01.07.26

What is digital claims management for P&C insurers

Digital claims management is the end-to-end handling of insurance claims through integrated digital platforms, replacing manual processes with automation, AI, and cloud-native workflows from first notice of loss to final settlement. Known formally as claims lifecycle digitalisation, this approach is reshaping how property and casualty insurers process, adjudicate, and close claims. The efficiency gains are substantial: automated platforms reduce per-claim costs from £15–£22 to £3–£5 and compress cycle times from 14 days to under 24 hours for eligible claims. For insurance executives weighing investment decisions, those numbers represent a structural shift in operational economics, not a marginal improvement.

What is digital claims management and how does it work?

Digital claims management is defined as a technology-driven process that covers every stage of the claims lifecycle, from digital claim submission through triage, adjudication, fraud detection, and payment settlement. The industry term for this end-to-end approach is claims lifecycle digitalisation, though the phrase “digital claims management” is now widely used by practitioners and platform providers alike.

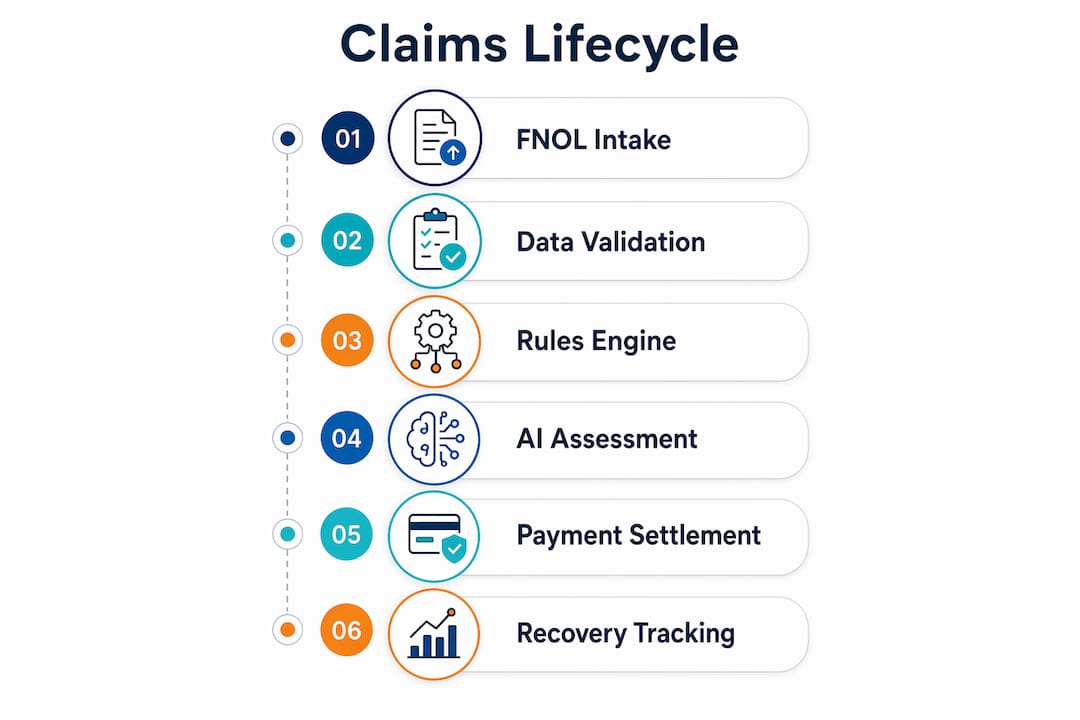

The process begins at First Notice of Loss (FNOL). In a digital system, policyholders submit claims via mobile apps, web portals, or API-connected third-party channels. Structured data enters the system immediately, triggering automated validation and routing. This replaces the traditional phone call or paper form, which required manual data entry and introduced transcription errors from the outset.

Once FNOL data is captured, the system applies a rules engine to triage the claim. Simple, low-risk claims meeting pre-set criteria move directly to settlement without human intervention. This is straight-through processing (STP). More complex claims, or those flagging anomalies, route to an adjuster queue with supporting data already assembled. The adjuster reviews a pre-populated file rather than building one from scratch.

AI layers sit above the rules engine and handle tasks that require pattern recognition rather than binary logic. These include document analysis, damage assessment from photographs, behavioural fraud scoring, and reserve recommendations. AI-powered claims systems perform 30–40% of the claims lifecycle work before a human adjuster becomes involved. That proportion frees adjusters to focus on genuinely complex cases where human judgement adds value.

Core components of a digital claims management system

A digital claims management system is not a single application. It is a set of integrated modules, each handling a distinct stage of the claims lifecycle.

