03.06.26

Insurance rate quoting explained: a 2026 guide

Insurance rate quoting is the process by which an insurer calculates an estimated premium for a policyholder by applying carrier-specific rates to risk and coverage data. The industry term for this process is premium rating, and understanding it gives you a direct advantage when comparing policies and managing costs. Whether you are insuring a vehicle, a commercial property, or a workforce, the quote you receive is shaped by a rating engine processing dozens of variables before a single figure appears on your screen. This guide explains how that process works, what drives the numbers, and how to use quotes intelligently.

What is insurance rate quoting and why does it matter?

Insurance rate quoting is the structured method insurers use to translate risk data into a price estimate. It sits at the start of every insurance transaction and determines whether a policy is affordable, appropriate, and competitive.

The process begins when you submit information to an insurer or broker. A rating engine then applies the carrier’s filed rates to your specific exposure profile. The output is a quote: an estimated premium based on the data you have provided and the assumptions the insurer makes before full underwriting. State Farm describes quotes as detailed price estimates tailored to the coverage, limits, and deductibles you select, not as final bills.

For consumers, understanding this distinction prevents surprise. For businesses, it enables more precise budgeting and more productive conversations with brokers. The quote is the starting point, not the destination.

What factors affect insurance rate quotes?

Common factors in insurance rate quoting include accident history, vehicle or business details, coverage choices, and location-based risk characteristics. Each factor feeds directly into the insurer’s estimate of future claim costs.

Here is how the main inputs influence your quote:

- Claims history. A record of previous claims signals higher future risk. Even a single at-fault accident can increase a motor insurance quote significantly for three to five years.

- Location. Urban postcodes typically carry higher theft, accident, and weather-related risk than rural areas. Insurers apply area-specific factors to reflect this.

- Coverage levels and deductibles. Higher limits increase the insurer’s potential payout and therefore raise the premium. A higher excess (deductible) shifts more risk to you and reduces the quoted price.

- Vehicle or business profile. For motor insurance, the make, model, engine size, and age of the vehicle all affect repair and replacement costs. For commercial insurance, the nature of the business, number of employees, and turnover are equivalent inputs.

- Credit score (where permitted). Some European insurers use credit-related data as a proxy for financial responsibility, though regulatory frameworks vary by country.

Each of these inputs influences the insurer’s estimated future claim costs and hence the premium calculation. Providing inaccurate or outdated information does not lower your final premium. It delays it, because underwriting verification will surface discrepancies and adjust the figure before the policy is issued.

Pro Tip: Before requesting any quote, gather your claims history for the past five years, confirm your registered address, and have your vehicle registration or business details to hand. Accurate inputs produce quotes that are far closer to the final premium, saving you time and avoiding unwelcome adjustments later.

