10.06.26

Insurance product configurators: a 2026 guide for insurers

Insurance product configurators are specialised software platforms that empower insurance professionals to configure, price, and manage insurance products using no-code interfaces and native insurance workflows. Unlike generic business rule management systems, these tools are built around insurance-specific abstractions: coverages, endorsements, rating factors, and eligibility logic. For European P&C insurers facing mounting pressure to launch products faster and comply with evolving regulation, the shift from IT-led development to business-led configuration is no longer optional. Modern configurators reduce product launch time from 12 to 18 months down to 4 to 8 weeks, giving product teams a genuine competitive edge.

How do insurance product configurators function and integrate with existing systems?

Insurance product configurators operate as a dedicated layer between your product strategy and your policy administration system (PAS). Business analysts define pricing rules, eligibility conditions, endorsements, and validation logic through a visual interface, without writing a single line of code. The configurator then executes those rules in real time across every channel: direct, broker, or API-connected aggregator.

The architecture matters here. Configurators integrate with PAS suites rather than replacing them. Your existing system continues to handle billing, claims, and financial processing, while the configurator takes ownership of product definition, rating, and underwriting logic. This hybrid stack approach is particularly valuable for mid-market European carriers that have invested heavily in their core platforms but need faster product iteration than those platforms allow.

Tools such as Higson and SSP Pure Product Studio illustrate two ends of the spectrum. Higson focuses on rule-based configuration with strong versioning and audit capabilities. SSP Pure Product Studio takes this further: AI-driven configurators convert plain language product descriptions into production-ready business rules and UI schemas without manual coding. Both approaches share a common goal: putting product control in the hands of business users rather than IT queues.

Multi-channel deployment is another critical function. A well-designed configurator publishes the same product logic to your broker portal, your direct-to-consumer website, and your internal underwriting workbench simultaneously. This eliminates the version drift that occurs when separate teams maintain separate rule sets for each channel.

Pro Tip: When evaluating configuration tools, ask vendors to demonstrate how a mid-cycle pricing change propagates across all channels. If the answer involves a development sprint, the tool is not truly business-led.

Key integration capabilities to look for include:

- REST API connectivity to existing PAS, CRM, and billing systems

- Real-time rule execution with sub-second response times for online quoting

- Support for complex product structures such as modular covers and optional endorsements

- Audit logging at the rule level, not just the transaction level

What are the key features that set insurance configurators apart?

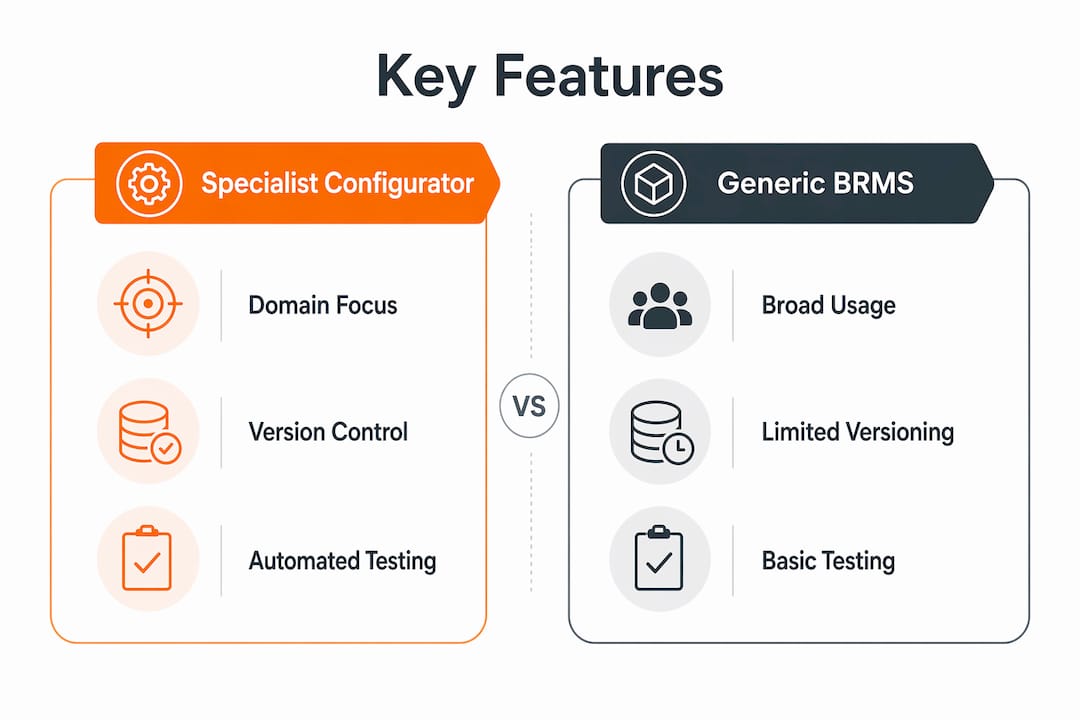

The defining difference between an insurance product configurator and a generic business rule management system is the domain model. Generic BRMS tools require you to build insurance concepts from scratch. A specialist configurator offers insurance-native abstractions for coverages, endorsements, rating factors, and multi-version product management as standard. This distinction cuts implementation time significantly and reduces the risk of modelling errors that only surface at claims time.

