18.03.26

What is an end-to-end insurance platform: a 2026 guide

Many property and casualty insurers still operate with fragmented legacy systems, believing piecemeal solutions can meet modern demands. This misconception costs the industry billions in inefficiencies annually. End-to-end insurance platforms offer a unified, cloud-native alternative that transforms operations from policy administration through claims settlement. This guide clarifies what these platforms are, how they drive digital transformation, and why they matter for P&C insurance leaders navigating 2026’s competitive landscape.

Table of Contents

- Understanding End-To-End Insurance Platforms

- How End-To-End Platforms Drive Digital Transformation In P&C Insurance

- Comparing Legacy Systems And Modern End-To-End Insurance Solutions

- Implementing An End-To-End Insurance Platform: Best Practices For P&C Insurers

- Discover Tailored End-To-End Insurance Solutions For Your Company

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Unified operations | End-to-end platforms integrate policy, claims, billing, and underwriting into one seamless system |

| Digital transformation | Modern platforms enable automation, real-time analytics, and improved customer engagement across the insurance value chain |

| Legacy replacement | Integrated solutions eliminate data silos and manual processes that plague fragmented systems |

| Strategic implementation | Phased deployment with stakeholder alignment ensures maximum return on platform investment |

Understanding end-to-end insurance platforms

An end-to-end insurance platform integrates policy administration, claims management, underwriting, and billing into a seamless system. Unlike traditional point solutions that require custom integrations, these comprehensive platforms provide unified workflows across the entire insurance value chain. They eliminate the technical debt and operational friction that accumulate when insurers cobble together disparate systems over decades.

The core functional modules work together through shared data architecture. Policy administration handles quoting, binding, and renewals. Claims management tracks incidents from first notice through settlement. Underwriting engines assess risk and price products. Billing systems manage premiums, payments, and collections. When these modules share a common database and user interface, insurers gain unprecedented visibility into their operations.

Integration delivers advantages legacy systems cannot match. Real-time data flows between modules without batch processing delays. Customer service representatives access complete policyholder histories instantly. Underwriters see claims patterns that inform pricing decisions. Finance teams reconcile transactions without manual data entry. This connectivity transforms how insurers operate.

Pro Tip: Prioritise platforms with modular architecture that lets you activate features incrementally rather than requiring full replacement of existing systems overnight.

Key components of modern insurance platforms include:

- API-first design enabling seamless integration with third-party services and distribution channels

- Cloud-native infrastructure providing scalability without capital expenditure on servers

- Configurable workflows allowing business users to modify processes without developer intervention

- Advanced analytics engines surfacing insights from operational data in real time

- Mobile-responsive interfaces supporting remote work and field operations

The shift from fragmented systems to unified platforms represents more than technology modernisation. It fundamentally changes how insurers compete by enabling product innovation, operational efficiency, and customer experience improvements that legacy architectures cannot support.

How end-to-end platforms drive digital transformation in P&C insurance

Property and casualty insurers face mounting pressure in 2026 to modernise operations whilst managing regulatory complexity and customer expectations. Traditional carriers lose market share to insurtechs that launch products in weeks rather than months. Customers demand self-service portals and instant claims processing. Regulators require detailed reporting and rapid response to compliance changes. These imperatives make digital transformation drivers impossible to ignore.

End-to-end platforms enable automation, real-time data access, and improved decision-making across insurance operations. They replace manual processes with intelligent workflows that route tasks, validate data, and trigger actions based on business rules. Underwriters spend less time on data entry and more time on complex risk assessment. Claims adjusters focus on customer service rather than paperwork. Finance teams close books faster with automated reconciliation.

The transformational benefits unfold systematically:

- Process automation eliminates repetitive manual tasks through configurable workflows and robotic process automation, reducing processing time by up to 60% for routine transactions.

- Business agility accelerates product launches from months to weeks by enabling business users to configure new offerings without IT bottlenecks or custom development.

- Regulatory compliance simplifies adherence to evolving requirements through built-in audit trails, automated reporting, and configurable rules engines that adapt to jurisdiction changes.

