17.04.26

Why policy administration is critical for efficient P&C ops

TL;DR:

- Modern policy administration systems can reduce manual processing by up to 70 percent.

- Effective PAS enhances speed, accuracy, customer loyalty, and profitability for insurers.

- Limitations include handling complex edge cases and regulatory variability, requiring strategic integration.

Modern policy administration systems (PAS) can reduce manual processing by up to 70%, yet many insurers still treat this function as routine back-office overhead. That assumption is costly. Policy administration is the operational spine of every property and casualty (P&C) insurer, governing everything from initial policy issuance through endorsements, renewals, and cancellations. Get it right and you gain speed, accuracy, and customer loyalty. Get it wrong and you face ballooning expense ratios, compliance failures, and frustrated policyholders. This guide covers the full scope of policy administration, the technology reshaping it, its direct business impact, its real limitations, and why it deserves a seat at the strategic table.

Table of Contents

- Core functions of policy administration in P&C insurance

- How technology is reshaping policy administration

- Business impact: Efficiency, costs, and profitability

- Limits, edge cases, and emerging challenges

- A strategic view: Policy administration as the insurer’s competitive differentiator

- Explore leading solutions for policy administration transformation

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Automation drives efficiency | Modern policy administration systems can reduce manual tasks by up to 70%. |

| Profitability gains | Efficient policy administration directly boosts underwriting profits and lowers combined ratios. |

| Strategic differentiator | When optimised, policy administration becomes a lever for growth and customer loyalty. |

| Know the system limits | Even advanced platforms require human oversight for complex, nuanced scenarios. |

Core functions of policy administration in P&C insurance

Policy administration is the set of processes, rules, and systems that govern a policy’s entire lifecycle, from the moment a quote converts to a bound policy through every change, payment, and eventual termination. For P&C insurers, this lifecycle is rarely linear. It branches constantly, responding to endorsement requests, mid-term adjustments, audit obligations, and regulatory mandates that vary by jurisdiction.

Understanding policy administration basics starts with mapping the key lifecycle stages:

- Policy issuance: Binding coverage, generating documents, and confirming premium terms.

- Endorsements: Processing mid-term changes to coverage, limits, or insured details.

- Renewals: Re-underwriting and re-rating expiring policies within defined timeframes.

- Cancellations and reinstatements: Managing terminations, statutory notices, and potential reinstatements.

- Audits: Reconciling estimated premiums against actual exposure for commercial lines.

Each stage involves multiple operational touchpoints. Underwriters set the risk appetite and pricing parameters. Servicing teams handle policyholder queries and documentation. Finance reconciles premium receipts. Compliance monitors adherence to state and national filing requirements. A PAS connects all of these functions, acting as the single source of truth for every policy record.

Knowing how to read an insurance policy reveals just how much structured data a PAS must manage: coverage forms, exclusions, conditions, endorsement schedules, and premium calculations all coexist within a single document set.

| Policy lifecycle stage | Primary operational owner | Key PAS function |

|---|---|---|

| Issuance | Underwriting | Document generation, premium calculation |

| Endorsement | Servicing | Mid-term rating, document update |

| Renewal | Underwriting/Servicing | Re-rating, renewal offer generation |

| Cancellation | Servicing/Compliance | Notice generation, return premium |

| Audit | Finance/Underwriting | Exposure reconciliation, adjustment billing |

However, a PAS is not omniscient. Research shows that a PAS excels at transaction-level accuracy and throughput but struggles with portfolio aggregation, executive reporting, and handling nuanced definitions across departments. This distinction matters enormously when you are building a technology architecture that needs to serve both operational and strategic needs.

How technology is reshaping policy administration

The gap between legacy and modern policy administration is not merely a question of user interface. It is a fundamental difference in architecture, capability, and business agility. Legacy systems, often built on monolithic code bases from the 1990s or early 2000s, require lengthy development cycles to accommodate even minor product changes. Modern cloud-native platforms operate on a different logic entirely.

Automation in P&C insurance has moved from a competitive advantage to a baseline expectation. Modern PAS platforms now automate renewal invitations, endorsement processing, document generation, and compliance checks without human intervention. The result is measurable: routine task automation reduces manual processing by up to 70%, improving operational efficiency, accuracy, and compliance across the board.

Pro Tip: When evaluating a new PAS, ask vendors to demonstrate their no-touch renewal rate on a commercial lines portfolio. This single metric reveals more about genuine automation maturity than any product brochure.