FNOL capture and validation collects structured data at intake, validates policy coverage in real time, and flags missing information before the claim progresses. Clean data at this stage is the foundation for every automated step that follows.

STP rules engine applies deterministic logic to auto-adjudicate eligible claims. STP automates based on coverage type, fraud score thresholds, and claim value limits. It does not learn or adapt; it executes configured rules consistently and at scale.

AI adjudication layer supplements STP with machine learning models that analyse documents, assess damage from images, and score claims for fraud risk using behavioural analytics. This layer handles the grey areas that rules engines cannot resolve.

Fraud detection and analytics cross-references claim data against historical patterns, third-party databases, and network link analysis to identify suspicious submissions before payment is authorised.

Digital payment and settlement processes approved claims through direct bank transfer or digital payment rails, generating automated settlement letters and closing the claim record without manual intervention.

Subrogation and recovery tracking identifies recovery opportunities automatically and initiates the subrogation process, which is frequently overlooked in manual operations due to workload pressure.

Pro Tip: Before selecting a platform, map your current FNOL data fields against the system’s intake schema. Gaps here cause downstream automation failures that no AI layer can compensate for.

Modern systems use modular architectures that connect to legacy policy administration and billing platforms via APIs. Carriers prefer modular integration over full replacement because it allows iterative improvement of individual lifecycle stages without operational disruption.

What are the measurable benefits of digital claims management?

The financial case for digital claims processing is well documented. Per-claim costs fall from the £15–£22 range typical of manual operations to £3–£5 with full automation. That reduction reflects lower labour input, fewer errors requiring rework, and faster cycle times that reduce reserve holding periods.

Cycle time compression is equally significant. Claims that previously took 14 days to settle can close in under 24 hours when they meet STP criteria. That speed directly affects customer satisfaction. Policyholders who receive fast, transparent claim settlements are measurably more likely to renew and less likely to escalate complaints to regulators.

Accuracy improves because automated systems apply rules consistently. A human adjuster working under time pressure may miss a coverage exclusion or miscalculate a reserve. A rules engine applies the same logic to every claim, every time. This consistency reduces errors, supports audit trails, and simplifies regulatory reporting under frameworks such as Solvency II.

Operational scalability is a less-discussed but equally important benefit. A manual claims operation scales by hiring. A digital operation scales by configuration. When claim volumes spike after a weather event, a digital system absorbs the increase without proportional cost growth. That elasticity is a material advantage for P&C insurers managing catastrophe exposure.

For a detailed breakdown of how these efficiency gains translate into process improvements, the claims processing efficiency guide from Ibapplications covers practical steps insurers are taking across European markets.

How digital claims workflows differ from manual processes

Manual claims handling is characterised by sequential, human-dependent steps. Each handoff between departments introduces delay and the risk of data loss. A claim submitted by post or phone requires manual data entry, physical document storage, and repeated follow-up calls to gather missing information. Fraud detection relies on adjuster experience rather than systematic analysis.

Digital workflows replace sequential handoffs with parallel, automated processes. The key differences are structural, not cosmetic.

- Intake: Digital systems capture structured data at submission. Manual systems transcribe unstructured information, introducing errors immediately.

- Triage: AI and STP route claims in seconds based on risk and complexity. Manual triage depends on adjuster availability and judgement, creating bottlenecks.

- Communication: Digital platforms send automated status updates at each lifecycle stage. Manual operations rely on outbound calls, which are inconsistent and resource-intensive.

- Fraud detection: Automated systems score every claim against fraud indicators in real time. Manual review catches only the cases an adjuster recognises as suspicious.

- Audit trail: Digital systems log every action, decision, and communication automatically. Manual records are incomplete by nature and difficult to reconstruct for regulatory review.

Modern claims platforms are shifting from systems of record to systems of action, managing claims proactively through real-time risk modelling rather than reacting to adjuster input. That shift fundamentally changes the role of the claims adjuster from data processor to decision-maker.

Pro Tip: Do not automate your current manual process as-is. Map the process first, remove the steps that exist only because of manual constraints, then build the digital workflow around what remains.

How to implement digital claims management successfully

Successful implementation follows a sequence. Skipping steps, particularly the early data and process steps, causes failures that no technology investment can recover.

-

Standardise FNOL data inputs. Without machine-readable FNOL data, AI workflows fail to deliver benefits. Define mandatory fields, validation rules, and acceptable formats before selecting a platform.

-

Audit existing processes before automating. Layering AI on broken manual processes causes failure. Identify which steps add value and which exist only to compensate for manual limitations.

