20.03.26

What is a digital insurance marketplace: a guide for 2026

Many insurance executives confuse digital insurance marketplaces with aggregators, missing critical distinctions that impact transformation strategies. Whilst aggregators simply compare consumer quotes, marketplaces enable full B2B workflows including underwriting, binding, and compliance for property and casualty insurers. Understanding these differences matters in 2026 as digital marketplaces reshape P&C insurance, cutting time to market by half and reducing operational costs by 30 to 40 per cent. This guide clarifies what digital insurance marketplaces are, their unique role in P&C transformation, and why they represent a strategic advantage for brokers, managing general agents, and carriers seeking competitive edge through rapid innovation and operational excellence.

Table of Contents

- Defining Digital Insurance Marketplaces And Their Distinction From Aggregators

- Impact Of Digital Insurance Marketplaces On Property And Casualty Insurance

- Nuances And Challenges Of Digital Insurance Marketplaces In 2026

- Implementing Digital Insurance Marketplaces: Strategies For P&C Executives And Digital Leaders

- Discover IBSuite’s Policy Administration Platform

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Marketplaces versus aggregators | Digital insurance marketplaces support end-to-end B2B workflows for commercial and P&C insurance, whilst aggregators focus on consumer price comparison for personal lines. |

| Transformation impact | Marketplaces reduce time to market by 50 per cent and operational costs by 30 to 40 per cent through digitisation and automation. |

| AI underwriting advantage | AI-enhanced underwriting in marketplaces improves combined ratios by 3 to 6 points, directly boosting profitability. |

| Implementation priorities | API-first, cloud-native architectures enable faster launches, flexible integrations, and scalable ecosystem partnerships. |

| MGA innovation engine | Asset-light MGA models leveraging marketplaces outperform traditional carriers, doubling market growth in recent years. |

