Why Choose an Insurance Platform for P&C Success

Nearly 80 percent of Central European insurers now rely on digital platforms to sharpen their competitive edge. The pressure to keep pace with British standards of customer service and operational efficiency means the choice of insurance platform holds major consequences. This article distills core definitions, platform types, and key capabilities, helping Chief Information Officers navigate the complex options that shape bottom-line performance and regulatory success.

Table of Contents

- Defining Insurance Platforms In Today’s Market

- Types Of Insurance Platforms And Delivery Models

- Core Capabilities Driving Operational Efficiency

- Regulatory Compliance And Integration Considerations

- Business Impacts: Cost, Agility, And Risk Reduction

- Evaluating Alternatives To Insurance Platforms

Key Takeaways

| Point | Details |

|---|---|

| Importance of Modern Insurance Platforms | These platforms are essential for digital transformation in the insurance sector, integrating advanced technologies to enhance operations and customer engagement. |

| Diverse Delivery Models | Insurance platforms feature various delivery models, such as cloud-based SaaS and API-first core platforms, each suited to different operational needs. |

| Operational Efficiency Drivers | Key capabilities include automated workflows and predictive analytics, which streamline processes and improve insurers’ responsiveness to market changes. |

| Regulatory Compliance Necessity | The integration of robust compliance mechanisms is vital for insurers to navigate complex regulatory landscapes while maintaining operational effectiveness. |

