15.05.26

How digital billing transforms insurance operations

Billing is the moment an insurer’s promise meets cold, hard reality. Yet most P&C organisations still treat it as a back-office function, something that happens after the real work is done. That framing is costly. Your billing platform touches every policyholder, every payment cycle, and every renewal decision. It shapes cash flow, fuels compliance reporting, and either builds or quietly erodes customer trust. This guide cuts through the noise to explain why digital billing deserves a seat at the strategic table, what modern platforms must actually do, and how your organisation can evaluate the right path forward.

Table of Contents

- Why digital billing matters for insurance

- Core functions of digital billing in P&C insurance

- Comparing digital billing approaches: in-house, vendor, legacy

- Strategic benefits: efficiency, compliance, engagement

- What most insurers miss about digital billing transformation

- See digital billing in action

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Billing’s strategic role | Modern digital billing drives operational efficiency and customer trust for insurers. |

| Edge case readiness | Robust solutions must handle proration, compliance, fraud, and payment retries. |

| Avoiding hidden costs | In-house and legacy platforms can conceal true costs and hinder agility. |

| Benefits of API-first approach | API-driven digital billing unifies workflows and enables real-time adaptability. |

| Integrated transformation | Connecting policy, claims, and billing creates seamless customer and business outcomes. |

Why digital billing matters for insurance

Billing is not simply about collecting premiums. It is the operational heartbeat of a P&C insurer. When it works well, it is invisible. When it fails, the consequences ripple outward: delayed cash settlements, compliance exposure, frustrated policyholders, and inflated administrative costs.

The billing systems and efficiency connection is well established, yet many insurers still underinvest here. Consider what a billing failure actually costs. A single payment error can trigger a cancellation notice, prompt a policyholder complaint, and require manual intervention from two or three teams to resolve. Multiply that across thousands of policies and the cost becomes structural, not incidental.

Digital billing addresses this at the root. Real-time payment processing, automated dunning sequences, and self-service portals reduce inbound query volumes significantly. Policyholders who can view their schedule, update payment methods, and download statements without calling a contact centre are measurably more satisfied. The billing automation benefits for P&C carriers are therefore both financial and reputational.

Key areas where billing directly affects strategic outcomes include:

- Cash flow predictability: Automated retry logic and real-time reconciliation reduce days sales outstanding and improve forecasting accuracy.

- Customer retention: Billing errors are a leading cause of avoidable churn. Transparent, accurate statements reduce disputes and build loyalty.

- Regulatory posture: Jurisdictional rules around notice periods, grace periods, and fee disclosures are increasingly stringent. Manual processes cannot keep pace reliably.

- Operational cost: Every manual exception handled by a billing team is overhead that could be eliminated with the right platform design.

“The true cost of billing is rarely visible on a spreadsheet. It hides in exception queues, reconciliation cycles, and the customer complaints that never quite get attributed to a billing root cause.”

Pro Tip: When assessing your current billing process impact, audit the number of manual touchpoints per billing cycle. That figure alone will tell you more about your real cost structure than any vendor comparison.

As legacy batch systems cause fragmentation versus modern API-first architectures, the gap between digital-native carriers and those running older platforms widens every quarter. The urgency is real.

Core functions of digital billing in P&C insurance

Digital billing in property and casualty insurance is structurally more complex than billing in most other financial services sectors. The combination of regulatory variation, mid-term policy changes, and the diversity of payment instruments creates a demanding operational environment.

A mature digital billing platform must handle all of the following without manual intervention:

- Proration and mid-term recalculation: When a policyholder adds a vehicle, changes coverage, or cancels mid-term, the billing engine must recalculate charges instantly and accurately across the remaining period.

- Payment failure management: Expired cards, insufficient funds, and bank errors all require intelligent retry logic. The platform must attempt retries at optimal intervals and escalate appropriately without triggering unnecessary cancellations.