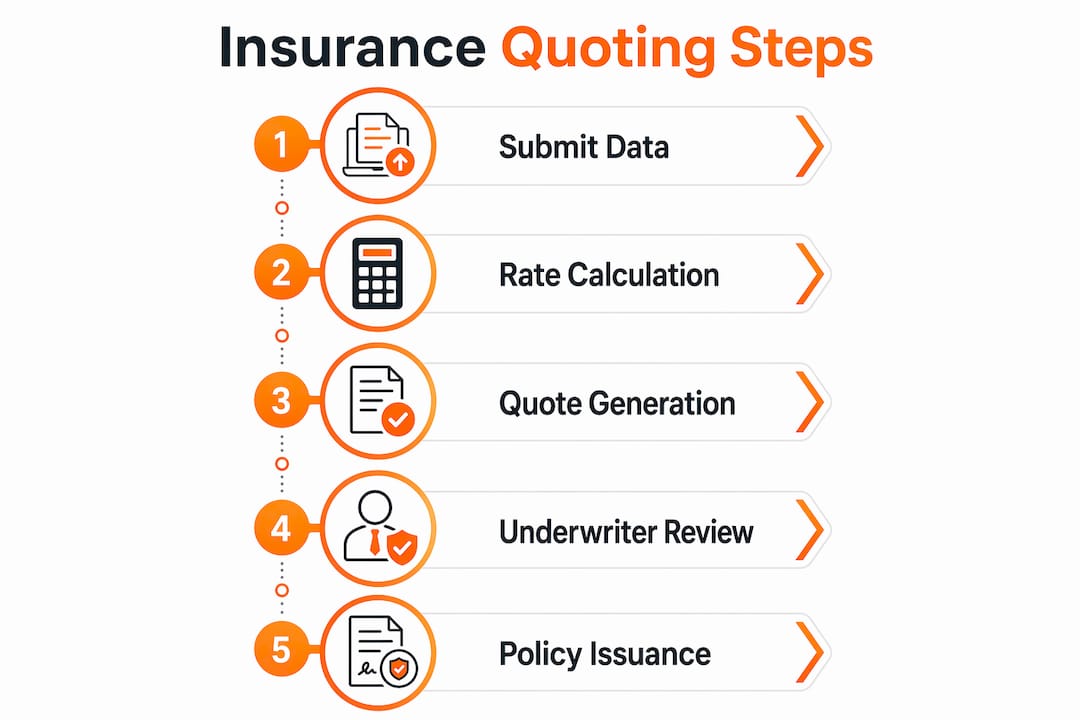

How do insurance rating engines and quoting tools work?

A rating engine is the software that applies an insurer’s filed rates to submitted data and produces a premium output. It is the computational core of every quoting system, whether that system is a simple online form or a sophisticated broker platform.

A rater is any tool that generates insurance premium quotes; carrier portals and comparative raters differ mainly in scope and complexity. Understanding the distinction helps you choose the right channel for your needs.

The data flow through a rating engine follows four stages:

- Input collection. You or your broker submits risk data: personal details, asset information, coverage preferences, and claims history.

- Risk assessment. The engine applies underwriting rules and risk factors to classify your exposure and identify applicable rate tables.

- Rate application. The carrier’s filed rates are multiplied against the relevant exposure units (for example, payroll for employers’ liability or vehicle value for motor insurance).

- Quote output. The engine produces a premium estimate, often with options showing how different coverage levels or excess amounts change the price.

Single-carrier portals run this process using one insurer’s rate tables. Comparative raters run the same data through multiple carriers simultaneously, producing side-by-side results. Different quoting channels from the same insurer may show varied quotes because of differing verification steps and assumptions, which is why the same policyholder can receive different figures from a carrier’s website versus a broker’s platform.

The most significant recent development in quoting technology is conversational AI. Liberty Mutual launched an AI quoting app inside ChatGPT in 2026, using their own rating engine to maintain pricing accuracy while meeting regulatory requirements around data privacy and disclosure. This illustrates both the opportunity and the constraint: AI can widen consumer access to quotes, but the underlying rating engine must still comply with filed rates and data governance rules.

Commercial lines quoting is more challenging than personal lines because commercial data is less standardised and fewer APIs exist to connect broker systems with carrier rating engines. This is why commercial quotes often take longer and require more manual input than a motor or home insurance quote.

Pro Tip: When using an online quoting tool, check whether it performs real-time data verification during entry. Tools that pull Motor Vehicle Records or claims data in real time produce near-final quotes. Tools that rely entirely on self-reported data will show a wider gap between the quote and the final premium.

What is the difference between a rate, a quote, and a premium?

These three terms are used interchangeably in everyday conversation, but they describe distinct stages of the pricing process. Confusing them leads to misplaced expectations.

| Term | Definition | Example |

|---|---|---|

| Rate | The price per unit of exposure, set by the insurer and filed with the regulator | £0.50 per £100 of insured payroll |

| Quote | An estimated premium calculated by applying rates to submitted data before full underwriting | £1,200 per year based on information provided |

| Premium | The final cost confirmed after underwriting verification and any adjustments | £1,340 after claims history verified |

In rate mathematics, the rate is the price per unit of exposure, while the premium is the final calculated cost after adjustments. A workers’ compensation example makes this concrete: a rate of £0.50 per £100 of payroll applied to a £500,000 payroll produces a base premium of £2,500 before discounts, surcharges, or fees are applied.

The quote sits between these two. It is the insurer’s best estimate given the data submitted, before the underwriter has verified claims records, credit data, or inspection reports. Auto insurance quotes are snapshots based on information given, not the final bill. The final premium depends on underwriting verification.

Insurance rate setting is constrained by claim cost coverage requirements and regulatory limits, which means insurers cannot simply adjust rates at will. Rate changes require regulatory approval, which is why quotes can remain stable even when claims costs are rising.

How to compare and use insurance quotes effectively

Getting a quote is straightforward. Using quotes well requires a more deliberate approach. The goal is not simply to find the lowest number but to identify the best value for the coverage you actually need.

- Compare like for like. Request quotes with identical coverage limits, excess amounts, and policy conditions from each insurer or broker. A quote that appears 20% cheaper may simply carry a higher excess or exclude a key coverage section.

- Use multiple channels. Request quotes from carrier portals, broker platforms, and comparative raters. Real-time data validation during entry improves accuracy over simplistic comparison tools, so prioritise platforms that verify data as you enter it.

