Insurance companies once relied on gut instinct and guesswork to set prices but things have changed fast. Now, modern rating engines can process thousands of calculations per second and turn mountains of risk data into precise prices. That power goes beyond just number crunching. It is quietly reshaping who gets the best deals and how fast insurance companies react to risk.

Table of Contents

- What Are Rating Engines In Insurance?

- Why Rating Engines Matter To Insurers

- How Rating Engines Work: Key Concepts And Processes

- The Role Of Technology In Modern Rating Engines

- Challenges And Innovations In Rating Engine Development

Quick Summary

| Takeaway | Explanation |

|---|---|

| Rating engines automate premium calculations | They leverage complex algorithms to analyze risk factors and streamline pricing decisions for insurers. |

| Real-time data enhances pricing accuracy | Rating engines can adjust premiums based on current risk patterns, improving competitiveness and profitability. |

| Integration of AI boosts risk assessment | Advanced machine learning techniques allow engines to refine their models continuously, increasing predictive accuracy. |

| Dynamic pricing strategies offer competitive edges | Insurers can adjust pricing quickly in response to market changes, enhancing customer satisfaction. |

| Challenges include system integration and data standardization | Insurers face difficulties in updating legacy systems and ensuring compliance while developing effective rating engines. |

What Are Rating Engines in Insurance?

Rating engines are sophisticated software systems that serve as the computational heart of insurance pricing strategies. These powerful algorithmic tools enable insurers to calculate precise insurance premiums by evaluating multiple risk variables simultaneously. Insurance rating engines transform complex underwriting data into actionable pricing models that balance risk assessment and competitive market positioning.

Core Components of Rating Engines

A rating engine integrates several critical components to generate accurate premium calculations. These typically include:

- Risk assessment algorithms

- Policyholder demographic analysis

- Historical claims data processing

- Geographical risk mapping

- Predictive modeling techniques

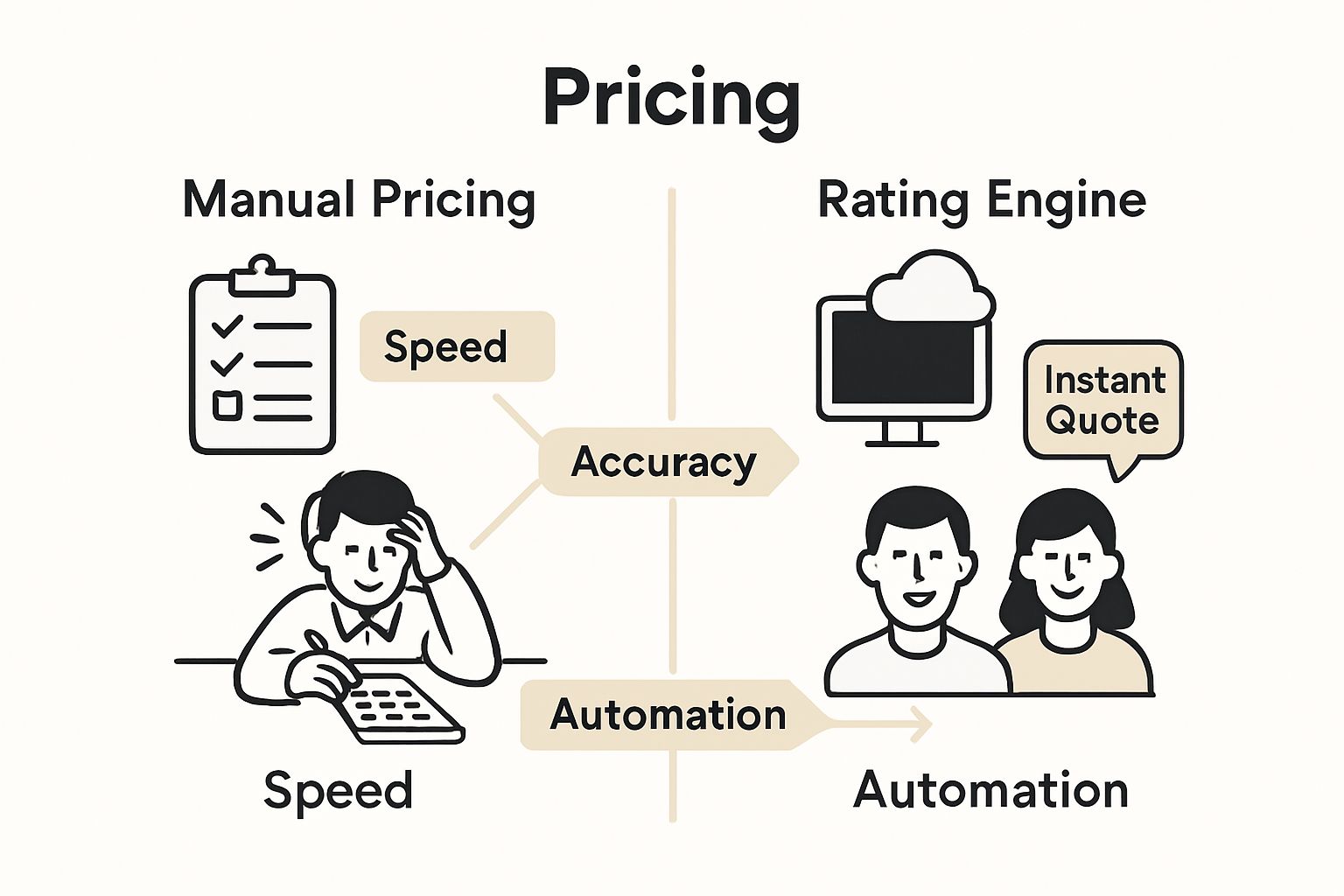

Insurers rely on these advanced computational systems to automate pricing decisions, reducing human error and standardizing premium calculations across different insurance products. By leveraging extensive data points, rating engines can quickly assess an individual’s or business’s risk profile and generate pricing that reflects their unique characteristics.

Technical Mechanics of Premium Calculation

The technical process involves complex mathematical models that analyze multiple variables simultaneously. An insurance rating engine might consider factors like:

- Age and personal history

- Credit score indicators

- Property characteristics

- Previous insurance claims

- Geographical location risks

These variables are weighted and processed through sophisticated algorithms that generate precise premium recommendations.

Modern rating engines can process thousands of calculations per second, enabling real-time pricing adjustments. Read more about our digital insurance platform’s rating capabilities to understand how technology transforms insurance pricing strategies.

The ultimate goal of a rating engine is to create fair, data-driven pricing models that protect both the insurance provider and the policyholder by accurately reflecting potential risks and financial exposures.

Why Rating Engines Matter to Insurers

Rating engines represent more than just technological solutions they are strategic instruments that fundamentally transform how insurance companies approach risk management and pricing strategies. Digital transformation in insurance systems has made these computational tools essential for competitive survival in a rapidly evolving market.

Strategic Business Advantages

Insurers gain substantial strategic advantages by implementing sophisticated rating engines.

These systems enable organizations to:

These systems enable organizations to:

- Develop precise risk assessment models

- Accelerate product development cycles

- Reduce operational expenses

- Enhance pricing accuracy

- Improve customer experience through personalized pricing

The ability to rapidly analyze complex datasets allows insurers to make more informed decisions, ultimately leading to better financial outcomes and reduced potential for underwriting losses.

Economic Impact and Competitive Edge

Modern rating engines provide insurers with a significant competitive advantage by enabling dynamic pricing strategies. By processing massive amounts of data in milliseconds, these systems allow companies to adjust premiums instantly based on emerging risk patterns. Learn more about our insurance platform’s automation capabilities to understand how technology drives strategic decision making.

Moreover, rating engines help insurers manage financial risks more effectively. They can quickly identify potential high-risk scenarios, adjust pricing models proactively, and maintain profitability even in volatile market conditions. The precision of these computational tools means insurers can offer more competitive rates while simultaneously protecting their bottom line.

Ultimately, rating engines are not just technological tools but strategic assets that enable insurance companies to navigate complex risk landscapes with unprecedented accuracy and efficiency.

How Rating Engines Work: Key Concepts and Processes

Rating engines function as sophisticated computational frameworks that transform raw data into precise insurance pricing strategies. Insurance rating systems utilize complex algorithms to convert multidimensional risk information into actionable premium calculations with remarkable accuracy and speed.