- Customer experience improves dramatically with self-service portals, mobile apps, and omnichannel engagement that meet modern expectations for digital interaction.

- Innovation capacity increases as insurers redirect IT resources from maintaining legacy systems to developing competitive advantages and exploring emerging technologies.

Digital transformation through end-to-end platforms is not optional for insurers who want to remain competitive. The question is not whether to modernise, but how quickly you can execute the transition whilst maintaining business continuity.

Data analytics capabilities embedded in modern platforms reveal patterns invisible to legacy systems. Insurers identify profitable segments, detect fraud earlier, and personalise pricing with precision. Machine learning models improve continuously as they process more transactions. These insights drive strategic decisions about market positioning, risk appetite, and operational priorities.

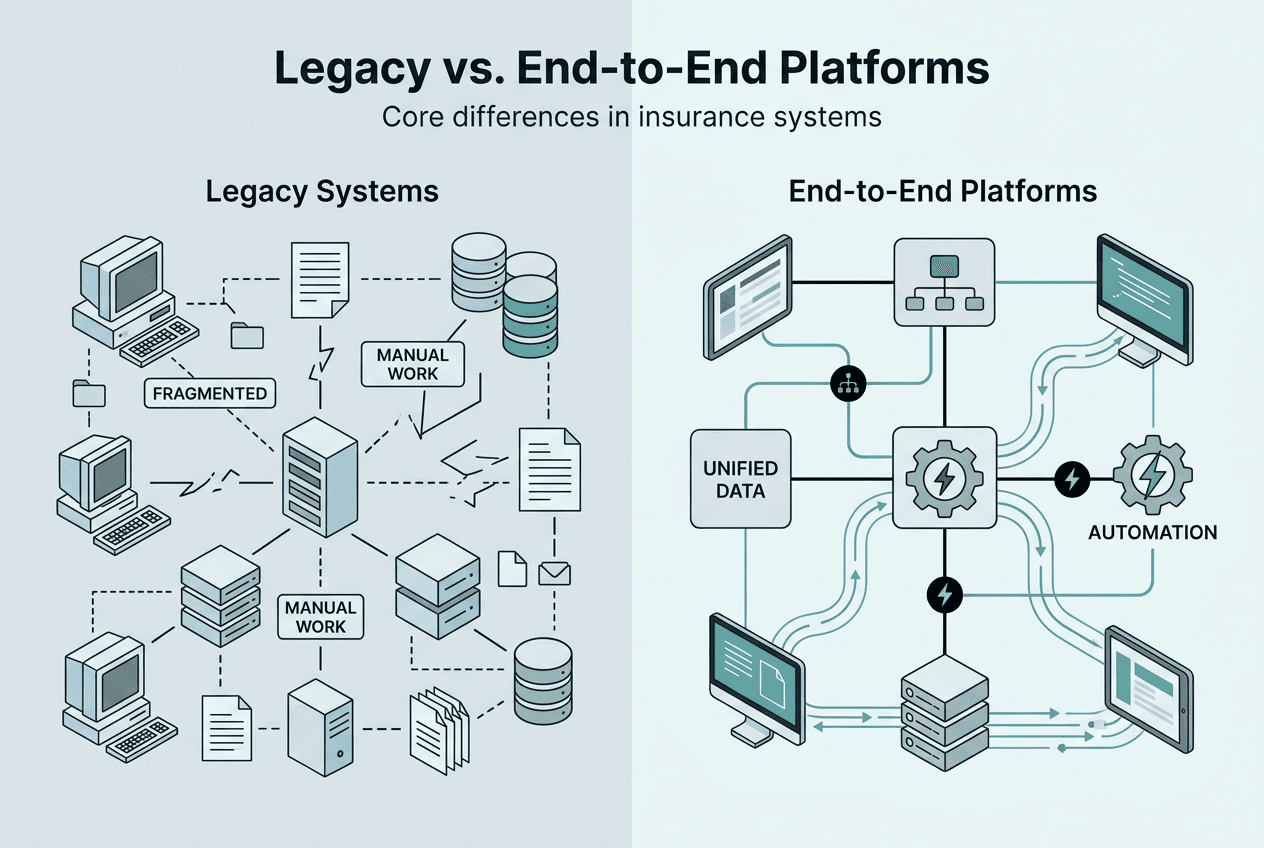

Comparing legacy systems and modern end-to-end insurance solutions

Traditional insurance technology stacks evolved through acquisition and incremental addition rather than intentional design. Insurers typically operate separate systems for policy administration, claims, billing, and document management. Each system maintains its own database, user interface, and business logic. Legacy systems hamper insurers with siloed data and manual processes, creating operational friction at every handoff point.

Fragmentation manifests in concrete problems. Customer service representatives toggle between five or more screens to answer simple questions. Data inconsistencies emerge when information updates in one system but not others. Reporting requires extracting data from multiple sources and reconciling differences manually. Compliance becomes challenging when audit trails span disconnected systems. Innovation stalls because changing one component risks breaking integrations with others.

Next-generation insurance platforms provide unified data models, automated workflows, and elastic scalability that legacy architectures cannot match. They eliminate integration complexity by design rather than attempting to bridge incompatible systems. Modern platforms support continuous updates without disruptive version upgrades. Cloud infrastructure scales capacity dynamically to handle peak loads without over-provisioning hardware.

| Aspect | Legacy Systems | End-to-End Platforms |

|---|---|---|

| Data architecture | Siloed databases requiring custom integrations | Unified data model with real-time synchronisation |

| Deployment model | On-premises servers with capital expenditure | Cloud-native SaaS with operational expenditure |

| Update cycle | Major upgrades every 3-5 years with downtime | Continuous updates with zero disruption |