- Account for discounts and surcharges. Many insurers apply no-claims discounts, multi-policy discounts, or telematics-based reductions that do not appear in a standard quote. Ask specifically what adjustments are available.

- Expect post-submission changes. Quote generation is often faster than binding a policy, as downstream document and approval coordination can add time. If your quote changes after submission, ask the insurer to explain which data point triggered the adjustment.

- Know when to use a broker. For commercial insurance, a broker adds genuine value by accessing markets that do not quote directly to consumers and by structuring coverage to match your actual risk profile. For personal lines, a comparative rater is often sufficient.

- Review coverage trade-offs critically. Reducing coverage to lower a quote is a legitimate choice, but it should be deliberate. Understand what you are giving up before accepting a lower figure. A useful reference for this is understanding why the cheapest option is not always the right one.

The API-driven integration between broker platforms and carrier rating engines is what makes multi-carrier comparison possible at speed. Where these integrations are absent, particularly in commercial lines, the comparison process becomes slower and more manual.

Key takeaways

Accurate insurance rate quoting requires consistent input data, an understanding of the rate-quote-premium distinction, and deliberate comparison across multiple channels and coverage configurations.

| Point | Details |

|---|---|

| Rate vs quote vs premium | A rate is the price per exposure unit; a quote is an estimate; the premium is the final verified cost. |

| Data accuracy matters | Inaccurate inputs produce quotes that diverge from the final premium after underwriting verification. |

| Channel choice affects output | Single-carrier portals, comparative raters, and broker platforms can produce different figures for the same risk. |

| AI quoting is advancing | Conversational AI tools like Liberty Mutual’s ChatGPT integration expand access but require accurate data and regulatory compliance. |

| Compare consistently | Quotes are only comparable when coverage limits, excess amounts, and conditions are identical across all options. |

The tension at the heart of modern quoting

I have spent considerable time working alongside insurers grappling with the gap between what quoting technology promises and what it actually delivers. The acceleration of digital quoting is real and genuinely useful. Real-time data verification, AI-powered automation, and comparative raters have made the process faster and more transparent for consumers. That is unambiguously good.

What concerns me is the growing assumption that speed equals accuracy. A quote generated in thirty seconds from a conversational AI interface is only as reliable as the data the consumer provides and the assumptions baked into the rating engine. Conversational AI quoting presents genuine opportunities but also raises challenges in data accuracy and regulatory compliance that are not yet fully resolved.

The consumers who get the most value from quoting tools are those who treat the quote as the beginning of a conversation, not the end of one. They verify what the quote includes, ask what could change it, and understand that the premium confirmed at binding may differ from the figure that first appeared on screen. That critical but confident approach is what separates informed buyers from those who are surprised when their renewal arrives.

Regulatory frameworks across Europe are also tightening around data use in automated pricing, particularly where credit data or behavioural signals feed into rating engines. This is a healthy development. It forces insurers to be more transparent about what drives a quote, which ultimately benefits everyone who buys insurance.

— Tuna

How IBSuite supports the full quoting and policy lifecycle

For insurers and brokers looking to improve the accuracy, speed, and consistency of their quoting processes, IBSuite from Ibapplications provides an end-to-end platform built for exactly this challenge. IBSuite’s policy administration capabilities connect rating engines, underwriting rules, and policy issuance within a single cloud-native system, reducing the manual steps that slow down the quote-to-bind process. The platform supports API-first integration with external data sources, enabling real-time verification that brings quotes closer to final premiums from the outset. If you are evaluating platforms for quoting, rating, or policy management, Ibapplications offers a demonstration tailored to your product lines and distribution model.

FAQ

What is insurance rate quoting?

Insurance rate quoting is the process by which an insurer applies carrier-specific rates to a policyholder’s risk and coverage data to produce an estimated premium. The resulting figure is a quote, not a confirmed price, until underwriting verification is complete.

What is the difference between a quote and a premium?

A quote is an estimated premium based on submitted information and preliminary calculations. The premium is the final cost confirmed after the insurer has verified claims history, credit data, and other underwriting factors.

What factors affect insurance rate quotes most?

Claims history, location, coverage levels, and vehicle or business profile are the primary factors. Each influences the insurer’s estimate of future claim costs and therefore the quoted price.

Why do quotes from the same insurer differ across channels?

Multi-channel quoting from a single insurer can yield different pricing outputs because different tools apply varying assumptions and data verification steps. A broker platform with real-time data checks will typically produce a more accurate quote than a basic comparison tool.

Can a quote change before the policy is issued?

Yes. Quote generation is faster than binding, and the final premium depends on underwriting confirmation. If the insurer discovers discrepancies during verification, the premium will be adjusted before the policy is issued.