Data Processing and Risk Segmentation

The core functionality of rating engines revolves around comprehensive data processing and intelligent risk segmentation. These systems analyze extensive datasets by breaking down risk factors into granular components:

- Individual policyholder characteristics

- Historical claims performance

- Geographic and environmental variables

- Asset and property specifications

- Statistical probability models

By systematically evaluating these interconnected variables, rating engines create nuanced risk profiles that enable insurers to develop precise pricing models tailored to specific policyholder segments.

Algorithmic Calculation Mechanisms

Modern rating engines employ advanced mathematical models that integrate multiple calculation techniques. The algorithmic process involves several critical steps:

- Data normalization and standardization

- Weighted risk factor analysis

- Predictive modeling and statistical inference

- Real-time computational processing

- Dynamic pricing adjustments

These sophisticated computational strategies allow insurers to generate instantaneous premium recommendations that reflect current market conditions and individual risk characteristics. Explore our comprehensive approach to digital insurance platforms to understand how technology transforms complex risk assessment processes.

The ultimate objective of these intricate algorithmic mechanisms is to create a fair, transparent, and dynamically responsive pricing ecosystem that balances risk mitigation with competitive market positioning. By leveraging advanced computational techniques, rating engines represent a pivotal technological innovation in modern insurance strategy.

The Role of Technology in Modern Rating Engines

Technology has revolutionized rating engines, transforming them from static calculation tools into dynamic, intelligent systems capable of processing complex risk assessments in real time. Advanced machine learning techniques in insurance have dramatically expanded the computational capabilities of these critical insurance platforms.

Artificial Intelligence and Machine Learning Integration

Modern rating engines leverage cutting-edge technological innovations to enhance risk prediction and pricing accuracy. Key technological advancements include:

- Neural network algorithms

- Predictive analytics frameworks

- Real-time data processing capabilities

- Advanced statistical modeling

- Adaptive learning mechanisms

These technological approaches enable rating engines to continuously refine their risk assessment models by learning from historical data patterns and emerging market trends, creating increasingly sophisticated pricing strategies.

Cloud Computing and Data Architecture

Cloud-based infrastructures have fundamentally transformed how rating engines operate, providing unprecedented computational power and scalability. These technological platforms offer insurers:

- Massive parallel processing capabilities

- Secure, distributed data storage

- Instant scalability of computational resources

- Enhanced data integration across multiple sources

- Reduced infrastructure maintenance costs

Explore our approach to digital insurance transformation to understand how technological innovation drives strategic competitive advantages. By embracing these advanced technological frameworks, insurers can develop more responsive, accurate, and personalized rating mechanisms that adapt quickly to changing market dynamics and individual risk profiles.

To clarify the key technologies that empower modern rating engines, the following table compares their distinct roles and benefits within insurance pricing systems.

| Technology Component | Description | Benefit to Insurers |

|---|---|---|

| Artificial Intelligence & Machine Learning | Uses data-driven modeling and predictive analytics | Enhances risk assessment and pricing accuracy |

| Neural Networks | Complex pattern recognition through interconnected nodes | Adapts to new risk patterns in real time |

| Predictive Analytics Frameworks | Statistical models projecting future events | Anticipates claims and sets proactive pricing |

| Real-Time Data Processing | Immediate analysis of incoming data | Enables instant pricing adjustments |

| Cloud Computing | Distributed, scalable computational resources | Ensures flexibility and cost-effective scaling |

| Secure Data Storage | Protected repositories for sensitive insurance data | Maintains regulatory compliance and privacy |

Challenges and Innovations in Rating Engine Development

Rating engine development represents a complex technological frontier where insurers continuously balance sophisticated computational capabilities with evolving market demands. Insurance technology modernization requires strategic approaches to overcome significant technological and operational challenges.

Technological Integration Complexities

Developing advanced rating engines involves navigating intricate technological landscapes that demand seamless integration across multiple systems. Key challenges include:

- Legacy system compatibility

- Data standardization across diverse sources

- Real-time computational performance

- Security and privacy compliance

- Scalable architectural design

Successful rating engine development requires robust technological frameworks that can adapt to changing regulatory environments and integrate complex data processing requirements while maintaining computational efficiency and accuracy.