-

Adopt modular integration. Modular integration preserves existing infrastructure while enabling incremental digitalisation. Start with FNOL and STP, then extend to AI adjudication and fraud analytics as confidence grows.

-

Set realistic automation targets. Realistic STP targets for personal lines sit between 40% and 70% of claim volume. Targeting 100% automation introduces operational risk because edge cases always require human review.

-

Train adjusters on the new role. Adjusters in a digital operation review AI recommendations and handle complex exceptions. That requires different skills than traditional end-to-end manual handling. Invest in training before go-live, not after.

-

Monitor and refine continuously. Rules engines and AI models degrade if not maintained. Schedule regular reviews of auto-adjudication accuracy, fraud detection rates, and STP throughput to identify where rules need updating.

For a step-by-step breakdown of the automation build sequence, the claims automation guide from Ibapplications covers each phase in practical detail.

Key takeaways

Digital claims management delivers measurable efficiency, accuracy, and cost benefits when built on clean data, modular integration, and realistic automation targets.

| Point | Details |

|---|---|

| Define the process before automating | Map and simplify claims workflows before applying STP or AI to avoid embedding inefficiencies. |

| FNOL data quality is foundational | Machine-readable, structured intake data is the prerequisite for every automated step downstream. |

| STP and AI serve different functions | STP applies deterministic rules; AI handles complex pattern recognition. Both are needed for full lifecycle coverage. |

| Set realistic automation targets | Personal lines STP targets of 40%–70% of claim volume reduce risk while delivering material efficiency gains. |

| Modular integration reduces disruption | Connecting digital modules to legacy systems via APIs allows incremental improvement without full platform replacement. |

The uncomfortable truth about digital claims adoption

Having worked closely with P&C insurers across European markets on claims digitalisation projects, the pattern I see most often is this: insurers invest in a capable platform and then underperform their targets because they automated the wrong thing.

The technology is rarely the problem. The problem is that manual claims processes accumulate workarounds over years. Steps exist not because they add value but because a previous system required them. When you digitise those steps, you lock inefficiency into code. It becomes harder to see and harder to change than the paper form it replaced.

The insurers who get the most from digital claims management are the ones who treat implementation as a process redesign project with a technology component, not a technology project with a process component. That distinction sounds subtle. In practice, it determines whether you hit your automation targets or spend two years debugging a rules engine that was configured around the wrong process.

The other thing I would caution against is treating STP rate as the primary success metric. A high STP rate on low-value, low-risk claims is easy to achieve and tells you relatively little about the health of your claims operation. The more revealing metrics are adjuster time per complex claim, fraud detection accuracy, and customer satisfaction scores at settlement. Those numbers tell you whether the digital system is actually improving outcomes or just moving volume faster.

AI’s role will expand, but the fundamentals will not change. Clean data in, reliable decisions out. The insurers building that foundation now will have a genuine operational advantage as AI capabilities mature.

— Tuna

How IBSuite supports digital claims transformation

Ibapplications built IBSuite as a cloud-native, API-first platform covering the full P&C insurance value chain, including a dedicated claims management module designed for modular deployment alongside existing core systems. IBSuite supports automated FNOL capture, STP rules configuration, AI-assisted adjudication, and digital payment processing within a single integrated environment. The platform connects to legacy policy administration systems via open APIs, which means European insurers can digitalise their claims operation incrementally without replacing functioning infrastructure. For insurers also looking at how claims integrates with broader policy operations, the policy administration platform provides the connected foundation that makes end-to-end automation achievable.

FAQ

What is digital claims management in insurance?

Digital claims management is the end-to-end handling of insurance claims using automated, AI-driven platforms from first notice of loss through to settlement, replacing manual paper and phone-based processes.

How does straight-through processing differ from AI adjudication?

STP applies pre-configured business rules to auto-settle eligible claims without human input. AI adjudication analyses documents, images, and behavioural data to support decisions on more complex claims that rules alone cannot resolve.

What automation rate is realistic for personal lines claims?

Realistic STP targets for personal lines sit between 40% and 70% of claim volume. Targeting higher rates increases operational risk because edge cases and complex claims always require human review.

Why does FNOL data quality matter so much?

Structured, machine-readable data at first notice of loss is the prerequisite for every automated step downstream. Poor FNOL data causes AI workflows to fail regardless of platform capability.

How do digital claims systems reduce fraud?

Digital platforms score every claim against fraud indicators in real time using behavioural analytics, network link analysis, and historical pattern matching, identifying suspicious submissions before payment is authorised rather than after.