03.03.26

Digital Insurance Broker: 70% Faster Underwriting

Digital insurance brokers can reduce underwriting times by up to 70%, transforming how P&C insurers operate in 2026. This guide unpacks what digital brokers are, how their technology differs from traditional models, and concrete ways you can leverage them to drive operational efficiency and elevate customer engagement across your organization.

Table of Contents

- Introduction to Digital Insurance Brokers

- Technological Enablers of Digital Insurance Brokers

- Operational Efficiency Gains From Digital Brokers

- Enhancing Customer Engagement Through Digital Insurance Brokers

- Common Misconceptions About Digital Insurance Brokers

- Comparison Framework: Digital vs. Traditional Brokers

- Real-World Examples and Case Studies

- Implementation Challenges and Strategic Considerations

- Explore Modern Insurance Platforms to Accelerate Your Digital Brokerage

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Speed and Automation | Digital insurance brokers cut underwriting times by up to 70% through automated workflows. |

| Technology Foundation | Cloud-native platforms and API integrations enable scalable, flexible broker solutions. |

| Hybrid Models | Combining human advisors with digital tools preserves trust while boosting efficiency. |

| Operational Impact | Insurers gain cost savings, faster product launches, and improved data accuracy. |

| Customer Benefits | Instant quotes, personalized policies, and digital interactions enhance satisfaction and loyalty. |

Introduction to Digital Insurance Brokers

Digital insurance brokers leverage cloud-native platforms and APIs to automate sales, underwriting, and policy management. Unlike traditional brokers who rely on manual processes and in-person meetings, digital brokers handle workflows through software. They provide automated underwriting, instant quoting, policy issuance, and digital claims initiation, all integrated with insurer core systems.

Traditional brokers spend significant time on paperwork, phone calls, and face-to-face consultations. Digital brokers replace many of these steps with automated decisioning and self-service portals. This shift accelerates product launches and enables scalability that manual processes cannot match. Understanding digital-first insurance strategies helps you see how digital brokers fit into broader transformation efforts.

Core functions of digital brokers include:

- Automated underwriting using predefined rules and AI models

- Real-time quoting and policy comparison engines

- Digital policy issuance and document management

- Integrated claims initiation and tracking

- API-driven data exchange with insurer platforms

These capabilities fundamentally change how insurers interact with customers and manage risk. Digital brokers support faster time-to-market for new products and enable insurers to compete more effectively in a digital economy.

Technological Enablers of Digital Insurance Brokers

Cloud-native platforms provide the foundation for digital brokers by delivering flexibility, scalability, and reduced IT maintenance costs by up to 30%. These platforms eliminate the need for on-premise infrastructure and enable continuous updates without disrupting operations. When selecting modern insurance platforms, prioritize those with robust API ecosystems.

API-first architecture allows digital brokers to integrate seamlessly with insurer core systems, third-party data providers, and distribution channels. API-first insurance platforms enable real-time data exchange, reducing manual data entry and errors. This architecture supports rapid innovation by allowing new services to connect without rebuilding existing systems.

Automation and AI streamline workflows across the insurance value chain:

- Automated underwriting evaluates risk based on real-time data

- AI-powered recommendations personalize policy options for customers

- Robotic process automation handles routine administrative tasks

- Machine learning improves fraud detection and claims accuracy

Pro Tip: Select platforms with proven API integration capabilities to avoid technical debt and ensure future-proofing as your technology stack evolves.

These technologies work together to create a digital broker ecosystem that operates faster and more accurately than traditional models. Optimizing cloud insurance platforms ensures you maximize the value of these investments.

Operational Efficiency Gains From Digital Brokers

Automated underwriting can reduce processing time by 50-70%, directly impacting your bottom line. This acceleration comes from eliminating manual review steps, automating data collection, and applying consistent decisioning logic. Insurers also see cost reductions from less labor-intensive workflows and improved accuracy that reduces errors and rework.

Integration with core systems enables smooth data flow between brokers, underwriting, policy administration, and claims. This connectivity eliminates data silos and ensures all departments work from the same information. Understanding digital insurance platform benefits helps you quantify potential gains.

