10.04.26

Integrations in insurtech: driving efficiency in 2026

TL;DR:

- Integration forms the core architecture enabling connected, efficient insurance operations.

- API, core system, and third-party integrations drive agility, speed, and operational improvements.

- Leadership buy-in and organizational alignment are crucial for successful insurtech integration initiatives.

Digital transformation in insurance is widely misunderstood. Many executives still equate it with swapping out legacy software for shinier alternatives, yet the real engine behind scalable, efficient insurance operations is something far less visible: integration. When your policy administration, claims, billing, CRM, and third-party data sources operate as a genuinely connected ecosystem rather than isolated silos, the operational gains are profound. This article breaks down the types of integrations available to P&C insurers, the tangible efficiency benefits they deliver, the challenges you must anticipate, and the strategic mindset required to make them work at scale.

Table of Contents

- Setting the stage: integrations as the foundation of insurtech

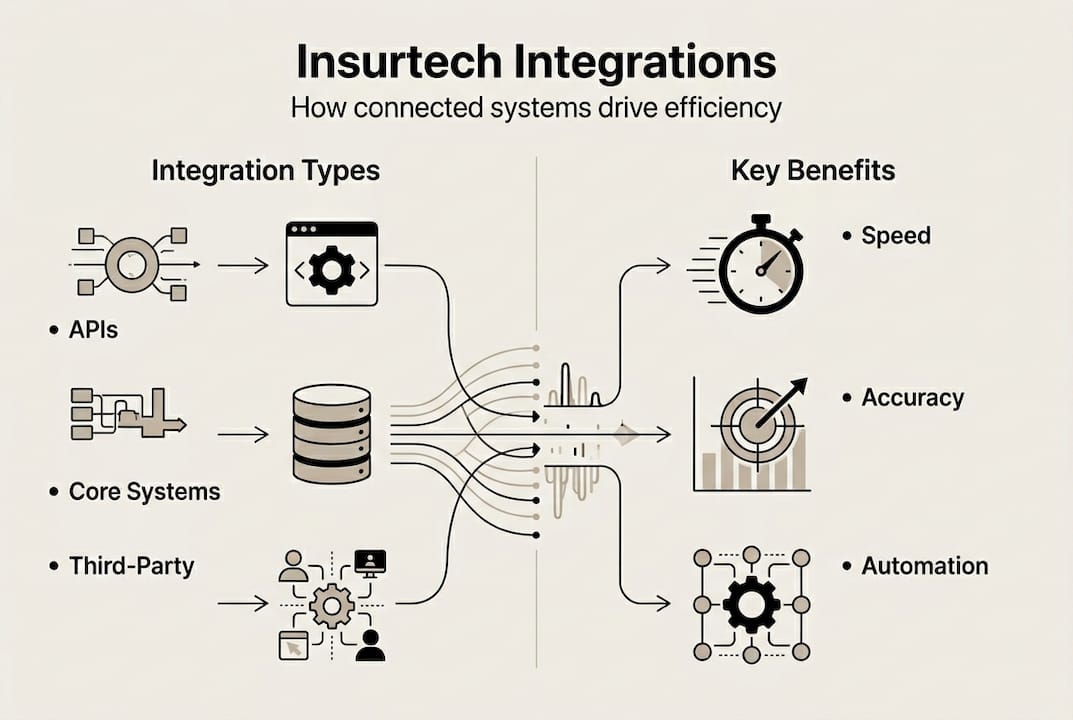

- Types of integrations in insurtech: APIs, core systems, and third-party services

- Driving operational efficiency through connected systems

- Challenges and solutions for successful insurtech integrations

- What most insurers get wrong about integrations

- Bring integration-centred efficiency to your insurance business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Integrations drive transformation | Modern insurance operations depend on effective integrations to accelerate innovation and efficiency. |

| Multiple integration types | API, core system, and third-party service integrations each provide unique benefits and should be prioritised by business need. |

| Operational gains are real | Streamlined integrations deliver measurable improvements in claims, underwriting, and customer satisfaction. |

| Address challenges proactively | Success demands resolving legacy, compliance, and organisational barriers before and throughout integration projects. |

| People, not just platforms | Sustainable integration outcomes require empowered leadership and interdepartmental collaboration. |

Setting the stage: integrations as the foundation of insurtech

Ask any insurer what slows their operations and the answer is rarely a single broken system. It is the gaps between systems. Data re-entered manually from one platform to another, claims teams waiting on underwriting data that lives in a separate database, customer service agents toggling between four screens to answer one question. These are integration failures, not technology failures.