Defining digital insurance marketplaces and their distinction from aggregators

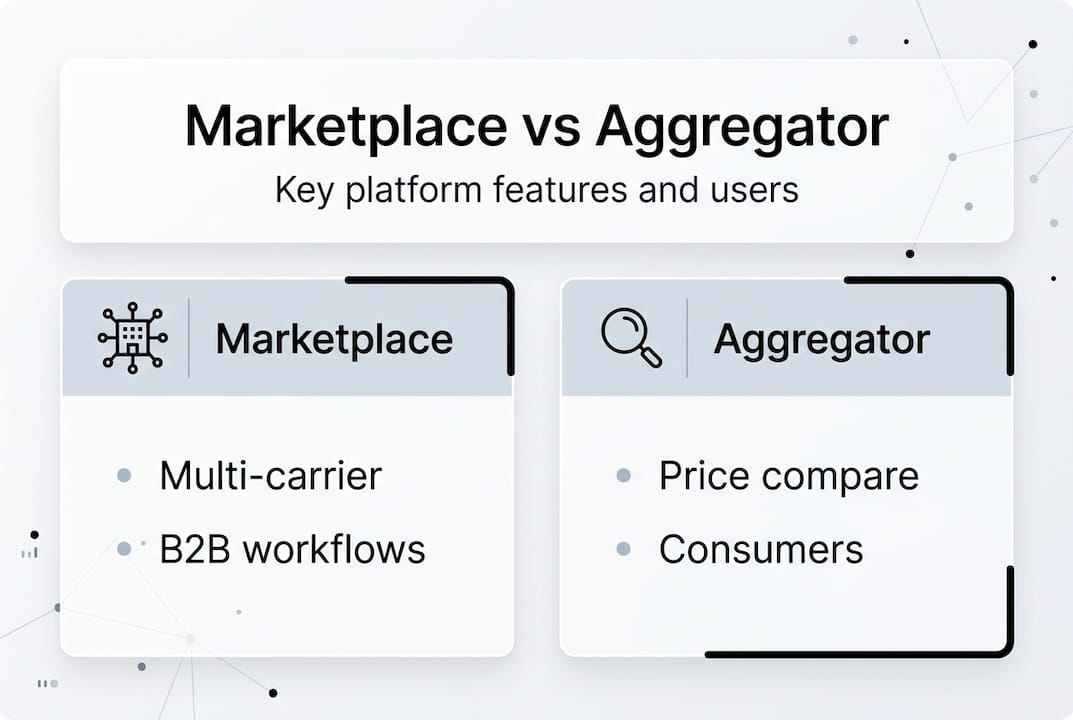

Digital insurance marketplaces are B2B platforms that enable multi-carrier placement, data validation, underwriting, binding, and compliance workflows for commercial and property and casualty insurance. They serve brokers, managing general agents, and carriers by digitising the entire insurance lifecycle from quote to claim. Aggregators focus on consumer quote comparison, whilst marketplaces enable full B2B workflows including underwriting, binding, and compliance.

Aggregators primarily serve personal lines customers seeking price comparisons across multiple carriers. They display quotes side by side, allowing consumers to select the cheapest option. Marketplaces operate at a fundamentally different level, integrating deeply with carrier systems through APIs to automate underwriting rules, validate complex risk data, and facilitate binding authority for brokers and MGAs.

This distinction matters enormously for P&C insurance digital strategy. Aggregators commoditise simple products through price competition. Marketplaces enable sophisticated risk placement, regulatory compliance, and operational efficiency for complex commercial lines. Understanding this difference helps executives identify the right technology investments for their transformation roadmaps.

| Feature | Aggregator | Marketplace |

|---|---|---|

| Primary users | Individual consumers | Brokers, MGAs, carriers |

| Insurance focus | Personal lines | Commercial and P&C |

| Core function | Quote comparison | End-to-end placement and binding |

| Integration depth | Surface-level display | Deep API connections with underwriting |

| Revenue model | Lead generation fees | Transaction and subscription fees |

| Compliance support | Limited | Comprehensive regulatory workflows |

API-first insurance platforms underpin successful marketplaces, enabling rapid carrier onboarding and flexible product launches. Executives evaluating digital transformation should prioritise platforms supporting true marketplace capabilities rather than simple aggregation.

Pro Tip: When assessing marketplace vendors, test their API documentation quality and carrier integration speed as key indicators of platform maturity and operational readiness.

Impact of digital insurance marketplaces on property and casualty insurance

Digital insurance marketplaces are transforming P&C insurance by dramatically accelerating time to market and reducing operational costs. Marketplaces reduce time to market by 50 per cent and operational costs by 30 to 40 per cent through process digitisation and automation. These improvements stem from eliminating manual data entry, automating underwriting rules, and streamlining compliance workflows across multiple carriers.

Time savings materialise through parallel processing of submissions across carriers, automated risk assessment, and instant policy issuance. Traditional placement processes requiring days or weeks now complete in hours. Operational cost reductions come from reduced administrative overhead, fewer errors requiring rework, and improved straight-through processing rates. Brokers and MGAs report productivity gains of 40 per cent or more after adopting marketplace platforms.

AI-enhanced underwriting represents another critical advantage. Combined ratios improve by 3 to 6 points when insurers leverage AI models within marketplace workflows. Machine learning algorithms analyse vast datasets to identify risk patterns invisible to traditional underwriting, enabling more accurate pricing and better loss ratios. This profitability improvement directly impacts carrier competitiveness and financial performance.

Reliability and uptime matter enormously for business-critical insurance operations. Leading marketplaces maintain 99.9 per cent uptime, supporting continuous business operations without disruption. This reliability enables brokers to serve clients confidently and carriers to process high volumes during peak periods.

Key marketplace benefits for P&C transformation include:

- Accelerated product launches enabling faster response to market opportunities

- Enhanced broker and MGA productivity through workflow automation

- Improved risk selection and pricing accuracy via AI underwriting

- Reduced IT complexity through standardised API integrations

- Better customer experience with faster quotes and binding

- Scalable infrastructure supporting growth without proportional cost increases

Automation and AI in P&C insurance extend beyond underwriting to claims processing, fraud detection, and customer service. Marketplaces serve as integration hubs enabling these AI capabilities across the insurance value chain. Executives should view marketplaces not merely as distribution channels but as strategic platforms enabling comprehensive digital transformation.