- Multi-jurisdictional compliance: Premium tax rates, statutory notice requirements, and grace period rules vary by state or territory. The billing engine must apply the correct rules automatically based on policy location.

- Instalment plan administration: Insurers commonly offer monthly, quarterly, and annual payment options. Each carries its own fee structure, down payment rules, and reconciliation requirements.

- Volume management during surge periods: Renewal cycles and catastrophe events can spike billing transaction volumes significantly. The platform must scale without degradation.

- Fraud detection integration: Unusual payment patterns, sudden method changes, and high-value transactions warrant real-time screening rather than batch-mode review.

“Edge cases such as mid-term endorsements requiring prorated recalculations, payment failures needing retry logic, multi-jurisdictional compliance, volume spikes, and fraud detection are not peripheral concerns. They are the daily operational reality for any P&C billing team.”

The billing process efficiency conversation often stalls at high-level automation promises. The real differentiator is how well a platform handles the edge cases. A generic payment processor can manage a standard card transaction. It cannot manage a mid-term endorsement on a commercial lines policy in a multi-state programme. That distinction is where insurers either gain or lose competitive ground.

The billing automation guide for P&C operations makes this point clearly: automation without insurance-specific logic is automation that creates new exceptions rather than eliminating existing ones.

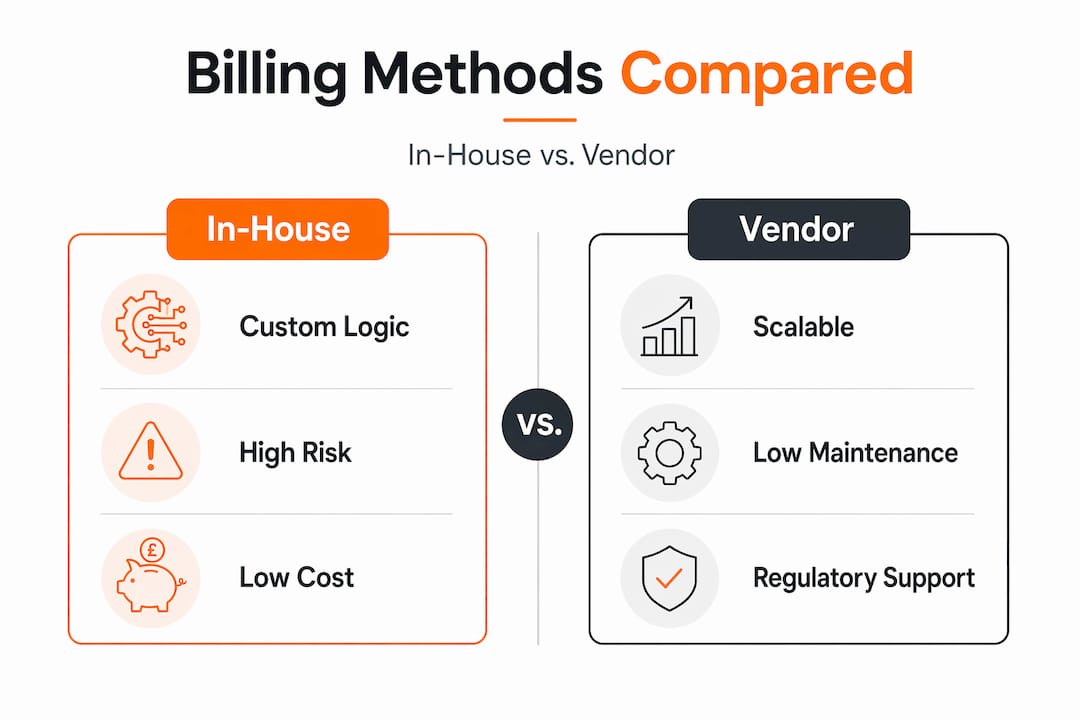

Comparing digital billing approaches: in-house, vendor, legacy

When evaluating billing transformation, most insurance leaders consider three broad options: build in-house, engage a third-party payments vendor, or adopt a cloud-native, API-first insurance platform. Each has genuine trade-offs.