To realize operational efficiency from digital brokers, follow these steps:

- Assess current workflows to identify manual bottlenecks and inefficiencies

- Select a cloud-native platform with strong API support and automation capabilities

- Integrate the platform with existing core systems using APIs

- Automate workflows for underwriting, quoting, and policy issuance

- Measure outcomes through key performance indicators like processing time and cost per policy

Pro Tip: Prioritize platforms with proven integration track records in your insurance segment to reduce transition risks and accelerate time to value.

The benefits of modern insurance platforms extend beyond speed to include better data quality, compliance support, and the ability to launch new products in weeks rather than months. These improvements compound over time, creating sustained competitive advantage.

Enhancing Customer Engagement through Digital Insurance Brokers

Digital brokers provide instant quotes and AI-driven policy recommendations, delivering measurable gains in customer satisfaction. Customers no longer wait days for quotes or policy decisions. Instead, they receive immediate responses and can complete transactions digitally at their convenience. This speed and transparency build trust and increase conversion rates.

Personalized policy suggestions powered by AI analyze customer data to recommend coverage that fits individual needs. This customization goes beyond generic product offerings to create tailored solutions. Digital document management simplifies policy issuance and claims filing, reducing friction throughout the customer journey.

Key customer engagement improvements include:

- Instant digital quotes that shorten the buying cycle

- AI-enabled personalized recommendations that improve policy fit

- Self-service portals for policy management and claims filing

- Omni-channel interactions blending digital and advisor support

- Real-time status updates and notifications

Customer engagement scores improve measurably after digital broker adoption. Insurers report higher Net Promoter Scores, increased policy retention, and greater customer lifetime value. Digital brokers support omni-channel strategies that let customers choose how they interact, whether through self-service or with human advisors.

The combination of speed, personalization, and convenience creates experiences that meet modern customer expectations. Exploring insurance customer experience improvements shows how digital brokers fit into broader engagement strategies.

Common Misconceptions about Digital Insurance Brokers

Many executives believe digital brokers will fully replace human agents. In reality, over 60% of successful implementations use hybrid human-digital models. These models combine automated workflows with human expertise for complex risks or high-value customers. The technology handles routine tasks while agents focus on advisory services that require judgment and relationship building.

Another misconception is that digital brokers are simply traditional brokers with websites. True digital brokers use cloud-native, API-driven automation that fundamentally transforms operations. They integrate with insurer core systems, apply real-time data analytics, and automate decisioning in ways basic websites cannot.

Some leaders assume digital broker adoption guarantees instant, flawless operations. Integration with legacy systems and regulatory compliance requires careful planning and phased implementation. Success depends on selecting the right platform, managing change effectively, and addressing technical debt in existing systems.

Understanding these realities helps you:

- Set realistic transformation timelines and expectations

- Design hybrid models that leverage both technology and human expertise

- Allocate sufficient resources for integration and change management

- Avoid underestimating the strategic planning required for success

Addressing these misconceptions upfront prevents common pitfalls and improves your chances of achieving the full benefits digital brokers offer.