| User experience | Multiple interfaces requiring separate training | Consistent interface across all functions |

| Compliance management | Manual tracking across disconnected systems | Automated audit trails and regulatory reporting |

| Innovation speed | Months to implement new products | Weeks to configure and launch offerings |

Critical considerations when assessing platform options include:

- Total cost of ownership including licensing, implementation, training, and ongoing support rather than just initial purchase price

- Migration strategy and timeline for transitioning from existing systems without business disruption

- Vendor stability and roadmap to ensure long-term viability and continued innovation

- Integration capabilities with existing tools, data sources, and distribution channels you plan to retain

- Customisation limits and configuration flexibility to support your unique business processes

Pro Tip: Evaluate platform compliance capabilities specifically aligned with regulations in your operating jurisdictions, as generic solutions may require expensive customisation for local requirements.

Implementing an end-to-end insurance platform: best practices for P&C insurers

Successful platform adoption requires more than selecting the right technology. Insurers must align implementation with strategic business objectives, engage stakeholders across functions, and manage change systematically. A strategic implementation roadmap, stakeholder engagement, and continuous optimisation are key to leveraging platforms effectively rather than simply replacing old problems with new ones.

Phased deployment minimises risk whilst building organisational capability. Attempting to replace all systems simultaneously overwhelms teams and magnifies the impact of unforeseen issues. Incremental rollout allows learning from early phases to inform later stages. Success breeds confidence and support for continued investment.

Follow this proven implementation sequence:

- Assessment phase involves documenting current state processes, identifying pain points, and defining success metrics that align technology investment with business outcomes.

- Vendor selection requires evaluating platforms against functional requirements, conducting proof of concept testing, and negotiating contracts that protect your interests.

- Pilot deployment starts with a single product line or business unit to validate the platform, train super users, and refine configurations before broader rollout.

- Staged rollout expands the platform to additional products and regions systematically, applying lessons learned and maintaining business continuity throughout the transition.

- Optimisation cycle establishes ongoing performance monitoring, user feedback collection, and continuous improvement to maximise return on platform investment over time.