Emerging Innovative Strategies

Insurers are implementing innovative strategies to address rating engine development challenges through advanced technological approaches:

- Microservices architecture

- Containerized computational models

- Adaptive machine learning algorithms

- Modular rating configuration platforms

- Decentralized data processing frameworks

Learn about digital transformation in insurance platforms to understand how technological innovations are reshaping risk assessment methodologies. These emerging strategies enable insurers to develop more flexible, responsive rating engines that can quickly adapt to market changes and individual policyholder requirements.

The future of rating engine development lies in creating intelligent, interconnected systems that can process complex risk variables with unprecedented speed and precision, ultimately delivering more accurate and personalized insurance pricing strategies.

To enhance understanding of the specific challenges and solutions in rating engine development, the following table organizes major obstacles alongside innovative strategies already being adopted by insurers.

| Challenge | Description | Innovative Strategy | Benefit |

|---|---|---|---|

| Legacy System Compatibility | Integrating new engines with old technology | Microservices Architecture | Facilitates seamless integration |

| Data Standardization | Aligning diverse data sources | Modular Rating Platforms | Increases flexibility and adaptability |

| Real-Time Performance | Maintaining fast, reliable computations | Containerized Models | Boosts scalability and responsiveness |

| Regulatory Compliance | Ensuring data privacy and security | Decentralized Processing | Enhances security and reliability |

| Scalability | Expanding computational resources as needs grow | Cloud-Based Infrastructure | Provides instant resource scaling |

Transform Your Insurance Rating with the Power of IBSuite

Are you struggling with outdated rating systems that cannot keep up with fast-moving risk environments and personalized pricing demands? The article highlighted how modern rating engines rely on cutting-edge data processing, predictive modeling, and seamless system integration to deliver fair and dynamic insurance premiums. Many insurers find their legacy technology limits their ability to automate pricing, offer tailored products, and adapt to new market challenges.

This is where Insurance Business Applications (IBA) steps in. IBSuite empowers you to bring advanced rating logic, API-first integrations, and cloud scalability all into one secure platform. Take your rating engine to the next level with real-time data analytics, automation, and effortless compliance. See how IBSuite supports the full P&C value chain by requesting your personalized demo now. Experience firsthand how you can accelerate digital transformation and stay competitive today. Do not let inefficient rating hold back your growth—book a guided walkthrough and discover what true modernization looks like.

Frequently Asked Questions

What is a rating engine in insurance?

A rating engine is a software system that calculates insurance premiums using various risk variables. To understand how it works, review the core components such as risk assessment algorithms and policyholder demographic analysis.

How do rating engines improve insurance premium calculations?

Rating engines enhance premium calculations by analyzing multiple data points simultaneously, which reduces human error and increases accuracy. Consider evaluating your current pricing strategies by incorporating an advanced rating engine model to see improvements in pricing speed and precision.

What factors do rating engines consider when calculating premiums?

Rating engines take into account variables like age, credit score, property characteristics, and historical claims data. Review these factors systematically to ensure comprehensive risk assessments that reflect the unique profile of each policyholder.

How can insurance companies benefit from implementing a rating engine?

Implementing a rating engine allows insurers to develop precise risk models, enhance customer experience, and reduce operational expenses. To gain an advantage, focus on integrating real-time pricing adjustments to stay competitive in the market.

What challenges do insurers face in developing rating engines?

Key challenges include legacy system compatibility, data standardization, and ensuring compliance with security regulations. Address these challenges by developing a robust technological framework that can adapt to changing requirements and enhance computational efficiency.

How can technology improve rating engines in insurance?

Technology improves rating engines by enabling real-time data processing, predictive analytics, and machine learning integration. Explore and apply these cutting-edge technologies to continuously refine risk assessment models and ensure more accurate pricing strategies.

Recommended

- Automation and Artificial Intelligence in P&C Insurance – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Rating – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Understanding the Impact of AI in Insurance 2025 – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- 6 Types of Insurance Platforms You Should Know – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Engine Optimization Meaning: Clear Benefits Unveiled

Each phase should have clear milestones, resource allocations, and specific technological interventions. Consider developing a multi-year strategy that allows for flexibility and iterative improvements while maintaining a consistent vision.

Each phase should have clear milestones, resource allocations, and specific technological interventions. Consider developing a multi-year strategy that allows for flexibility and iterative improvements while maintaining a consistent vision.