13.05.26

Cloud transformation in P&C insurance: a practical guide

Cloud transformation has moved well beyond the server room. For property and casualty insurers, it represents a fundamental rethinking of how products are built, priced, distributed, and serviced. The pressure is real: policyholders expect Amazon-grade self-service, regulators are tightening data governance standards, and competitors are launching new products in weeks rather than years. Insurers who treat cloud migration as a purely technical exercise are leaving measurable business value on the table. This guide cuts through the complexity and equips you with the knowledge to drive transformation that genuinely moves the needle.

Table of Contents

- What is cloud transformation in P&C insurance?

- Major benefits: why cloud transformation delivers value

- Approaches and methodologies: navigating the transformation journey

- Challenges, risks, and compliance realities

- From planning to execution: driving value in real P&C environments

- What most cloud transformation journeys get wrong—and how to get it right

- Unlock the next phase of cloud-driven insurance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Business value first | Cloud transformation is most effective when driven by measurable business outcomes, not just IT strategy. |

| Choose the right approach | Successful migrations balance phased, flexible strategies with careful vendor and methodology selection. |

| Prioritise governance | Robust data and compliance governance is essential for maximising benefits and managing risks. |

| Track transformation KPIs | Monitoring claims cycle time, STP rates, and customer satisfaction ensures ongoing improvement. |

What is cloud transformation in P&C insurance?

Let’s begin by defining our terms. Cloud transformation in P&C insurance is not simply moving files to an off-premises server. It is the deliberate migration of legacy core systems, including claims platforms, policy administration engines, rating engines, and data warehouses, to cloud-native environments built for elasticity, automation, and real-time responsiveness.

As McKinsey describes it, cloud transformation in P&C involves migrating legacy core systems to cloud-native platforms to enable scalability, automation, real-time analytics, and ecosystem integration. That definition matters because it sets the scope well beyond infrastructure cost reduction.

The shift towards cloud-native architecture enables insurers to integrate with third-party data sources via APIs, deploy AI-powered underwriting models at scale, and release product updates without lengthy regression testing cycles. These capabilities translate directly into competitive advantage.

Key dimensions of cloud transformation for P&C insurers include:

- Policy administration: Enabling dynamic product configuration and real-time endorsements

- Claims management: Automating triage, fraud detection, and settlement workflows

- Rating and pricing: Deploying telematics and external data feeds without core system changes

- Customer engagement: Powering self-service portals and personalised communications through API-first design

- Data and analytics: Consolidating fragmented data estates into governed, query-ready repositories

“The question is no longer whether to move to the cloud, but how to extract the most business value from doing so.”

When approached strategically, optimising P&C cloud platforms produces compounding returns across underwriting accuracy, claims efficiency, and customer retention. The foundation is a clear understanding of which core insurance systems are best positioned to generate early wins.

Major benefits: why cloud transformation delivers value

Now that we understand what cloud transformation means, let’s see why leading insurers are prioritising it, especially in business terms.

The benefits are best understood across four domains: cost, speed, resilience, and customer experience. Research consistently shows that cloud-migrated insurers outperform their on-premises counterparts across all four.