Artificial intelligence is adding another layer of precision. Machine learning models now flag anomalous endorsement requests, identify potential fraud prevention signals during policy servicing, and recommend optimal renewal terms based on loss history. These capabilities were simply unavailable to insurers running on legacy infrastructure.

| Capability | Legacy PAS | Modern cloud-native PAS |

|---|---|---|

| Product configuration | Requires IT development | Configurable by business users |

| Renewal automation | Largely manual | High no-touch rates |

| Compliance updates | Slow, costly patches | Evergreen, automatic updates |

| Integration | Point-to-point, brittle | API-first, flexible |

| Reporting | Batch, delayed | Real-time dashboards |

The modern insurance platform benefits extend well beyond efficiency. Customer satisfaction improves when policyholders receive accurate documents instantly, endorsements are processed within minutes rather than days, and renewal communications arrive on time with correct pricing. These are not soft metrics. They translate directly into retention rates and net promoter scores.

Business impact: Efficiency, costs, and profitability

For insurance executives, the most persuasive argument for investing in policy administration technology is the bottom-line impact. The drivers of digital transformation in insurance are increasingly tied to measurable financial outcomes, not aspirational digital strategies.

Consider the industry context. P&C combined ratios improved to 96.9% in 2024, with net premiums written reaching $934 billion, and technology-driven operational efficiencies are a recognised contributor to that improvement. A combined ratio below 100% means underwriting profitability. Every percentage point improvement represents hundreds of millions of dollars across the industry.

“Efficient policy administration is not just an operational goal. It is an underwriting profitability lever that most insurers have yet to fully exploit.”

The direct financial benefits of best-in-class policy administration include:

- Lower cost per policy: Automation reduces the labour cost associated with routine transactions, cutting cost per policy significantly in high-volume personal lines portfolios.

- Faster time-to-bind: Streamlined workflows reduce quote-to-bind cycle times, improving conversion rates and reducing the risk of losing business to faster competitors.

- Reduced error rates: Automated data validation at point of entry prevents costly downstream corrections, re-issuances, and coverage disputes.

- Improved renewal retention: Accurate, timely renewal processing directly supports retention, and a 5% improvement in retention can dramatically increase portfolio profitability.

- Audit accuracy: For commercial lines, precise audit processing reduces premium leakage and disputes with policyholders.

Pro Tip: Map your current cost per policy by line of business before any PAS investment. This baseline makes ROI conversations with your board far more concrete and credible.

Technology also enables underwriting profitability improvements by ensuring that rating engines apply the correct factors consistently, eliminating the pricing inconsistencies that erode margins in manual environments. Automated underwriting further tightens the link between risk selection and premium adequacy, supporting a healthier portfolio over time.

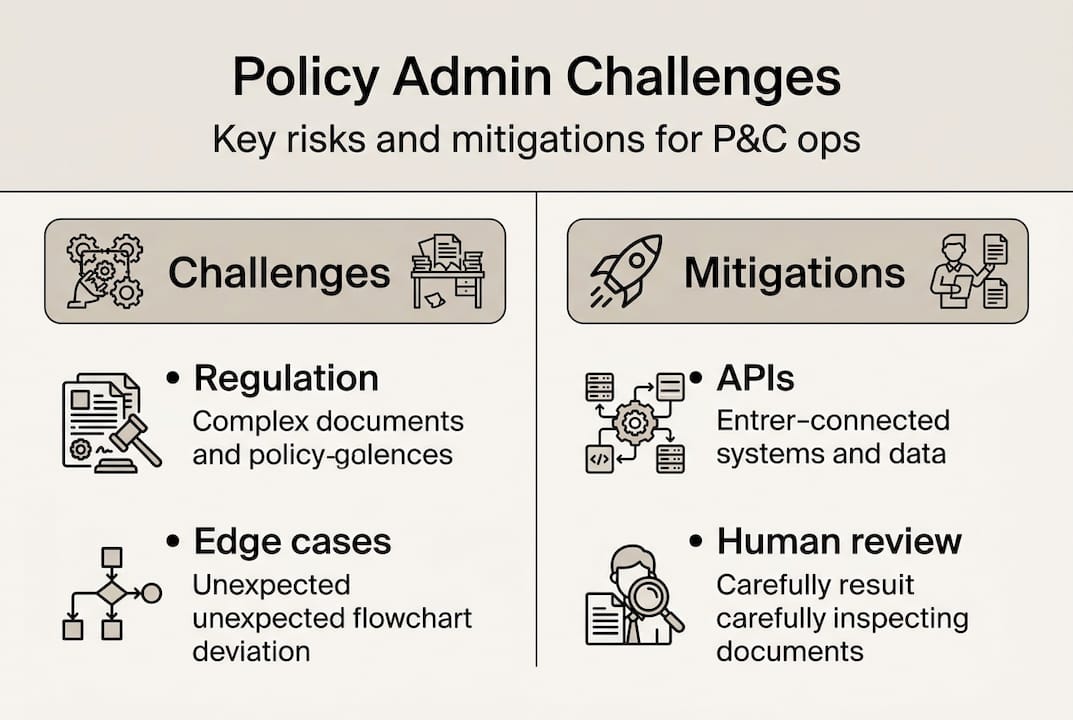

Limits, edge cases, and emerging challenges

No technology discussion is complete without an honest assessment of limitations. Even the most sophisticated PAS platforms have boundaries, and understanding them is essential for building a resilient operating model.