Defining Insurance Platforms in Today’s Market

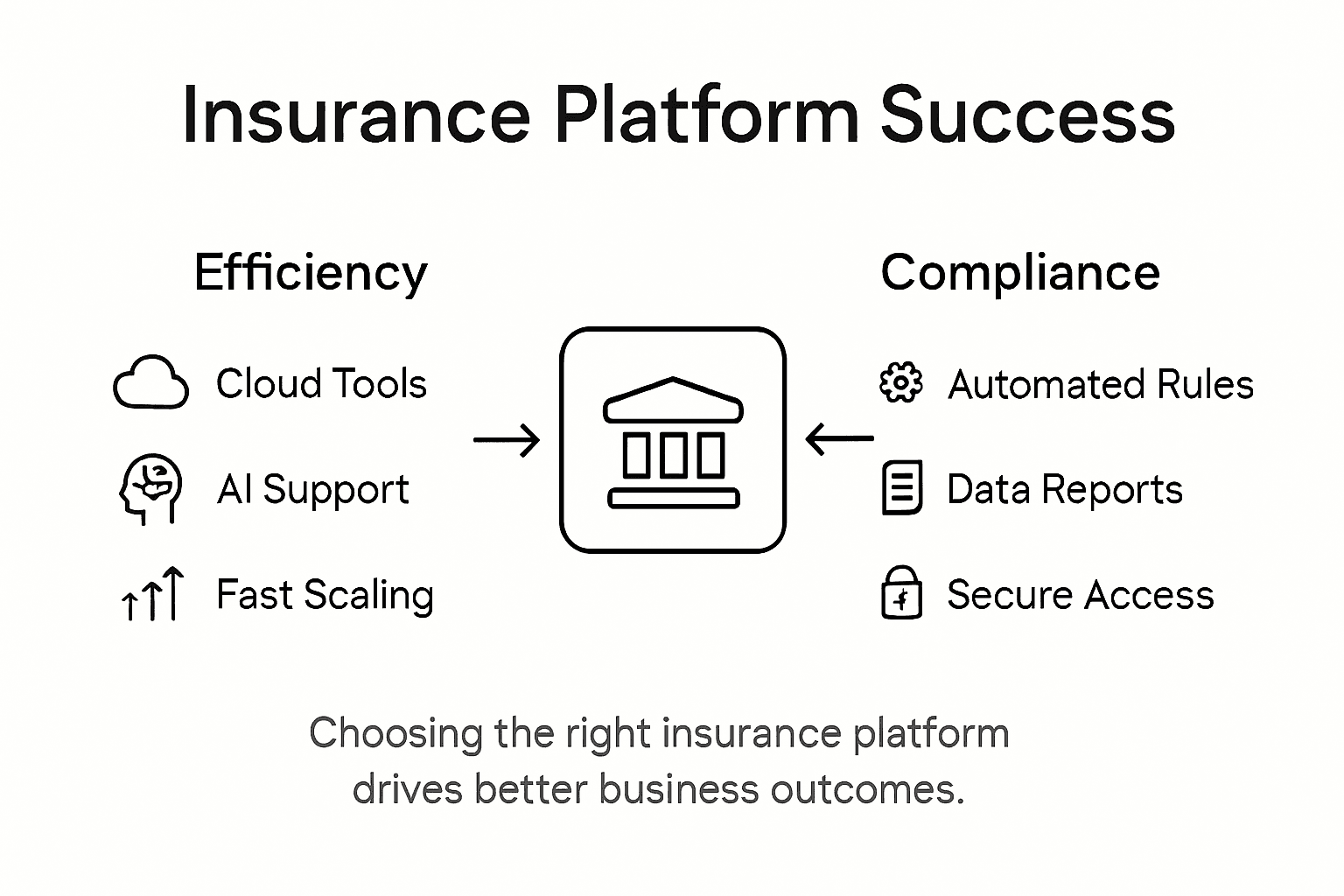

Insurance platforms represent sophisticated digital ecosystems that are fundamentally reshaping how property and casualty (P&C) insurers operate in the European market. According to the European Insurance and Occupational Pensions Authority (EIOPA), these platforms are integral to digital transformation, enabling insurers to leverage advanced technologies like artificial intelligence, Internet of Things (IoT), and blockchain for enhanced product development and customer service.

At their core, insurance platforms function as comprehensive technological infrastructure that seamlessly integrates multiple functions across the insurance value chain. The Geneva Association’s 2024 digital platform report highlights how these platforms facilitate business model innovation by connecting insurers with customers through sophisticated digital channels. They support multiple distribution models, ranging from traditional physical networks to fully digital interactions, allowing European insurers to adapt rapidly to changing market dynamics.

The strategic value of modern insurance platforms lies in their ability to address critical industry challenges. Key capabilities include:

- Streamlined operational processes

- Enhanced data analytics capabilities

- Flexible product configuration

- Improved customer engagement tools

- Robust regulatory compliance mechanisms

These platforms are not merely technological solutions but strategic enablers that empower insurers to compete effectively in an increasingly digital marketplace.

Pro tip: When evaluating insurance platforms, prioritise solutions that offer seamless integration, scalability, and comprehensive API capabilities to future-proof your digital transformation strategy.