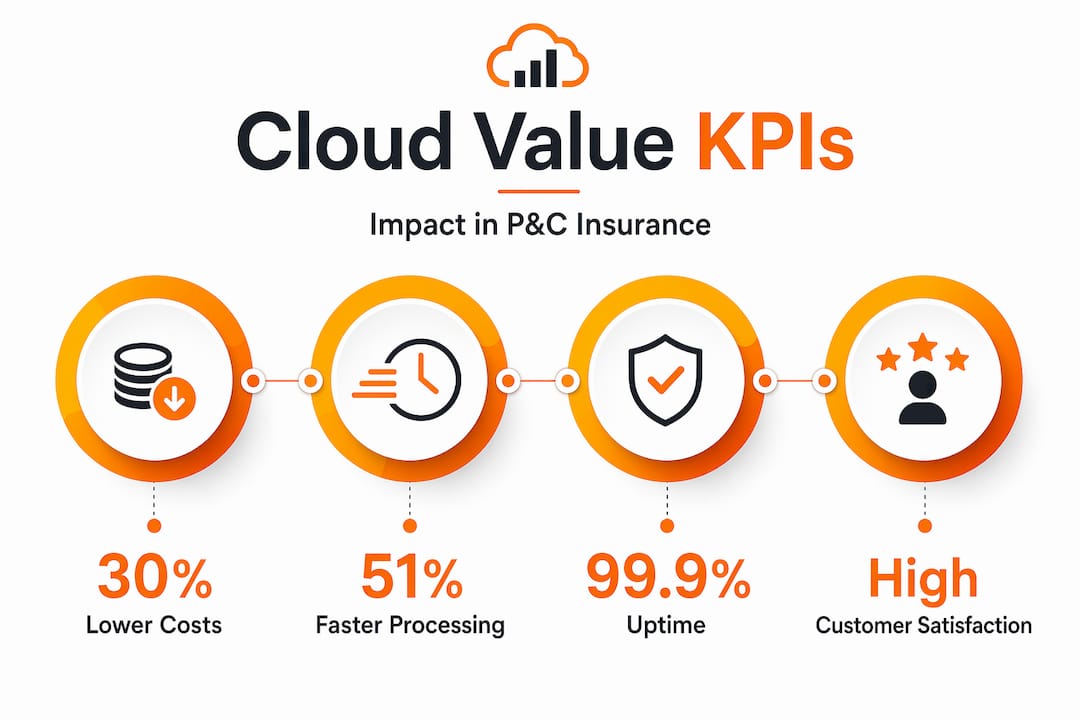

Empirical evidence from a leading US insurer’s transformation programme found dramatic operational improvements: a 30 to 51% reduction in licensing and operational costs, a 70% increase in application performance, 94% less unplanned downtime, 50% faster policy quoting, 80% straight-through processing rates, and 40% faster speed-to-market for new products.

| Benefit area | Typical improvement | Business impact |

|---|---|---|

| Operational costs | 30–51% reduction | Frees capital for product innovation |

| Application performance | 70% increase | Faster processing, fewer errors |

| Unplanned downtime | 94% reduction | Higher SLA reliability and trust |

| Policy quoting speed | 50% faster | Improved broker and customer experience |

| Speed-to-market | 40% faster | Competitive agility in new segments |

| Straight-through processing | Up to 80% | Significant reduction in manual handling |

These are not theoretical projections. They are documented outcomes from real P&C environments. The practical insurance cloud adoption benefits extend further when you factor in reduced technical debt and the elimination of costly end-of-life system maintenance contracts.

From a customer engagement standpoint, cloud-native architecture enables personalised digital experiences through robust API layers. Insurers can integrate real-time weather data to trigger proactive communications during severe events, offer dynamic self-service claims lodgement via mobile, and deliver personalised renewal offers based on behavioural data. None of this is feasible on monolithic legacy stacks.

Cloud infrastructure also serves as the prerequisite for serious AI and analytics adoption. Fragmented on-premises data cannot support enterprise-grade machine learning pipelines. Moving to a unified, governed cloud data estate is the essential first step before AI investments produce reliable results. Understanding the full range of insurer cloud value metrics helps leadership build a credible business case.

Pro Tip: Build your business case using a three-horizon model. Horizon one captures near-term cost reduction from infrastructure consolidation. Horizon two quantifies speed and STP gains from process automation. Horizon three values the strategic optionality unlocked by AI, ecosystem partnerships, and rapid product launches.

Approaches and methodologies: navigating the transformation journey

Armed with the business case, the next step is deciding how to approach the transformation itself.

There is no single right methodology. The best approach depends on your current system landscape, regulatory environment, budget tolerance, and strategic ambition. McKinsey’s framework for core system modernisation identifies several migration patterns that each carry distinct trade-offs.

The three primary migration strategies:

- Lift-and-shift (rehost): Moving existing workloads to the cloud with minimal modification. Fast and low-risk initially, but EY research confirms that lift-and-shift risks higher costs if cloud-native optimisation does not follow promptly.

- Replatform: Migrating to managed cloud services with moderate refactoring. Balances speed and optimisation. Suitable for mid-size policy administration systems.

- Refactor (cloud-native rebuild): Redesigning systems as microservices or SaaS platforms. Highest effort, highest return. Most appropriate for claims engines and rating platforms where flexibility is critical.