Policy admin best practices consistently highlight the importance of identifying edge cases before they become operational crises. Research confirms that edge cases in PAS include multi-year policies spanning accounting boundaries, retroactive endorsements, rescinded cancellations, complex premium structures involving instalments and audits, in-flight transactions, and state-specific regulatory variations.

These are not rare occurrences in a mature P&C portfolio. They are everyday realities for commercial lines, specialty, and surplus lines insurers.

Common PAS limitation categories:

- Portfolio aggregation: Most PAS are optimised for individual policy transactions, not cross-portfolio analytics or executive dashboards.

- Regulatory variability: State-specific filing requirements, form mandates, and rate approval processes create complexity that generic systems handle poorly.

- Complex premium structures: Instalment plans, audit-based premiums, and retrospective rating programmes often require custom configuration or workarounds.

- Retroactive changes: Backdated endorsements and rescinded cancellations can create accounting and compliance complications that automated workflows struggle to resolve cleanly.

| Challenge area | Risk if unmanaged | Mitigation approach |

|---|---|---|

| Regulatory variation | Non-compliance, fines | Jurisdiction-specific rule engines |

| Retroactive endorsements | Accounting errors | Human override workflows |

| Portfolio reporting | Poor executive visibility | Separate BI/analytics layer |

| In-flight transactions | Data integrity issues | Transaction locking protocols |

An API-first approach in insurance addresses many of these limitations by enabling seamless integration between the PAS and specialist tools for analytics, regulatory compliance, and complex rating. Rather than forcing a single system to do everything, a composable architecture assigns each function to the tool best suited for it. Guidance on regulatory handling in policy admin further reinforces the need for structured escalation paths when automated processes reach their boundaries.

Human override capability is not a sign of system weakness. It is a deliberate design choice that separates mature platforms from brittle ones.

A strategic view: Policy administration as the insurer’s competitive differentiator

Most insurance executives view policy administration as infrastructure, necessary but unglamorous, akin to plumbing. This framing is both understandable and strategically dangerous. The insurers pulling ahead in competitive markets are those who have recognised that their PAS is not a cost centre. It is a growth engine.

Speed-to-market for new products is determined almost entirely by how configurable your policy administration environment is. Customer net promoter scores (NPS) are heavily influenced by the accuracy and timeliness of policy documents and endorsement processing. Portfolio agility, the ability to enter or exit lines of business quickly, depends on how modular your administration architecture is.

We have seen insurers launch new commercial products in weeks rather than months simply by modernising their administration layer. That is not a technology story. That is a revenue story. The insurance billing automation benefits that flow from a modern PAS further compound the commercial advantage, reducing billing disputes and improving cash flow predictability.

Our advice to C-suite leaders is direct: elevate policy administration planning to the same strategic level as product development and distribution strategy. The operational and financial returns are not incremental. They are transformational.

Explore leading solutions for policy administration transformation

For P&C insurers ready to move beyond legacy constraints, IBSuite by Insurance Business Applications (IBA) delivers a cloud-native, API-first platform that covers the full policy lifecycle with genuine automation depth and configurability. Built on AWS and trusted by global carriers, IBSuite enables insurers to reduce manual effort, accelerate product launches, and maintain compliance across jurisdictions without costly custom development. Whether you are modernising a personal lines book or scaling a complex commercial portfolio, IBA’s consultative approach ensures the platform fits your operational reality. Book a policy administration demo to see how IBSuite can transform your administration capabilities and deliver measurable results.

Frequently asked questions

What is policy administration in insurance?

Policy administration covers all core policyholder transactions from issuance to renewal, including endorsements, audits, and cancellations. A PAS provides transaction-level accuracy and throughput across every stage of the policy lifecycle.

How does automation benefit policy administration?

Automation in policy administration can reduce manual processing by up to 70%, directly boosting operational efficiency, reducing error rates, and improving regulatory compliance across the portfolio.

What limitations do policy administration systems have?

Even advanced systems may struggle with edge cases such as multi-year policies, rescinded cancellations, and state-specific regulatory variations, often requiring integration with specialist tools or human override workflows.

How does policy administration affect profitability?

Efficient policy administration lowers cost per policy and reduces errors that erode margins. P&C combined ratios improved to 96.9% in 2024, with technology-driven efficiencies recognised as a key contributing factor to underwriting profitability.

Recommended

- Why is insurance product management critical to obtain speed to value for insurers? – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- 7 Policy Administration Best Practices for Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Streamline policy management for insurance success

- Top insurance CRM features to boost P&C retention

- How to Prevent Insurance Fraud: A Practical Guide