04.05.26

Insurance billing systems: how they drive efficiency and trust

Billing is rarely the first thing on a P&C executive’s agenda when they sit down to plan digital transformation. Yet billing leakage alone carries a 4 to 5% revenue risk when managed inconsistently, a figure that would demand immediate boardroom attention if it appeared on a claims report. The truth is that billing systems sit at the intersection of every critical insurance function: policy administration, claims, compliance, and customer experience. This article cuts through the confusion, explaining how modern insurance billing systems are structured, why integration matters, and what it takes to lead meaningful transformation in your organisation.

Table of Contents

- Why insurance billing systems matter for P&C firms

- Core components of insurance billing systems explained

- Modern billing architectures: PAS and claims system integration

- The future of insurance billing: automation and AI agents

- The uncomfortable truth: why most insurers underinvest in billing transformation

- How to take action: next steps for P&C excellence

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Billing leakage risk | Legacy billing systems can cause 4-5 percent revenue loss due to management errors. |

| Modular integration | Modern billing systems must integrate smoothly with policy and claims systems for peak efficiency. |

| AI advantage | Automation and AI address billing edge cases and improve overall operational performance. |

| Cloud-native edge | Cloud-native billing platforms empower P&C insurers to adapt quickly and reduce compliance risk. |

Why insurance billing systems matter for P&C firms

An insurance billing system is far more than a mechanism for collecting premiums. It governs the entire financial relationship between an insurer and its policyholders, from the moment a quote converts to a bound policy through to renewal, endorsement, and cancellation. Understanding insurance billing processes explained in full reveals just how many revenue-critical touchpoints billing actually controls.

The financial stakes are substantial. Billing leakage from inconsistent management carries a 4 to 5% risk, driven by manual reconciliation errors, payment misapplication, and gaps in audit trails. For a mid-sized P&C insurer writing £500 million in gross written premium, that represents up to £25 million in potential lost or misallocated revenue every year. These are not edge cases. They are systemic failures that compound over time.

Regulatory exposure is equally serious. Billing errors that result in incorrect premium notices, late cancellation warnings, or failure to meet statutory instalment requirements can draw regulatory scrutiny and damage your reputation with brokers and policyholders alike. Many jurisdictions require precise documentation of every billing event, and legacy systems often lack the audit capabilities to provide that.

Key operational challenges with legacy billing systems:

- Manual posting of payments, leading to allocation errors and delayed reconciliation

- Inability to support multiple payment methods or instalment structures without custom workarounds

- Poor integration with policy administration systems, creating data silos and duplicate entry

- Lack of real-time reporting, making it difficult to identify aged receivables or delinquency trends

- High maintenance costs for ageing codebases, diverting IT resource from innovation

“The disconnect between legacy billing infrastructure and modern payment expectations is not a technology gap. It is a strategic liability. Insurers that treat billing as administrative overhead are systematically undervaluing a function that directly influences retention, compliance, and profitability.”

Improving insurance billing process efficiency is therefore not a back-office IT project. It is a revenue protection and customer experience initiative that belongs on the executive agenda.

Core components of insurance billing systems explained

A best-in-class insurance billing system is not a single application. It is a suite of interconnected modules, each handling a specific function within the billing lifecycle. Understanding what each component does helps executives ask better questions of their technology teams and vendors.

The billing lifecycle flows in a clear sequence:

- Premium calculation receives rating outputs from the underwriting or rating engine and translates them into the correct instalment schedule for a given policy.

- Invoicing generates and distributes billing notices to policyholders or agents, whether via post, email, or a self-service portal.

- Payment processing captures incoming payments across multiple channels, including direct debit, card, bank transfer, and third-party payment providers.

- Cash allocation matches payments to the correct policy and instalment, a step where legacy systems cause finance disconnects when automation is absent.

- Collections management handles overdue accounts, generating dunning notices, suspense postings, and escalation workflows for delinquent policies.

- Reconciliation compares posted payments against bank statements and general ledger entries to ensure financial accuracy.

- Reporting and analytics provides management with real-time visibility into receivables, delinquency rates, payment method trends, and instalment performance.

The impact of billing on P&C insurers becomes most visible when these modules fail to communicate with one another. That is precisely the risk with siloed legacy configurations.