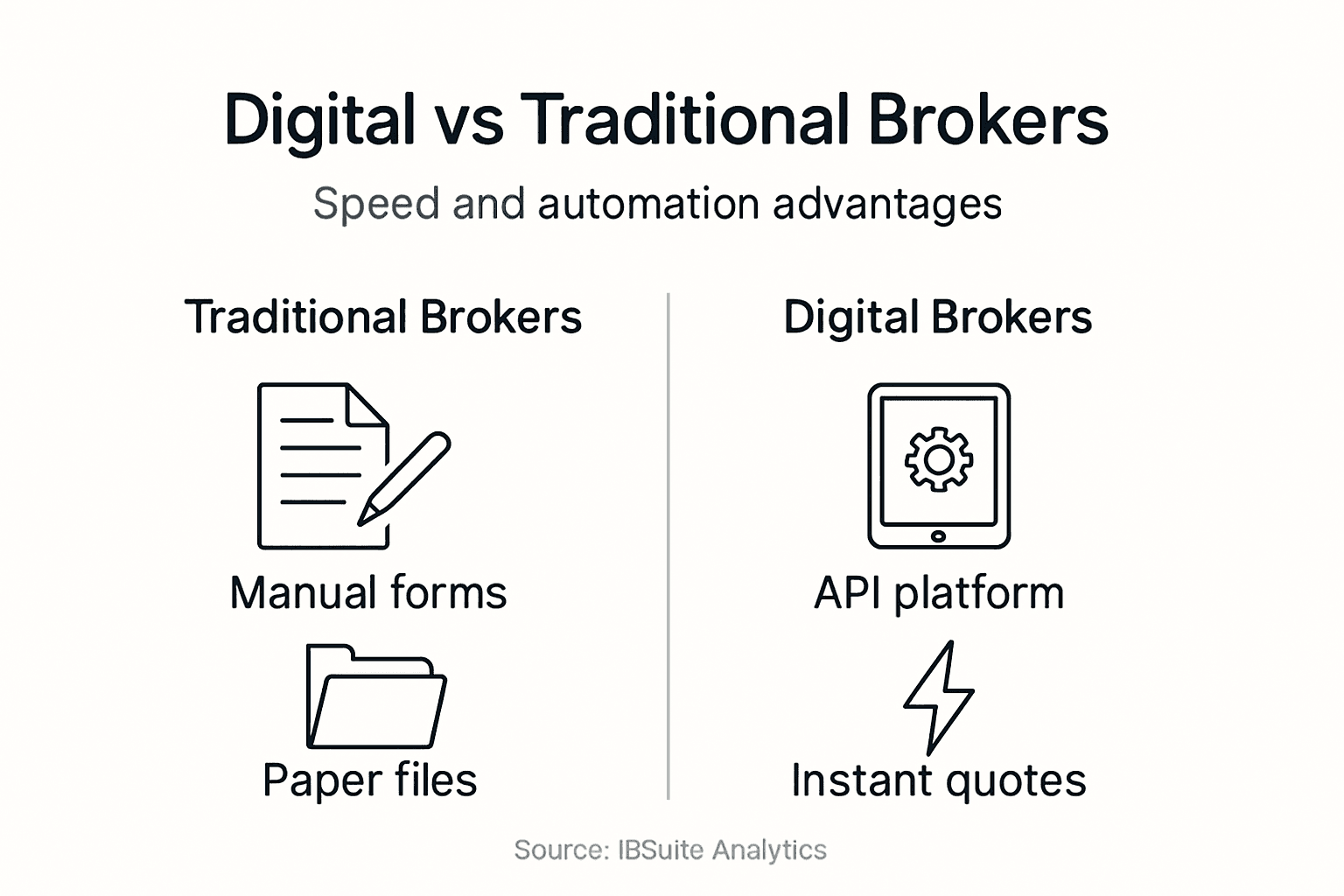

Comparison Framework: Digital vs. Traditional Brokers

Traditional brokers rely on manual workflows, face-to-face meetings, and paper-based documentation. Product launches can take months due to the need to train agents, print materials, and establish manual processes. Customer interactions happen primarily in person or via phone, limiting scalability and creating bottlenecks during peak periods.

Digital brokers use cloud-native platforms and automation to accelerate every step. They enable instant quotes, automated underwriting, and digital policy issuance. Customer interaction shifts to omni-channel digital experiences that support self-service while preserving access to human advisors when needed. Understanding P&C insurance distribution types provides context for how digital brokers fit into your distribution strategy.

| Dimension | Traditional Brokers | Digital Brokers |

|---|---|---|

| Workflow | Manual processes, paper documentation | Automated workflows, digital documentation |

| Underwriting Speed | Days to weeks | Minutes to hours |

| Customer Interaction | In-person, phone | Omni-channel digital, self-service with advisor support |

| Technology Platform | Legacy systems, limited integration | Cloud-native, API-first architecture |

| Product Launch Time | Months | Weeks |

| Scalability | Limited by agent capacity | Highly scalable through automation |

Key differences in operational approach:

- Digital brokers automate risk assessment using real-time data feeds

- Traditional brokers require manual data collection and analysis

- Digital platforms enable continuous innovation through API integration

- Traditional systems often require custom development for changes

The speed advantage of digital brokers compounds across the insurance value chain, enabling faster product innovation, quicker response to market changes, and better customer experiences.

Real-World Examples and Case Studies

A Central European P&C insurer reduced underwriting time by 65% after integrating digital broker capabilities through a modern core platform. The insurer automated risk assessment, policy issuance, and initial claims processing. Sales increased by 25% within the first year as the faster underwriting process improved conversion rates and enabled expansion into new market segments.