Integrations connect disparate insurance systems and enable seamless data flow across the entire value chain. They are not optional enhancements bolted onto a core platform. They are the architecture that makes a modern insurance operation function as a single, coherent unit. Without them, even the most sophisticated individual systems underperform.

The case for prioritising integrations is well established. As noted in IBA’s analysis of digital transformation drivers, “integrations have become critical in driving digital transformation and innovation within the insurance industry.” This is not a future prediction. It reflects the current reality for carriers competing on speed, accuracy, and customer experience.

What does an integration-led foundation actually look like in practice? It typically involves:

- API-led connectivity that allows systems to communicate in real time without manual intervention

- Core system linkages across policy, claims, billing, and CRM so data flows automatically between functions

- Third-party data feeds from weather services, fraud detection tools, telematics providers, and payment processors

- Workflow automation triggers that initiate actions across systems based on defined business rules

Critically, insurance core systems can only be modernised effectively when integration is treated as a first-class architectural concern, not an afterthought. Carriers that invest in integration infrastructure early gain a compounding advantage: every new capability added to the platform benefits from the connected foundation already in place.

“The question is no longer whether to integrate, but how quickly and strategically you can do it. Insurers who treat integration as a project rather than a programme will find themselves rebuilding the same foundations repeatedly.”

Types of integrations in insurtech: APIs, core systems, and third-party services

Having established integrations as the linchpin of modernisation, the next step is to understand the specific types available and their operational impacts.

API integrations are the most flexible and widely adopted approach. An application programming interface (API) defines how two systems communicate, what data they exchange, and under what conditions. For insurers, API strategy for insurers is increasingly a board-level conversation because APIs determine how quickly a carrier can connect to new distribution partners, launch products, or respond to market shifts. As IBA’s research confirms, “API integrations enable insurers to quickly adapt to changing market needs and streamline connectivity.”

Core system integrations connect the fundamental operational components of an insurer: policy administration, claims management, billing, rating engines, and CRM. When these systems share data automatically, underwriters see claims history before binding, billing teams receive policy changes instantly, and customer records stay consistent across every touchpoint.

Third-party service integrations extend the platform outward. Payment processors, analytics vendors, telematics providers, and regulatory reporting tools all connect via standardised interfaces. The growth of financial APIs for fintech demonstrates how deeply embedded third-party connectivity has become across financial services, and insurance is following the same trajectory.

| Integration type | Key features | Complexity | Speed to value | Flexibility |

|---|---|---|---|---|

| API integration | Real-time data exchange, standardised protocols | Medium | High | Very high |

| Core system integration | End-to-end data flow, process automation | High | Medium | Medium |

| Third-party service integration | Specialist data, extended capabilities | Low to medium | High | High |

For API-first insurance platforms, the table above illustrates why API integrations tend to deliver the fastest returns: they are relatively straightforward to implement and immediately expand what a platform can do. Core system integrations take longer but deliver the deepest operational transformation. Third-party connections fill capability gaps without requiring internal development.

Pro Tip: When prioritising your integration roadmap, start with the workflows that directly affect claims cycle time and customer satisfaction. These deliver measurable ROI fastest and build internal confidence in the integration programme.

Driving operational efficiency through connected systems

With an understanding of integration types, it is crucial to grasp their real-world productivity benefits and operational impact.

The most immediate gain from connected systems is the elimination of redundant data entry. When data integration in insurance is handled at the platform level, staff stop re-keying information between systems. Errors drop. Processing speeds increase. And the data that flows through your operation becomes trustworthy enough to base decisions on.

In claims specifically, integration is transformative. As IBA’s claims platform demonstrates, “connected systems reduce repetitive data entry and enable faster claims handling.” A claims handler with a fully integrated view can assess a loss, verify coverage, trigger a payment, and update the customer record without leaving a single interface.

Here is how an integrated claims process typically unfolds:

- First notice of loss is submitted via a digital channel and automatically populates the claims system

- Policy data is pulled from the administration system in real time, confirming coverage without manual lookup

- Third-party data (weather records, repair estimates, fraud scores) is ingested automatically from connected vendors

- Adjudication rules are applied by the system, escalating complex cases and auto-settling straightforward ones

- Payment is triggered through the integrated billing system, with the customer notified automatically via CRM

- The claim record is closed and data is passed to analytics tools for reporting and reserving

The efficiency gains are quantifiable. Consider what connected core systems in insurance can deliver:

| Metric | Without integration | With integration |

|---|---|---|

| Average claims cycle time | 14 to 21 days | 5 to 9 days |

| Data entry error rate | 8 to 12% | Under 2% |

| Customer satisfaction (NPS) | Moderate | Significantly higher |

| Staff processing capacity | Baseline | 30 to 40% increase |

For insurers evaluating CRM integration comparison options, the data consistently shows that connected customer records improve retention and cross-sell rates alongside operational metrics.