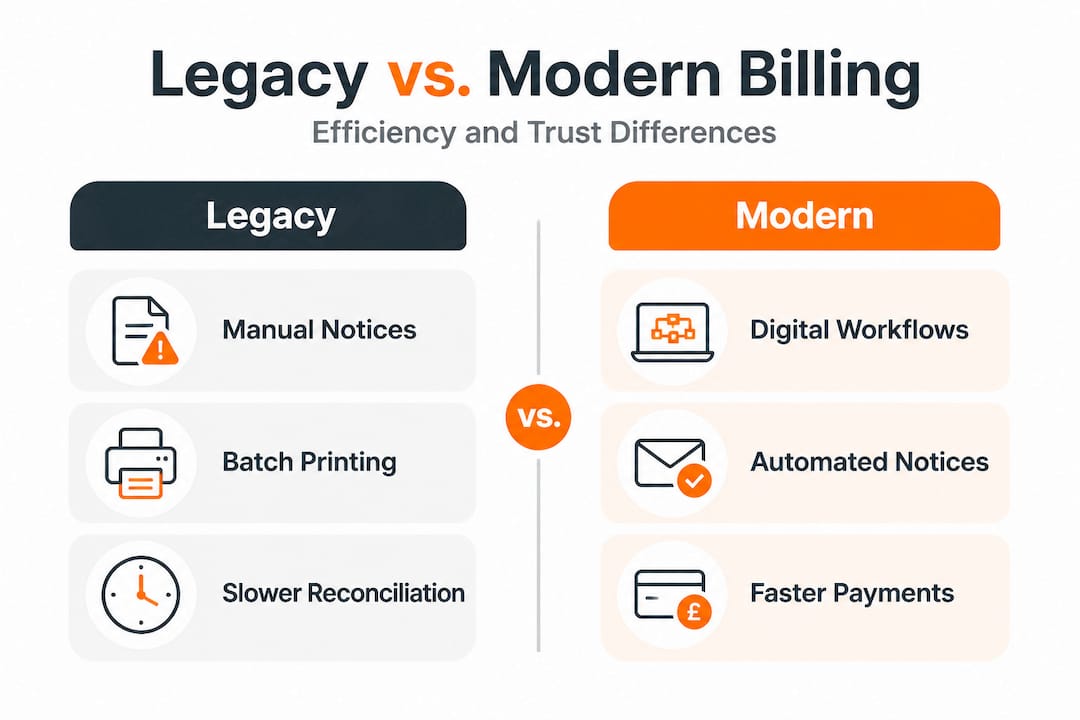

| Billing module | Legacy approach | Modern approach | Key benefit |

|---|---|---|---|

| Invoicing | Batch printed notices | Real-time digital delivery | Faster policyholder communication |

| Payment processing | Limited channels, manual entry | Omnichannel, automated posting | Reduced errors and friction |

| Cash allocation | Manual matching by finance teams | Rules-based automated matching | Elimination of misallocation |

| Collections | Static dunning schedules | Dynamic, risk-based workflows | Improved recovery rates |

| Reconciliation | End-of-month manual process | Continuous automated reconciliation | Real-time financial accuracy |

| Reporting | Static scheduled reports | Live dashboards and configurable MI | Faster executive decision-making |

Pro Tip: One of the most commonly overlooked legacy configuration pitfalls is the instalment schedule setup. Many older systems default to calendar-month billing cycles rather than policy anniversary cycles, creating persistent premium shortfalls and reconciliation noise that finance teams spend hours correcting every month. Audit your instalment logic before any migration.

Modern billing architectures: PAS and claims system integration

Knowing what each billing module does is only half the picture. The real efficiency gains come from how billing systems connect to the broader insurance technology estate, specifically to the Policy Administration System (PAS) and Claims Management System.

In a modern P&C environment, these three systems must operate as a unified platform rather than separate applications exchanging files on a nightly batch. When a policy is endorsed mid-term, the PAS should trigger an immediate premium adjustment in the billing system, which then issues a revised notice and updates the instalment schedule in real time. When a claim is settled and a premium credit applies, the claims system should communicate that directly to billing without manual intervention. That level of integration is what insurance billing automation benefits actually delivers in practice.