| Approach | Initial cost | Insurance-specific logic | Scalability | Long-term risk |

|---|---|---|---|---|

| In-house build | Low to medium | Fully customisable | Limited by internal capacity | High (maintenance, exceptions) |

| Generic payment vendor | Low | Minimal | High | Medium (compliance gaps) |

| Legacy batch system | Sunk cost | Partial | Poor | Very high (fragmentation) |

| API-first insurance platform | Medium to high | Comprehensive | High | Low |

The in-house route is frequently presented as the cost-effective choice, particularly for carriers with established development teams. However, cheapest in-house models lead to hidden costs through exceptions, reconciliations, and compliance remediation that accumulate year over year. What appears to be a controlled investment in year one often becomes an ongoing operational liability by year three.

Generic payment vendors handle transaction processing competently. They do not handle insurance-specific regulatory intelligence. They cannot automatically apply a state-mandated grace period or calculate the correct proration for a mid-term coverage change. Carriers that rely solely on payment vendors typically build a layer of custom logic on top, effectively recreating the in-house problem they were trying to avoid.

Legacy batch systems present the starkest risk. Processing billing in batches means data is always slightly stale, reconciliations are periodic rather than continuous, and real-time service requests cannot be fulfilled accurately. The API-first approach replaces this model with event-driven, real-time data flows that keep billing, policy, and claims records synchronised at all times.

Pro Tip: When you streamline billing operations, the most important question is not “what does this platform cost?” but rather “what does our current platform cost us in exceptions, manual reconciliations, and compliance risk?” That reframe almost always changes the decision criteria significantly.

The organisations that move furthest fastest are those that treat billing modernisation as a platform decision rather than a procurement exercise. The architecture matters enormously.

Strategic benefits: efficiency, compliance, engagement

The business case for digital billing consolidates around three themes: operational efficiency, regulatory compliance, and customer engagement. Each is measurable, and each compounds the value of the others.

Operational efficiency is the most immediately visible benefit. Straight-through processing rates rise when billing logic is automated and integrated with the policy administration system. Exception queues shrink. Reconciliation cycles that previously required overnight batch runs can be completed in real time. Finance teams gain accurate, current data rather than working from yesterday’s numbers.

| Metric | Legacy billing environment | Digital billing platform |

|---|---|---|

| Manual exceptions per 1,000 transactions | 15 to 25 | 2 to 5 |

| Reconciliation cycle time | Daily or weekly batch | Real-time or near real-time |

| Average payment failure resolution time | 3 to 5 days | Same day |

| Customer self-service availability | Limited or none | 24/7 via portal or app |

Regulatory compliance shifts from a reactive overhead to a built-in capability. Modern platforms maintain jurisdictional rule sets as part of their ongoing update cycles. When a state changes its grace period requirement or introduces a new premium tax category, the platform updates automatically rather than requiring a development sprint. This is the critical distinction between insurance billing processes built for compliance versus those that retrofit it.

Customer engagement is where billing’s strategic potential is most underappreciated. A billing portal is one of the most frequently visited digital touchpoints an insurer has with its policyholders. Investing in clarity, self-service, and proactive communication at that touchpoint builds trust that marketing spend cannot replicate.

Key customer-facing benefits include:

- Transparent billing statements that clearly itemise premiums, taxes, fees, and endorsements.

- Proactive notifications for upcoming payments, failed transactions, and renewal changes.

- Flexible payment options including digital wallets, bank transfers, and instalment management.

- Instant confirmation of payment receipts and coverage status updates.

As fragmented systems and manual exceptions drive higher costs and increased risk, the carriers that consolidate their billing within an integrated platform gain compounding advantages. The efficiency savings fund further investment; the compliance automation reduces risk exposure; and the customer experience improvements reduce churn. The cycle reinforces itself.