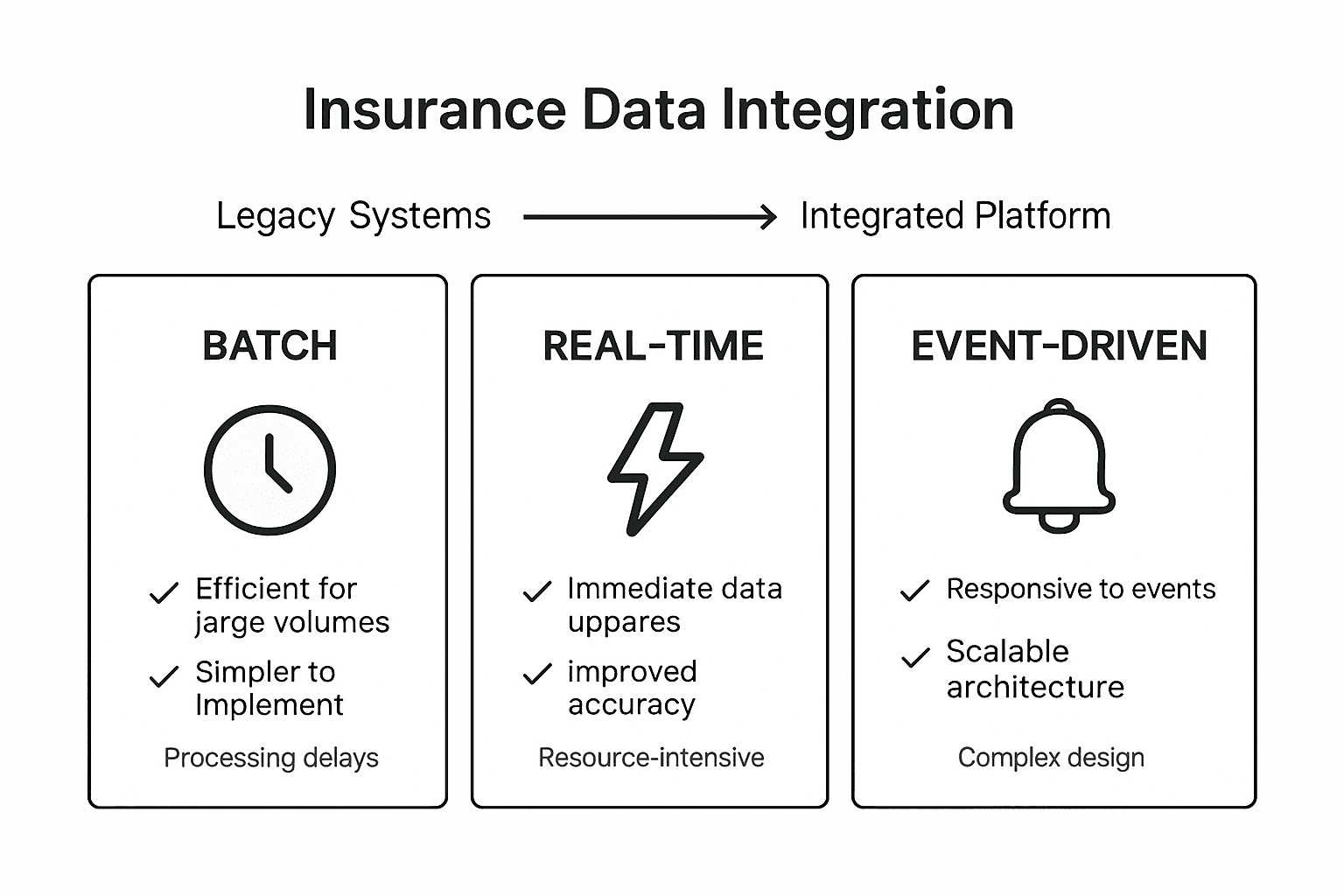

Types of Insurance Platforms and Delivery Models

Insurance platforms have evolved into diverse delivery models that cater to the complex needs of modern European insurers. The ISG Pulse Check 2024 report categorises these platforms across three primary delivery approaches: cloud-based Software as a Service (SaaS), API-first core platforms, and hybrid integration models, each designed to address unique technological and operational requirements.

Academic research from MDPI reveals a sophisticated landscape of platform types, highlighting three distinct models that are transforming the insurance ecosystem. These include traditional broker-intermediated platforms, pure digital platforms, and emerging multi-sided platforms that dynamically blend various roles and functionalities. Each model offers distinctive advantages:

- Broker-Intermediated Platforms: Maintain traditional distribution channels

- Pure Digital Platforms: Offer end-to-end digital experiences

- Multi-Sided Platforms: Enable complex interactions between multiple stakeholders

Cloud-based and API-first platforms are particularly significant for European insurers, providing unprecedented flexibility in product configuration, customer engagement, and regulatory compliance. These models enable insurers to rapidly adapt to market changes, integrate emerging technologies, and create more personalised insurance experiences.

Pro tip: When selecting an insurance platform, assess its scalability, integration capabilities, and alignment with your specific operational architecture to ensure long-term digital transformation success.

Below is a comparison of insurance platform delivery models and their primary business impacts:

| Platform Model | Key Advantage | Main Limitation |

|---|---|---|

| Cloud-Based SaaS | Rapid deployment, low upfront costs | May have less customisation |

| API-First Core | High integration flexibility | Requires advanced IT strategy |

| Hybrid Integration | Balances legacy and new tech | Can introduce complexity |

| Traditional Broker-Intermediated | Supports established networks | Slower digital adoption |

| Pure Digital | Fully automated processes | May exclude some demographics |

| Multi-Sided | Broad ecosystem interaction | Governance can be complex |

Core Capabilities Driving Operational Efficiency

Modern insurance platforms are transforming operational efficiency through advanced technological capabilities that fundamentally reshape how insurers manage their core business processes. The EIOPA 2024 publication highlights critical capabilities including cloud computing, AI-driven analytics, and automated workflows that dramatically enhance insurers’ ability to streamline complex operational tasks.