Beyond technical migration patterns, insurers face a strategic build-vs-buy-vs-upgrade decision. Here is how the options compare across six business dimensions:

| Dimension | Build | Buy (SaaS) | Upgrade (replatform) |

|---|---|---|---|

| Functionality | Fully customisable | Standardised with configuration | Inherited with improvements |

| Cost | High upfront, ongoing dev | Predictable subscription | Moderate, phased |

| Speed to value | Slow (18–36 months) | Fast (6–12 months) | Medium (12–24 months) |

| Scalability | Depends on architecture | Built-in | Improved but limited |

| Risk | High execution risk | Vendor dependency risk | Integration complexity |

| Future-readiness | Highest if well-built | Vendor roadmap-dependent | Moderate |

Vendor selection deserves serious scrutiny. Cloud migration for insurers delivers the greatest value when vendor platforms offer genuine integration flexibility, ecosystem partnerships with third-party data providers, and a credible product roadmap. Consulting a detailed cloud migration guide tailored to P&C environments helps avoid common selection pitfalls.

A phased transformation roadmap is usually preferable to a “big bang” cutover. Phased adoption lets you demonstrate ROI incrementally, maintain operational continuity, and course-correct before committing entire business units to a new platform.

Pro Tip: Evaluate SaaS vendors on their release cadence and how Evergreen updates are managed. A vendor that controls its own release schedule without requiring customer intervention dramatically reduces your ongoing IT overhead and positions you to benefit from continuous platform improvements without costly upgrade projects.

Challenges, risks, and compliance realities

Alongside the opportunities come a range of challenges, some regulatory, some technical, and some hidden until you are deep in the programme.

Data sovereignty is among the most complex. Regulations such as DORA (the EU Digital Operational Resilience Act) impose strict requirements on data residency, contractual rights with technology providers, and incident reporting. Cloud migration compliance risks include data residency obligations, encryption and tokenisation requirements, vendor lock-in exposure, inconsistent data formats during migration, and higher-than-anticipated egress or retraining costs.

Key risks to actively manage include:

- Vendor lock-in: Proprietary APIs and data formats can make switching providers prohibitively expensive. Prioritise open standards and contractual portability clauses.

- Data migration quality: Legacy systems often carry decades of inconsistently formatted data. Poor migration planning leads to downstream reporting failures and compliance gaps.

- Egress costs: Moving large volumes of claims images, documents, and telemetry data between cloud and on-premises environments can generate unexpected costs if not modelled in advance.

- Regulatory scrutiny: Supervisory expectations around cloud outsourcing are rising. DORA, in particular, requires documented third-party risk assessments and ongoing monitoring.

- Change fatigue: Large-scale migrations affect underwriters, claims handlers, and customer service teams simultaneously. Underestimating the human change management dimension is a common and costly mistake.

“Governance is not a constraint on cloud transformation. It is the mechanism that makes sustainable transformation possible.”

MAPFRE’s large-scale cloud programme illustrates what good governance looks like in practice. Their Landing Zone approach standardised more than one million cloud resources using infrastructure-as-code via Terraform and established private connectivity for over 150,000 users, all while maintaining compliance with local data residency requirements across multiple jurisdictions.

Hybrid cloud strategies offer a pragmatic middle path. Sensitive policy and claims data can remain in private cloud or on-premises environments, whilst customer-facing digital channels and analytics workloads run on public cloud. Consulting expert guidance on cloud compliance risks helps leadership establish clear boundaries before migration begins.

Pro Tip: Before finalising your cloud vendor contracts, commission a legal review of data portability and exit provisions. The cost of a thorough review upfront is trivial compared to the commercial and operational cost of being locked into a platform that no longer serves your strategy.

From planning to execution: driving value in real P&C environments

With risks and mitigations clear, the path forward moves from theory to actionable steps that drive meaningful outcomes.

The most successful transformation programmes share a common trait: they start with business outcomes, not technology. Rather than asking “which systems shall we migrate?”, high-performing teams ask “where does slow or unreliable technology most hurt our customers and our margins today?”

Here is a sequenced approach that consistently delivers results:

- Identify high-impact domains first. Claims processing and underwriting automation typically offer the fastest ROI. Business-aligned roadmaps with executive buy-in, starting in claims and underwriting, consistently outperform technology-led sequencing.

- Unify your data estate before migrating applications. Data fragmentation is the single most common cause of delayed transformation value. Establishing a governed data foundation early enables every subsequent workload to benefit from clean, consistent data. Data unification and governance should precede application migration, not follow it.

- Establish cross-functional governance from day one. Include finance, compliance, operations, and technology in the steering group. Decisions about data sovereignty, vendor selection, and release schedules affect all of these functions.

- Define your KPIs before you begin. Agree on claims cycle time targets, STP rate improvements, and NPS benchmarks before migration starts. This disciplines the programme and enables objective assessment of progress.