Nuances and challenges of digital insurance marketplaces in 2026

Whilst digital insurance marketplaces deliver substantial benefits, executives must navigate real challenges to achieve successful adoption. Understanding both opportunities and obstacles enables realistic planning and risk mitigation strategies.

Marketplaces excel at enabling ecosystem partnerships and MGA growth. The MGA market has doubled in recent years, with MGAs outperforming traditional carriers as innovation engines. Asset-light MGA models leveraging marketplace infrastructure launch products faster and adapt more quickly to market changes than legacy carriers burdened by technical debt. This ecosystem enablement represents a fundamental strength of marketplace platforms.

However, full-stack direct-to-consumer models struggle within marketplace ecosystems. Building complete insurance operations from scratch whilst competing on price proves difficult. Successful marketplace participants focus on specific strengths, whether underwriting expertise, distribution reach, or technology capabilities, rather than attempting vertical integration.

Integration complexity poses significant challenges. Connecting legacy carrier systems to modern marketplace APIs requires substantial technical effort and change management. Data format inconsistencies, varying business rules across carriers, and regulatory compliance requirements multiply integration difficulties. Many transformation initiatives underestimate the time and resources required for successful integration.

AI adoption faces particular hurdles. Seventy-four per cent of AI pilots fail to scale beyond initial proof-of-concept stages. Talent shortages hamper progress, with insufficient data scientists, machine learning engineers, and AI specialists available to support ambitious transformation programmes. Organisations struggle to move from experimental AI projects to production-grade systems delivering measurable business value.

Key challenges include:

- Technical integration complexity with legacy systems

- Talent shortages in AI, data science, and modern architecture skills

- Change management resistance within traditional insurance organisations

- Data quality issues preventing effective AI model training

- Regulatory compliance across multiple jurisdictions

- Vendor selection complexity with rapidly evolving marketplace landscape

Pro Tip: Prioritise partnerships with vendors offering comprehensive integration support and proven implementation methodologies rather than attempting complex integrations with internal resources alone.

Integration challenges in insurance marketplaces require strategic approaches combining technology upgrades, skills development, and phased implementation plans. Successful organisations invest in API-first architectures that simplify future integrations and reduce technical debt accumulation.

Balancing innovation ambition with realistic capability assessment proves critical. Executives should benchmark their organisation’s digital maturity against industry standards before committing to aggressive marketplace adoption timelines. Phased approaches starting with specific product lines or distribution channels reduce risk whilst building internal capabilities and confidence.

Implementing digital insurance marketplaces: strategies for P&C executives and digital leaders

Successful marketplace implementation requires strategic focus on architecture, vendor selection, AI capabilities, and business model considerations. These practical strategies guide investment decisions and transformation roadmaps.

Prioritising API-first, cloud-native platforms delivers maximum flexibility and speed. API-first architectures enable 50 per cent faster launches compared to traditional integration approaches. Cloud-native design provides elastic scalability, automatic updates, and reduced infrastructure management overhead. These architectural choices fundamentally determine transformation success and long-term operational efficiency.

Benchmarking against leading platforms establishes realistic expectations and identifies capability gaps. Solutions from vendors like Guidewire, Duck Creek, and specialised marketplace providers offer different strengths. ROI achievable within 12 months when organisations select platforms aligned with their specific needs and implementation capabilities. Comparing total cost of ownership, integration complexity, and vendor support quality informs better decisions.

Leveraging AI and machine learning for data enrichment and underwriting closes critical capability gaps. Focus on AI/ML data enrichment and underwriting to improve risk selection and pricing accuracy. Starting with specific use cases like automated risk scoring or fraud detection builds momentum and demonstrates value before expanding to more complex applications.

Considering asset-light MGA and B2B SaaS models offers strategic alternatives to full-stack carrier operations. MGAs leveraging marketplace infrastructure avoid capital-intensive carrier infrastructure whilst maintaining underwriting control and product innovation capabilities. This business model flexibility enables faster market entry and reduced operational complexity.