The table below compares the capabilities that matter most when choosing between a specialist configurator and a generic alternative:

| Capability | Specialist insurance configurator | Generic BRMS or PAS module |

|---|---|---|

| Insurance domain model | Native: coverages, endorsements, rating | Must be built from scratch |

| Versioning and rollback | Self-service, business-user controlled | Typically requires IT involvement |

| Automated testing | Built-in regression testing for rules | Manual or third-party tooling required |

| Multi-channel deployment | Single configuration, all channels | Separate builds per channel common |

| Regulatory override support | Region-specific rule sets as standard | Custom development required |

Versioning and rollback features allow business users to edit and revert rules without IT involvement. This is rarer than it sounds. Most PAS modules lock rule changes behind change management processes that can take weeks. Self-service rollback means a product manager can test a pricing adjustment, observe its effect in a sandbox environment, and revert within minutes if the results are unexpected.

Automated testing is equally significant. Faster innovation does not conflict with control when platforms include automated testing, audit trails, and version control. A configurator that runs regression tests against your full product catalogue every time a rule changes gives compliance and actuarial teams the confidence to approve changes quickly rather than demanding lengthy review cycles.

Pro Tip: Build a regression test library from day one. Capture your most complex rating scenarios as test cases before you configure a single rule. This library becomes your safety net for every future change.

For European insurers managing products across multiple markets, the speed-to-market improvement is the most immediately visible benefit. Reducing a product launch from a year-long programme to a matter of weeks changes what is commercially viable. Insurers can respond to competitor moves, test new segments, and retire underperforming products on a timeline that matches market reality.

How do configurators handle product complexity and regulatory variation?

Product complexity in insurance is not just about the number of covers on a policy. It is about managing multiple concurrent product versions, each with its own rating logic, eligibility rules, and endorsement sets, while ensuring that new business binds to the current version and in-force policies adhere to their original terms. True product configuration excellence requires exactly this: concurrent version management where each policy generation is governed by the rules that were active at inception.

Regulatory variation adds another dimension. European insurers operating across multiple jurisdictions face distinct regulatory requirements in each market. A configurator must support isolated, country-specific rule overrides that can be independently versioned and governed for regulatory compliance. This is not a minor feature. It is the difference between a single configurable product that serves ten markets and ten separate product builds that each require their own maintenance cycle.

The distinction between configurability and customisation is critical here, and it is frequently misunderstood. Structured configurability means adaptation within defined parameters, which avoids the operational strain and upgrade friction that unlimited customisation creates. When every insurer bends a platform to their unique requirements through bespoke code, the platform becomes unmaintainable and regulatory updates become expensive projects rather than configuration tasks.

Practical capabilities that address complexity and compliance include:

- Concurrent version management: new business on v3.2, renewals on v3.1, run-off on v2.0

- Country or region-specific rule override sets that inherit from a master product template

- Structured eligibility matrices that prevent invalid product combinations at the point of sale

- Policy lifecycle alignment so that endorsements, mid-term adjustments, and renewals all reference the correct product version

The compliance management advantages of modern configurable platforms are particularly relevant for insurers subject to Solvency II reporting requirements or national regulatory mandates that change on short notice. When a regulator requires a pricing adjustment or a new disclosure, a configurator makes that a configuration task rather than a development project.

What practical steps should insurance teams take to implement configurators?

Implementation success depends far more on governance discipline than on technology selection. The most capable configurator will underperform if the business processes around it are not designed with the same care as the tool itself. Best practices centre on business-led workflows, avoiding customisation bloat, and aligning product design with administration and claims processes from the outset.

Follow these steps to build a sustainable configuration practice:

-

Define your product taxonomy before you configure anything. Map every cover, endorsement, rating factor, and eligibility condition across your current product catalogue. This exercise reveals duplication and inconsistency that will otherwise be replicated in your new configurator.

-

Establish a configuration governance board. This group, typically comprising product management, actuarial, compliance, and IT, approves all rule changes before they reach production. The board should meet weekly, not monthly, to maintain the pace that configurators make possible.

-

Build repeatable frameworks through policy lifecycle services. Disciplined policy lifecycle services align product design and administrative frameworks, preventing costly one-off customisations later. Define how endorsements, renewals, and cancellations behave at the framework level, then configure individual products within those boundaries.

