep sensitive data on-premises whilst leveraging cloud scalability for customer-facing applications. This flexibility comes with increased complexity in management and integration.

| Deployment model | Best for | Key advantage | Primary challenge |

|---|---|---|---|

| SaaS | Insurers seeking rapid deployment | Fastest time-to-value | Limited customisation |

| Single cloud | Organisations prioritising simplicity | Unified management | Vendor dependency |

| Multi-cloud | Large insurers with diverse needs | Flexibility and resilience | Integration complexity |

| Hybrid | Regulated markets with data residency rules | Control over sensitive data | Higher operational overhead |

Your deployment decision should follow this framework:

- Assess compliance requirements—data residency rules may mandate specific approaches

- Evaluate integration needs—existing systems and partner connections influence architecture

- Determine customisation requirements—unique product offerings may require flexible platforms

- Calculate total cost of ownership—include ongoing management, not just initial implementation

- Consider organisational capabilities—match complexity to your team’s skills and capacity

A multi-core strategy in insurance often makes sense for larger organisations with diverse product lines. Different business units can operate on platforms optimised for their specific needs whilst sharing data through integration layers. Smaller insurers typically benefit more from standardised SaaS platforms that deliver immediate capability.

The debate between single and multi-cloud continues, but the right answer depends entirely on your specific context. Prioritise solving actual business problems over pursuing architectural purity.

The future: AI and cloud synergy in insurance operations

Selecting the right deployment is necessary, but what truly sets future-ready insurers apart is how they leverage cloud and AI together. This combination unlocks capabilities that transform competitive positioning.

Advanced AI and analytics depend fundamentally on cloud scalability. Machine learning models require massive computational resources during training. Real-time inference engines need instant access to current data across multiple sources. Traditional on-premises infrastructure simply cannot deliver the elasticity and performance these workloads demand. Eighty per cent of P&C insurers already use predictive pricing, and AI adoption will double or triple by 2028.

“Cloud infrastructure doesn’t just enable AI—it makes advanced analytics economically viable for insurers of all sizes, democratising capabilities once available only to the largest carriers.”

Practical use cases delivering value today include:

- Predictive pricing that adjusts rates based on real-time risk factors and market conditions

- Automated claims processing using computer vision to assess damage from photos

- Fraud detection systems that identify suspicious patterns across millions of transactions

- Customer personalisation engines that recommend coverage based on life events and behaviour

- Underwriting assistants that surface relevant risk factors from unstructured data sources

These applications free your staff from routine tasks, allowing them to focus on complex cases requiring human judgement. Claims adjusters spend time on disputed cases rather than straightforward approvals. Underwriters evaluate unusual risks instead of processing standard applications. Customer service representatives handle sensitive situations whilst chatbots manage routine enquiries.

Thirty-seven per cent of insurers are actively exploring Generative AI, recognising its potential for document generation, policy summarisation, and customer communication. Early adopters are using large language models to draft policy documents, generate claims summaries, and provide instant answers to complex coverage questions.

The synergy between AI automation in insurance and cloud infrastructure creates compounding advantages. Better data accessibility improves model accuracy. Faster processing enables real-time decision-making. Scalable infrastructure supports experimentation without major capital investment. Understanding AI’s impact on insurance helps you prioritise initiatives that deliver measurable business value.

Accelerate your cloud journey with the right partner

By aligning cloud and AI strategies, insurers have a clear runway for operational and competitive gains—now see how the right solution bridges vision and execution. Selecting a partner with deep insurance expertise accelerates your transformation whilst reducing implementation risk.

IBSuite provides purpose-built platforms for property and casualty insurers seeking to modernise operations without sacrificing control. Our policy administration platform enables rapid product launches through configurable rules engines and API-first architecture. Insurers using IBSuite reduce time-to-market for new products from months to weeks, responding quickly to market opportunities.

Claims management transforms when you leverage cloud claims management capabilities designed specifically for P&C workflows. Automated routing, integrated communication, and real-time analytics give your teams the tools they need to deliver exceptional customer experiences whilst controlling costs. The platform scales effortlessly during catastrophe events, maintaining performance when you need it most.

Our clients benefit from Evergreen updates that deliver new capabilities without disruptive upgrade projects. Built on AWS infrastructure, IBSuite provides enterprise-grade security and compliance whilst maintaining the flexibility insurers need to differentiate. We understand the unique challenges P&C insurers face because insurance is all we do.

Ready to explore how cloud-native platforms can transform your operations? Book a demo to see IBSuite in action and discuss your specific requirements with our insurance technology specialists.

Frequently asked questions

What are the main barriers to cloud adoption in insurance?

Key challenges include high costs and expertise needs, integration complexity with legacy systems, data privacy concerns, and organisational resistance to change. Successful insurers address these through phased approaches and strategic vendor partnerships.

Is cloud adoption in insurance secure and compliant?

With proper partners and controls, public cloud solutions meet industry and regional compliance requirements. Integration and data concerns slow some market segments, but leading cloud providers offer insurance-specific security certifications and proven compliance frameworks.

Which insurance functions benefit most from cloud adoption?

Claims management, underwriting, distribution, and analytics see the sharpest efficiency gains. Scalability for these functions drives growth, with cloud enabling rapid processing during peak demand and seamless integration with partner systems.

How does AI adoption interact with cloud strategy for insurers?

Cloud infrastructure enables rapid AI rollout by providing the computational power and data accessibility advanced analytics require. Insurers leveraging this combination achieve 6-point lower combined ratios and 3-point higher premium growth compared to peers relying on traditional infrastructure.

Recommended

- Optimizing Cloud Insurance Platforms for P&C Success

- Cloud Scalability in Insurance: Enabling Rapid Growth

- Drivers of Digital Transformation in the Insurance Industry – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Why Modernizing Insurance Systems is Crucial for Growth – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System