Essential implementation steps:

- Assess current digital maturity and identify specific capability gaps requiring marketplace solutions

- Define clear business objectives with measurable success criteria for marketplace adoption

- Evaluate vendor platforms against technical requirements, integration complexity, and total cost of ownership

- Pilot marketplace integration with a single product line or distribution channel to validate approach

- Invest in skills development for API integration, data engineering, and AI implementation

- Establish governance frameworks for data quality, security, and regulatory compliance

- Scale successful pilots gradually whilst capturing lessons learned and refining processes

- Monitor key performance indicators including time to market, operational costs, and combined ratios

| Platform feature | Business impact | Implementation priority |

|---|---|---|

| API-first architecture | 50% faster product launches | Critical |

| Cloud-native infrastructure | 30-40% operational cost reduction | Critical |

| AI underwriting capabilities | 3-6 point combined ratio improvement | High |

| Multi-carrier integration | Expanded distribution reach | High |

| Automated compliance workflows | Reduced regulatory risk | Medium |

| Real-time analytics dashboards | Better decision-making | Medium |

API-first insurance platform benefits extend beyond initial implementation to ongoing operational efficiency. Platforms supporting comprehensive API strategies for insurers enable ecosystem partnerships and future innovation without major system overhauls.

Pro Tip: Engage platform providers early in evaluation processes to understand their implementation methodologies, support models, and customer success track records rather than relying solely on feature comparisons.

Modern insurance platform benefits accumulate over time as organisations develop expertise and expand marketplace usage across product lines and distribution channels. Patient, strategic implementation delivers superior results compared to rushed, comprehensive overhauls that overwhelm organisations and increase failure risk.

Discover IBSuite’s policy administration platform

IBSuite offers a cloud-native, API-first policy administration platform specifically designed for property and casualty insurers pursuing digital transformation through marketplace strategies. Built on AWS infrastructure, IBSuite supports the complete insurance value chain from sales and underwriting through claims, billing, and financial management. The platform enables rapid product launches, seamless multi-carrier integrations, and operational efficiencies aligned with marketplace requirements discussed throughout this guide.

Insurance executives exploring marketplace adoption benefit from IBSuite’s proven implementation methodology and comprehensive support for P&C insurance workflows. The platform’s API-first architecture simplifies integration with digital marketplaces, broker platforms, and ecosystem partners. Evergreen updates ensure continuous platform improvements without disruptive upgrade cycles.

Book a demo to experience how IBSuite accelerates your marketplace transformation journey. Our team works with insurance leaders to tailor solutions addressing specific operational challenges and strategic objectives.

Pro Tip: Engage early with platform providers to understand how their solutions align with your organisation’s marketplace strategy and digital transformation roadmap before committing to lengthy evaluation processes.

Frequently asked questions

What is the difference between a digital insurance marketplace and an aggregator?

Digital insurance marketplaces support complete B2B workflows including underwriting, binding, and compliance for brokers and managing general agents. Aggregators focus primarily on consumer quote comparisons for personal lines insurance. Marketplaces integrate deeply with carrier systems through APIs, whilst aggregators display surface-level pricing information for individual customers.

How do digital insurance marketplaces impact operational efficiency in P&C insurance?

Marketplaces reduce time to market by approximately 50 per cent through automated workflows and parallel carrier processing. Operational costs decrease by 30 to 40 per cent via digitisation, eliminating manual data entry and reducing errors. Brokers report productivity improvements of 40 per cent or more after adopting marketplace platforms.

What are key challenges to adopting digital insurance marketplaces?

Integration complexity with legacy systems and talent shortages represent primary adoption barriers. Seventy-four per cent of AI pilots fail to scale beyond proof-of-concept stages without strong strategy and skilled resources. Change management resistance within traditional insurance organisations also slows transformation progress.

Why should P&C insurers prioritise API-first and cloud-native platforms?

API-first architectures enable 50 per cent faster product launches and simplified ecosystem integrations. Cloud-native platforms provide elastic scalability, automatic updates, and reduced infrastructure costs. These architectural choices determine long-term transformation success and operational flexibility for marketplace participation.

Recommended

- Complete Guide to Digital Insurance Trends 2025 – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance marketplace models 2026: 50% faster launches

- Drivers of Digital Transformation in the Insurance Industry – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Understanding Digital Insurance Platform Benefits for Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System