- Adopt incremental, modular rollouts. Avoid replacing entire platforms in a single cutover. Modular adoption reduces risk, preserves operational continuity, and allows teams to build confidence with new tools before full dependency.

- Invest in insurance change management as a core programme workstream. Technology adoption fails when people are not brought along. Claims handlers, underwriters, and customer service teams need structured training, clear communication, and visible leadership support.

Digitising insurance processes through cloud-native tools produces compound benefits when change management is treated as seriously as technical delivery. An insurance digital-first strategy requires both dimensions to succeed.

Pro Tip: Run a pilot in a single line of business or geography before scaling. A contained pilot lets you validate integration assumptions, surface unexpected compliance issues, and build an internal case study that accelerates stakeholder confidence across the wider business.

What most cloud transformation journeys get wrong—and how to get it right

Here is an uncomfortable observation from watching dozens of insurer transformation programmes: the technology rarely fails. The programme fails. And it fails for predictable reasons that have nothing to do with servers, APIs, or cloud vendors.

The most common failure mode is treating cloud transformation as an IT cost reduction project. When the steering committee’s primary success metric is infrastructure spend reduction, the business outcomes, faster claims, better customer experiences, and faster product launches, get subordinated to IT economics. The transformation delivers a smaller bill from the cloud provider and almost nothing else.

The second failure mode is underestimating data readiness. Insurers frequently discover mid-migration that their legacy systems contain multiple conflicting versions of the same customer record, claim, or policy. Attempting to resolve this in parallel with a live migration compounds both problems. Accessing real value from cloud requires clean, governed data as a prerequisite, not an afterthought.

The most forward-thinking insurers do three things differently. First, they appoint a business executive, not an IT director, as the transformation lead. This changes the conversation from technical milestones to business outcomes. Second, they invest in process reimagining before migration. If you move a broken process to the cloud, you have a faster broken process. Third, they measure ruthlessly from day one, tracking claims cycle time, STP rates, and customer satisfaction as primary indicators rather than server uptime or migration completion percentages.

Cloud transformation done well is not a technology project with business benefits attached. It is a business transformation programme that happens to require a technology platform. That distinction, simple as it sounds, separates the programmes that deliver transformative value from those that merely replace one cost centre with another.

Unlock the next phase of cloud-driven insurance

If this guide has clarified the path ahead, the logical next step is exploring the platforms designed to make it real. IBSuite from IBA is an AWS-native, API-first core insurance platform built specifically for P&C insurers ready to modernise without the risk of a full rip-and-replace. From cloud-based claims management that automates triage and settlement workflows to a fully configurable policy administration platform that enables rapid product launches, IBSuite delivers the technical foundation and the Evergreen update model that keeps you ahead of regulatory and market changes. Discover how global insurers are using IBSuite to reduce claims cycle times, achieve higher STP rates, and launch new products in weeks.

Frequently asked questions

Which core insurance systems benefit most from migration to the cloud?

Policy administration, claims management, and analytics systems see the greatest impact due to their need for scalability, automation, and real-time data integration. McKinsey confirms that core system migration to cloud-native platforms enables the ecosystem connectivity these systems require.

How can P&C insurers manage data sovereignty and compliance when using the cloud?

By adopting hybrid cloud models, enforcing robust governance frameworks, and selecting providers with strong compliance features such as data residency controls and encryption. Operational resilience requirements such as DORA make provider selection and contractual diligence essential.

What is the risk of vendor lock-in during insurance cloud transformation?

Vendor lock-in limits your ability to customise, negotiate, or switch providers without significant cost and disruption. Prioritising open APIs, data portability clauses, and modular adoption strategies substantially reduces this migration risk.

What KPIs should insurers track during and after cloud transformation?

Monitor claims cycle time, straight-through processing rates, and Net Promoter Score as primary indicators. These business-aligned metrics ensure the programme is delivering customer and operational value, not just technical milestones.

Is a lift-and-shift migration approach sufficient for legacy insurance systems?

It can serve as a starting point, but it is rarely sufficient on its own. Without subsequent cloud-native optimisation, lift-and-shift migrations often result in higher costs and missed performance gains compared to replatforming or refactoring approaches.

Recommended

- How to Digitize Insurance Processes for P&C Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Optimizing Cloud Insurance Platforms for P&C Success

- Digital Transformation Roadmap for P&C Insurance Success – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Cloud Migration in Insurance Guide for P&C Insurers