Cost savings came from multiple sources:

- Reduced manual effort in underwriting and policy administration

- Lower error rates and rework from automated data validation

- Decreased IT maintenance costs through cloud-native infrastructure

- Faster product launches that reduced time-to-market expenses

Lessons learned from this transformation include the importance of phased integration, starting with less complex product lines before expanding to the full portfolio. The insurer maintained hybrid agent models, allowing experienced underwriters to focus on complex risks while automation handled routine cases. A comprehensive digital transformation roadmap proved essential for managing change and maintaining business continuity.

The competitive advantage became clear within months. The insurer launched three new products in the time it previously took to launch one. Customer satisfaction scores improved by 35% due to faster quotes and policy issuance. Agent productivity increased as they spent less time on administrative tasks and more on customer relationships.

These measurable improvements demonstrate the tangible business impact digital brokers deliver when implemented strategically with the right technology foundation.

Implementation Challenges and Strategic Considerations

Integration complexity with legacy insurer systems represents the most common barrier to digital broker adoption. Many core systems lack modern APIs, requiring custom integration work or middleware solutions. This technical debt can slow implementation and increase costs if not addressed strategically.

Regulatory compliance must be factored into platform selection and workflow design. Digital brokers must maintain audit trails, data privacy protections, and compliance with insurance regulations across jurisdictions. Platforms with built-in compliance features reduce this burden.

Critical success factors include:

- Robust API architecture that enables seamless integration with existing systems

- Continuous platform updates that keep pace with regulatory changes

- Strong vendor support and implementation expertise

- Clear change management processes to support organizational adoption

Adopting hybrid human-digital brokerage models helps maintain customer trust during transitions. Customers accustomed to personal relationships appreciate having access to advisors while benefiting from digital convenience. This approach also eases internal resistance by showing agents how technology enhances rather than replaces their roles.

Strategic planning reduces implementation risks. Start with a pilot program on a single product line or market segment. Measure results, refine processes, then expand gradually. Partner with experienced providers who understand insurance operations and can guide you through technical and organizational challenges. Exploring API-first core insurance platforms helps you evaluate platform capabilities before committing.

Phased rollout allows you to build internal expertise, prove value to stakeholders, and adjust your approach based on real-world feedback. This method delivers faster time to value while managing risk effectively.

Explore Modern Insurance Platforms to Accelerate Your Digital Brokerage

Discover how modern insurance platforms powered by IBSuite enable seamless digital brokerage through cloud-native architecture and API-first design. IBSuite supports the full insurance value chain from sales and underwriting to policy administration, claims, and billing, helping you achieve the operational efficiency and customer engagement gains outlined in this guide.

Leverage automation and integrated workflows to boost productivity while maintaining the flexibility to adapt quickly to market changes. IBSuite’s proven integration capabilities reduce implementation risks and accelerate your path to digital transformation. Understanding the complete range of insurance platform benefits helps you evaluate how these capabilities apply to your specific needs.

Ready to see how a modern core platform can transform your brokerage operations? Book a demo to explore IBSuite’s capabilities and discuss a customized roadmap for your digital broker strategy.

FAQ

What is the difference between a digital insurance broker and a traditional insurance broker?

Digital brokers automate workflows through cloud-native platforms and APIs, while traditional brokers rely on manual processes and in-person interactions. Digital brokers deliver faster underwriting, instant quotes, and digital engagement, whereas traditional brokers provide more face-to-face service. Many successful insurers use hybrid models that combine digital efficiency with human advisory for complex situations, preserving relationship value while gaining automation benefits.

How do digital insurance brokers improve customer engagement?

They offer instant digital quotes, AI-driven policy recommendations, and digital document handling that create faster, more transparent interactions. This convenience and personalization lead to higher customer satisfaction scores and increased loyalty. Customers appreciate the ability to self-serve for routine tasks while still accessing human advisors when needed.

What are the main challenges when implementing digital insurance brokers?

Integration with legacy insurer systems and ensuring regulatory compliance represent the biggest complexities. Strategic planning, selecting platforms with strong API architectures, and phased implementation help mitigate these challenges. Working with experienced partners who understand insurance operations reduces risk and accelerates successful adoption.

Recommended

- Digital Underwriting Workflow Guide for Seamless Automation – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- How to Optimise Underwriting Workflows for Efficiency

- Drivers of Digital Transformation in the Insurance Industry – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Modern Insurance Platform Benefits – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System