Integrated data management stands at the forefront of these capabilities, enabling insurers to consolidate disparate information sources and generate actionable insights. Key operational efficiency drivers include:

- Predictive underwriting models

- Automated claims processing

- Real-time customer service tools

- Centralized regulatory reporting mechanisms

- Dynamic product configuration systems

ISG’s comprehensive platform analysis-2024.pdf?sfvrsn=2debd431_2) emphasises that modern platforms provide unprecedented flexibility through cloud and API connectivity. These technologies enable insurers to rapidly adapt their operational infrastructure, reduce manual intervention, and create more responsive, intelligent business processes that can quickly adjust to regulatory and market changes.

The convergence of advanced technologies like artificial intelligence, machine learning, and comprehensive data analytics is revolutionising how European insurers approach operational efficiency. By leveraging these sophisticated platform capabilities, organisations can significantly reduce operational costs, minimise processing times, and create more personalised customer experiences.

Pro tip: Prioritise insurance platforms with robust API integration and modular design to ensure maximum operational flexibility and future scalability.

Regulatory Compliance and Integration Considerations

Regulatory compliance represents a critical challenge for European insurers seeking to modernise their technological infrastructure. Comprehensive research from academic preprints reveals the intricate landscape of EU regulatory frameworks affecting digital insurance platforms, emphasising the complex requirements surrounding data protection, consumer rights, and Solvency II standards.

Key regulatory integration considerations for Central European insurers include:

- Ensuring GDPR data protection compliance

- Maintaining transparent consumer protection mechanisms

- Implementing robust audit trail capabilities

- Supporting comprehensive regulatory reporting standards

- Enabling operational resilience through integrated controls

The EIOPA report on digital insurance sector transformation underscores the importance of platforms that facilitate seamless regulatory adherence. Modern insurance platforms must provide automated compliance monitoring, dynamic reporting capabilities, and flexible architectural designs that can rapidly adapt to evolving regulatory landscapes.

Successful integration demands a holistic approach that balances technological innovation with stringent compliance requirements. Insurers must select platforms capable of embedding regulatory controls directly into core operational processes, ensuring continuous alignment with complex European regulatory standards.

Pro tip: Prioritise insurance platforms with built-in compliance automation and configurable regulatory reporting modules to minimise manual intervention and reduce compliance risks.

Business Impacts: Cost, Agility, and Risk Reduction

Business transformation in the insurance sector increasingly depends on platforms that deliver measurable operational advantages. The Geneva Association’s comprehensive digital platform research demonstrates how modern insurance platforms generate substantial value through strategic cost reduction, enhanced organisational agility, and sophisticated risk management capabilities.

Three primary business impacts distinguish contemporary insurance platforms:

- Cost Efficiency: Dramatically reducing operational overhead

- Organisational Agility: Enabling rapid market responsiveness

- Risk Mitigation: Improving underwriting accuracy and compliance

ISG’s 2024 industry survey reveals that Central European insurers prioritise platforms delivering quantifiable business outcomes. Specifically, these platforms generate value by streamlining core processes, reducing IT maintenance expenditure, and providing flexible technological infrastructure that supports rapid product development and seamless partner integrations.

Modern insurance platforms represent more than technological solutions—they are strategic enablers that transform traditional operational models. By leveraging advanced data analytics, cloud computing, and intelligent automation, insurers can create more responsive, efficient, and resilient business ecosystems that adapt quickly to evolving market dynamics.

Pro tip: Conduct a comprehensive total cost of ownership analysis when evaluating insurance platforms, focusing on long-term efficiency gains and strategic flexibility rather than just initial implementation expenses.

Evaluating Alternatives to Insurance Platforms

Strategic technology selection in the insurance sector requires careful consideration of various implementation approaches. Comprehensive market analysis from DataIntelo explores the complex landscape of alternatives to integrated insurance platforms, highlighting critical trade-offs between point solutions, legacy system upgrades, and custom in-house software development.