Proactive fraud analytics in billing is also increasingly viable when billing data flows through a unified platform. Integrated analytics can identify unusual payment patterns in real time, flagging potential fraud before losses are incurred rather than after.

What most insurers miss about digital billing transformation

Here is the uncomfortable truth that most billing transformation programmes avoid: technology selection is necessary but not sufficient. The organisations that fail to see meaningful returns from billing modernisation are almost always those that replaced a legacy system with a modern one without redesigning the workflows around it.

Billing transformation is not a technology project. It is a business process redesign project that happens to involve technology. The distinction matters enormously when you are scoping investment, assembling teams, and setting success criteria.

The exceptions are where this becomes clear. Most billing platforms can handle the standard cases well. The test of a genuinely transformed operation is what happens when a commercial policyholder requests a mid-term cancellation with a return premium, whilst simultaneously disputing a prior payment and requesting a change of billing contact. That scenario involves billing, policy administration, finance, and customer service. If those systems are not integrated, the process fragments immediately.

Legacy batch systems cause fragmentation precisely because they were designed to process transactions in isolation rather than as part of a connected operational workflow. Modern platforms eliminate that isolation, but only if the implementation genuinely connects the data flows.

The second thing most insurers miss is the importance of transparency as a design principle. Policyholders do not need perfect billing. They need billing they can understand, query, and act on. A clear self-service portal that shows exactly what is owed, why, and when builds more loyalty than a flawlessly accurate back-office system that customers never see.

Future-state billing should prioritise three characteristics above all others: transparency in every customer interaction, flexibility to adapt to new products and regulatory changes without bespoke development, and ongoing engagement that keeps billing moments from feeling adversarial. The organisations driving digital efficiency in their billing operations are those that designed for the customer journey first and the transaction processing second.

Real transformation means fewer manual reconciliations, fewer exception queues, and more time for billing teams to focus on genuinely complex cases that require human judgement. That is the goal. The technology is the enabler, not the outcome.

See digital billing in action

Understanding the strategic case for digital billing is one thing. Seeing how it connects to your existing policy and claims infrastructure is another. IBSuite from IBA brings billing, policy administration, and claims management onto a single API-first platform, eliminating the fragmentation that drives manual exceptions and compliance risk. Every billing event is connected to the policy record in real time, giving your teams accurate data when they need it rather than after the next batch run. If your organisation is ready to move from back-office billing to a genuine strategic capability, book a digital insurance demo and see how IBSuite handles the edge cases your current platform is struggling with.

Frequently asked questions

How does digital billing support regulatory compliance for insurers?

Digital billing systems embed jurisdictional rules directly into the processing engine, automatically applying the correct grace periods, notice requirements, and tax calculations for each policy location. As multi-jurisdictional compliance is one of the most demanding edge cases in P&C billing, this built-in capability dramatically reduces both manual oversight and compliance exposure.

What’s the biggest risk with in-house billing solutions?

The primary risk is hidden cost accumulation over time, particularly in exception handling, reconciliation cycles, and compliance remediation. As in-house models lead to hidden costs through exceptions and delays, what appears cost-effective at launch typically becomes a significant ongoing liability as the policy book grows and regulatory requirements evolve.

How can digital billing help reduce fraud in insurance?

Modern integrated billing platforms enable real-time analytics across payment streams, allowing unusual patterns to be flagged and reviewed before losses occur rather than identified retrospectively. Volume spikes and fraud detection are core operational concerns that digital billing platforms are specifically designed to address through continuous monitoring rather than batch-mode review.

Why do legacy batch billing systems present a problem today?

Batch processing means data is always delayed, reconciliations are periodic, and real-time customer service requests cannot be accurately fulfilled. Legacy batch systems cause fragmentation that undermines both operational agility and the integrated data flows that modern insurance platforms require to function effectively.