Pro Tip: Track integration ROI using three core KPIs: claims cycle time, net promoter score, and staff cases handled per day. These give you a balanced view of efficiency, customer impact, and workforce productivity.

Challenges and solutions for successful insurtech integrations

Despite clear benefits, integrating insurtech presents tangible challenges that leaders must pragmatically anticipate and resolve.

The four most common barriers are legacy system compatibility, data security, regulatory compliance, and change management. Each is real. None is insurmountable with the right approach.

- Legacy system compatibility: Older platforms often lack modern API support. Solutions include middleware layers, API gateways, and phased migration strategies that allow legacy and modern systems to coexist during transition

- Data security: Connecting systems increases the attack surface. Mitigate this through end-to-end encryption, strict access controls, and regular penetration testing across all integration points

- Regulatory compliance: Data sharing between systems must comply with jurisdiction-specific rules. Automated compliance reviews embedded into integration workflows reduce manual oversight burden and flag issues before they become violations

- Change management: Staff accustomed to existing processes resist new workflows. Structured training programmes, clear communication about benefits, and cross-functional integration teams reduce friction significantly

Vendor evaluation deserves particular attention. Thorough API documentation, clear SLAs, and a vendor’s track record with similar carriers are non-negotiable due diligence items. The API-driven edge in insurance increasingly belongs to carriers who choose partners with proven integration ecosystems rather than point solutions.

Governance is equally critical. Establishing an integration centre of excellence, with ownership clearly assigned across IT, operations, and compliance, prevents the fragmented decision-making that derails otherwise well-funded programmes.

As IBA’s research on overcoming integration challenges makes clear: “Overcoming integration challenges requires a robust strategy, clear governance, and culture embracing change.”

What most insurers get wrong about integrations

Here is the uncomfortable truth: the majority of integration initiatives that stall or fail do so not because of technology, but because of people and structure.

Carriers invest heavily in platform selection and API documentation, then under-invest in the cross-functional alignment needed to make integrations deliver value. A technically flawless connection between your claims and billing systems means very little if the claims team and finance team still operate as separate kingdoms with separate priorities.

Real ROI from integration arrives when the connected systems align with strategic goals that are owned and championed from the executive level downward. As IBA’s work on integration pitfalls confirms, “leadership buy-in and a cultural shift are often more decisive to integration success than any single platform or tool.”

This means your integration strategy must include investment in training, interdepartmental communication, and shared KPIs that cross functional boundaries. Technology connects systems. Leadership connects people. Both are required.

Pro Tip: Assign a named executive sponsor to every major integration initiative. Without senior ownership, integration projects drift into IT backlogs and never reach their operational potential.

Bring integration-centred efficiency to your insurance business

If this article has clarified one thing, it is that integration is not a technical detail to delegate downward. It is a strategic capability that determines how fast you can innovate, how efficiently your teams operate, and how well you serve your policyholders. IBSuite is built from the ground up as an API-first, end-to-end platform designed to make that connectivity real and manageable. From our policy administration solution to our claims management tools, every component is designed to work as a seamlessly integrated whole. If you are ready to move from fragmented systems to a connected operation, we would welcome the conversation.

Frequently asked questions

What types of integrations are most important in insurtech?

API, core system, and third-party service integrations are essential, as they enable agility, data flow, and seamless customer experiences. API integrations in particular allow insurers to adapt quickly to market changes without rebuilding core systems.

How do integrations improve insurance operational efficiency?

Integrations automate workflows, reduce manual data entry, and speed up both underwriting and claims processing for higher productivity. Connected systems eliminate the bottlenecks caused by data moving manually between platforms.

What challenges do insurers face with integrations?

The most common challenges are legacy systems, regulatory compliance, and ensuring data security; choosing the right partners and clear governance can help mitigate risks. A structured approach to overcoming integration challenges reduces both technical and organisational friction.

Why is leadership important in the success of insurtech integrations?

Leadership buy-in and a commitment to cultural change are vital for alignment and follow-through on digital transformation initiatives. Without executive sponsorship, even well-designed integrations fail to deliver their intended operational value.

Recommended

- Drivers of Digital Transformation in the Insurance Industry – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance marketplace models 2026: 50% faster launches

- 7 Key Insurtech Trends 2025 for P&C Insurance Leaders – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Overcoming Integration Challenges – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Why automate compliance in 2026: benefits for finance & tech firms