-

Resist the temptation to configure every edge case. Customisation bloat is the most common failure mode. When a product team requests a bespoke rating rule for a single distribution partner, the correct answer is usually to model it within the existing framework or decline it. Every exception adds maintenance overhead.

-

Leverage audit trails as a management tool, not just a compliance artefact. A full audit trail of who changed what rule, when, and why is invaluable during regulatory reviews and post-incident analysis. Train your product team to treat the audit log as a living record of product decisions.

-

Align product configuration with claims and underwriting from day one. The product management and claims integration relationship is often overlooked during configurator implementation. Cover definitions that are ambiguous at configuration time become disputed claims at settlement time.

The role of AI and automation in configuration is growing rapidly. AI tools that translate product specifications into rule sets reduce the configuration effort for new products and lower the skill threshold for business users. This is moving from experimental to operational across European carriers, and insurers that build the governance frameworks now will be best placed to adopt these capabilities as they mature.

Key takeaways

Insurance product configurators deliver measurable speed, control, and compliance advantages when implemented with disciplined governance and a clear separation between configuration and customisation.

| Point | Details |

|---|---|

| Speed to market | Specialist configurators reduce product launch time from over a year to 4 to 8 weeks. |

| Integration, not replacement | Configurators sit alongside existing PAS systems, handling product logic while PAS manages billing and claims. |

| Governance is non-negotiable | Versioning, rollback, and automated testing make speed and control compatible, not competing priorities. |

| Configurability has limits | Structured configurability within defined parameters prevents the customisation bloat that stalls future updates. |

| Regulatory complexity is manageable | Country-specific rule override sets, independently versioned, are the correct approach for multi-jurisdictional European insurers. |

Why the balance between speed and control is the real prize

I have seen insurers treat configurators as a technology purchase and then wonder why the promised speed gains never materialise. The tool is rarely the problem. The problem is that the organisation has not changed how it makes product decisions. A configurator gives your product team the ability to change a rating rule in an afternoon. If that change still requires a three-week approval cycle, you have bought agility you cannot use.

The insurers who get the most from these platforms are the ones who redesign their governance alongside their technology. They create lightweight approval processes that are fast by design, not slow by default. They train product managers to own configuration rather than hand requirements to IT. They treat the audit trail as a strategic asset rather than a compliance burden.

There is also a selection problem worth naming directly. Not every tool marketed as an insurance product configurator is genuinely insurance-native. Some are generic rule engines with an insurance-flavoured interface. The test is simple: ask the vendor to show you how their tool models a multi-section commercial property product with location-specific rating and mid-term endorsement handling. If the demonstration requires significant custom development, the tool is not what it claims to be.

The speed-to-value question for insurance product management is ultimately about organisational readiness as much as platform capability. The technology is mature. The governance frameworks are well understood. The insurers who move fastest are those who commit to both simultaneously.

— Tuna

How IBSuite supports modern insurance product configuration

Ibapplications built IBSuite specifically for P&C insurers who need to move faster without sacrificing control. IBSuite’s policy administration capabilities include a product configuration layer that allows business teams to define covers, rating logic, eligibility rules, and endorsements without IT dependency. The platform supports concurrent product versioning, multi-channel deployment, and full audit trails as standard. Built on AWS and designed with an API-first architecture, IBSuite connects to your existing systems rather than demanding a wholesale replacement. If you are evaluating modern insurance platform features for your next configuration project, IBSuite is worth a close look.

FAQ

What is an insurance product configurator?

An insurance product configurator is a specialist software platform that enables business users to define, price, and manage insurance products using no-code rule authoring and insurance-native abstractions such as coverages, endorsements, and rating factors. It sits alongside a policy administration system rather than replacing it.

How long does it take to launch a product using a configurator?

Modern configurators reduce new product launch time from 12 to 18 months to 4 to 8 weeks, using business-led workflows and no-code rule authoring that remove IT bottlenecks from the product design process.

How do configurators handle regulatory differences across European markets?

Specialist configurators support country-specific rule override sets that are independently versioned and governed, allowing a single master product template to be adapted for each jurisdiction without creating separate product builds.

What is the difference between configurability and customisation?

Configurability means structured adaptation within defined parameters, which keeps the platform maintainable and upgradeable. Customisation means bespoke code changes that accumulate over time, increasing operational strain and making regulatory updates expensive to implement.

Do configurators replace existing policy administration systems?

No. Configurators integrate with existing PAS platforms, taking ownership of product definition, pricing, and underwriting logic while the PAS continues to handle billing, claims, and financial processing.

Recommended

- Insurance Customer Experience: Complete Guide for 2025 – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance marketplace models 2026: 50% faster launches

- Rapid Insurance Product Innovation Guide for P&C Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- How Insurers Can Launch Digital Products Fast – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System