Common implementation challenges have proven solutions:

- Data migration complexity requires early profiling of source systems, cleansing efforts to improve quality, and parallel running to validate accuracy before cutover

- User resistance diminishes through early involvement in design decisions, comprehensive training programmes, and celebrating quick wins that demonstrate tangible benefits

- Integration issues surface during proof of concept testing rather than production deployment when you validate connections with critical third-party systems upfront

- Scope creep threatens timelines when you lack clear governance processes for evaluating change requests against strategic priorities and resource constraints

- Performance problems emerge under load testing that simulates peak transaction volumes before go-live rather than discovering capacity limits with live customers

Cross-functional teams representing underwriting, claims, IT, finance, and customer service ensure the platform serves actual business needs rather than theoretical requirements. Executive sponsorship provides authority to make difficult decisions and allocate necessary resources. External expertise from implementation partners accelerates deployment by applying lessons from previous projects.

Post-implementation success depends on treating the platform as a living system requiring continuous attention. Monitor key performance indicators to identify optimisation opportunities. Collect user feedback systematically and prioritise enhancements. Stay current with platform updates to benefit from new capabilities. Review business processes periodically to eliminate workarounds that undermine platform value.

The digital transformation roadmap extends beyond initial deployment to ongoing evolution. As your organisation builds capability with the platform, you can tackle more ambitious initiatives like predictive analytics, embedded insurance, and ecosystem partnerships that create competitive advantages.

Discover tailored end-to-end insurance solutions for your company

Transforming your insurance operations with an end-to-end platform represents a significant strategic decision. Understanding how modern platforms address your specific challenges requires hands-on exploration beyond theoretical descriptions. IBSuite provides cloud-native insurance technology designed specifically for property and casualty carriers seeking to accelerate digital transformation whilst maintaining operational stability.

Experience platform capabilities directly through a personalised demonstration. Book a demo to see how unified workflows, automated processes, and real-time analytics transform insurance operations. Our specialists configure demonstrations around your business priorities, whether you focus on product innovation, operational efficiency, or customer experience enhancement.

Evaluating modern insurance platform features against your requirements ensures the solution fits your strategic direction. Consider how API-first architecture supports your distribution strategy, whether configurable workflows match your operational complexity, and how cloud infrastructure aligns with your IT philosophy. The right platform grows with your business rather than constraining future possibilities.

Frequently asked questions

What is an end-to-end insurance platform?

An end-to-end insurance platform is a unified software system that manages the complete insurance value chain from policy administration through claims settlement. Unlike legacy point solutions, these platforms integrate underwriting, policy management, billing, claims, and customer relationship management into a single system with shared data and workflows. Modern platforms typically operate as cloud-native SaaS solutions with API-first architecture enabling seamless integration with third-party services and distribution channels.

How does an end-to-end insurance platform improve operational efficiency?

End-to-end platforms eliminate manual data entry and system switching that plague fragmented legacy architectures. Automated workflows route tasks intelligently based on business rules, reducing processing time for routine transactions by up to 60%. Real-time data synchronisation across modules prevents inconsistencies and duplicate effort. Staff focus on value-adding activities like customer service and complex decision-making rather than administrative tasks.

What are the key features to look for in an end-to-end insurance platform?

Prioritise platforms offering modular architecture that allows incremental adoption, API-first design supporting ecosystem integration, and cloud-native infrastructure providing elastic scalability. Essential capabilities include configurable workflows enabling business users to modify processes without coding, embedded analytics surfacing operational insights, and comprehensive compliance tools managing regulatory requirements. Evaluate key platform features against your specific business priorities and technical requirements.

How can P&C insurers ensure successful implementation of an end-to-end platform?

Successful implementation requires phased deployment starting with pilot projects that validate the platform and build organisational capability before full rollout. Engage cross-functional teams representing all affected departments to ensure the solution serves actual business needs. Invest in comprehensive training and change management to overcome user resistance. Establish clear governance processes for managing scope and prioritising enhancements. Follow proven implementation best practices to maximise return on platform investment whilst minimising disruption.

Recommended

- Why Choose End-to-End Platforms for Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- End-to-End Insurance Platforms: Unlocking P&C Success

- Modern Insurance Platforms: What to look for – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- End-to-End Insurance Solutions: Accelerating Digital Transformation