Key alternative approaches to comprehensive insurance platforms include:

- Point Solutions: Addressing specific functional needs

- Legacy System Upgrades: Incrementally improving existing infrastructure

- Custom In-House Development: Creating bespoke technological solutions

- Cloud-Based Microservices: Implementing modular architectural strategies

Market research from OMR Global suggests that while these alternatives offer niche advantages, they often fall short in delivering the comprehensive benefits of integrated platforms. Central European insurers must carefully evaluate their digital maturity, regulatory requirements, and long-term strategic objectives when considering technological alternatives.

The primary challenges with alternative approaches include limited scalability, increased compliance complexity, and higher long-term maintenance costs. Insurers frequently discover that seemingly cost-effective solutions ultimately require significant additional investment to achieve the flexibility and comprehensive functionality provided by modern integrated platforms.

Pro tip: Conduct a thorough total cost of ownership analysis that extends beyond initial implementation, considering long-term scalability, integration challenges, and potential regulatory compliance constraints.

The table below summarises how integrated insurance platforms compare with alternative approaches:

| Approach | Long-Term Cost Profile | Scalability | Regulatory Alignment |

|---|---|---|---|

| Integrated Platform | Lower total cost | High, future-ready | Automated compliance tools |

| Point Solution | Rising maintenance cost | Limited scope | Manual checks needed |

| Legacy Upgrade | Incremental costs | Medium, constrained | Potential for gaps |

| Custom In-House | Unpredictable cost | Custom scalability | Varies with resources |

| Microservices | Efficient for modular tasks | High, but integration required | Depends on orchestration |

Unlock P&C Success with a Future-Ready Insurance Platform

The challenges outlined in the article highlight the urgent need for Property and Casualty insurers to adopt scalable, API-first, and cloud-native insurance platforms that streamline operations, enhance regulatory compliance, and enable rapid product innovation. Many insurers struggle with outdated legacy systems, costly manual compliance, and limited agility in responding to evolving market demands. If your goal is to achieve operational efficiency, seamless integration, and customer-centric digital transformation, it is crucial to select a platform designed to future-proof your business.

Insurance Business Applications (IBA) offers IBSuite, a secure, end-to-end solution trusted by global leaders and built specifically for the challenges you face. IBSuite supports the entire insurance value chain—from underwriting and claims to billing and CRM—while delivering Evergreen updates that maintain regulatory compliance without disruption. With IBSuite’s robust cloud infrastructure and comprehensive API capabilities, you can reduce IT complexity and launch innovative products faster. Learn how IBSuite can transform your operations by exploring our demo booking page, then discover the benefits of a platform tailored for your needs on Insurance Business Applications.

Make your next move towards agility and growth today. Book a demo to see how IBSuite can empower your P&C business to outperform competitors and thrive in a digital-first market.

Frequently Asked Questions

What are the main benefits of using an insurance platform for property and casualty insurance?

Utilising an insurance platform enhances operational efficiency, provides advanced data analytics, and improves customer engagement. It allows insurers to streamline processes, adapt to market changes, and ensure regulatory compliance effectively.

How do different types of insurance platforms compare in terms of flexibility and operational efficiency?

Insurance platforms can vary significantly, with cloud-based solutions offering rapid deployment and lower costs, while API-first platforms provide high integration flexibility. Traditional broker-intermediated platforms may support established structures but can lag in digital adoption compared to pure digital or multi-sided platforms that offer comprehensive benefits.

What role does regulatory compliance play in selecting an insurance platform?

Regulatory compliance is critical when selecting an insurance platform. It is essential to choose a platform that provides automated compliance monitoring and adaptable reporting capabilities to ensure alignment with evolving regulatory standards and to simplify adherence to data protection and consumer rights regulations.

How can integrating advanced technologies improve the performance of an insurance platform?

Integrating advanced technologies like artificial intelligence, machine learning, and IoT into an insurance platform can significantly enhance its operational efficiency. These technologies enable predictive modelling, automated claims processing, and real-time customer service, leading to cost reductions and improved customer experiences.

Recommended

- Complete Guide to Integrated Insurance Platforms – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Why Choose End-to-End Platforms for Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Opportunities and Challenges for P&C Insurers: Embracing Insurtech – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- 7 Types of P&C Insurance Distribution for Insurers

- LD Financial Services | Final Expenses Insurance | Life Insurance | Retirement Planning