Gartner Peer Insights on SaaS P&C core platforms consistently highlights that cloud-native, configurable billing integrated with PAS and claims delivers measurable efficiency gains, while AI agents are increasingly being used to address edge cases like delinquencies dynamically.

| Architecture | Legacy point-to-point | Modern integrated platform |

|---|---|---|

| Data flow | Nightly batch file transfers | Real-time API-driven events |

| Configuration | Hard-coded, vendor-dependent | Self-service configurable workflows |

| Payment methods | Limited, often single-channel | Omnichannel with third-party connectors |

| Customer experience | Delayed notices, manual corrections | Instant updates, self-service portal |

| Compliance reporting | Manual extraction and formatting | Automated, audit-ready outputs |

| Scalability | Expensive custom development | Elastic cloud scaling |

Practical steps for achieving integration readiness:

- Map every data exchange between your billing, PAS, and claims systems to identify batch dependencies that need replacing with real-time API calls

- Standardise your policy and claim event taxonomy so that all three systems speak the same language when triggering billing actions

- Assess your policy administration systems for API readiness before selecting a billing platform

- Evaluate whether your claims management integration supports bidirectional premium adjustment events

- Define your payment channel strategy upfront, including whether an integrated payments bundle fits your regional requirements

Pro Tip: When evaluating third-party payment connectors, always test the failure mode, not just the success path. Legacy point-to-point integrations often handle payment rejections poorly, leaving amounts in suspense for days. A modern integration should handle declined payments, retry logic, and exception routing automatically, without human intervention.

The future of insurance billing: automation and AI agents

Automation in insurance billing is not new. Rules-based matching, scheduled dunning notices, and auto-posting of direct debit collections have existed for years. What is new is the application of machine learning and AI agents to the genuinely messy, exception-heavy parts of the billing process that rules alone cannot handle.

AI in insurance billing is already moving beyond simple automation into territory that previously required significant human judgement. The practical implications are significant for P&C executives evaluating their next technology investment.

Key use cases for AI in insurance billing:

- Delinquency prediction and intervention: AI models analyse payment behaviour patterns to identify policyholders at risk of lapsing before they actually miss a payment, enabling proactive outreach rather than reactive collections

- Intelligent cash allocation: Machine learning models resolve unmatched payments by cross-referencing policy numbers, amounts, agent codes, and historical payment patterns, dramatically reducing suspense balances

- Fraud detection in payment channels: Anomaly detection flags unusual payment behaviour such as sudden changes in account details, multiple failed attempts, or unusually large overpayments before they escalate

- Dynamic collections workflows: Rather than applying a static dunning schedule, AI agents assess individual policyholder risk profiles and adjust the communication cadence, tone, and channel accordingly

- Customer communication personalisation: Natural language generation tools create billing communications tailored to the individual policyholder’s history, product type, and preferred channel

“AI agents address edge cases like delinquencies dynamically, resolving scenarios that would previously require experienced finance staff to intervene manually. The implication for P&C insurers is clear: automation is no longer about replacing simple tasks. It is about augmenting complex human judgement at scale.”

To assess your organisation’s automation readiness, start by quantifying the volume of manual interventions your billing team makes each month and categorising them by type. High volumes of cash allocation exceptions or dunning overrides are strong indicators that AI-assisted automation would deliver immediate return on investment.

The uncomfortable truth: why most insurers underinvest in billing transformation

We have worked with P&C insurers across multiple markets, and we have observed a consistent pattern: billing transformation consistently loses the internal funding battle to underwriting tools, customer portals, and claims automation. The reason is almost always political rather than financial.

Billing is invisible when it works. No broker complains about seamless premium collection. No executive celebrates a zero-suspense balance month. But claims automation produces visible wins: faster settlements, happier customers, measurable NPS improvements. That visibility makes it easier to justify investment, even when the financial return from billing modernisation is demonstrably larger.

The hidden cost of deferring billing transformation compounds every year. Legacy billing platforms accumulate technical debt at a rate that most IT teams significantly underestimate. Maintaining custom reconciliation scripts, managing nightly batch failures, and training new finance staff on arcane workarounds are costs that never appear on a transformation business case but are very real in the annual operating budget.

Modern insurance platform benefits extend well beyond the billing function itself. When billing is modernised as part of a broader core system transformation, the downstream benefits to finance, compliance, and customer service teams are immediate and measurable.

“The insurers who treat billing as a strategic asset rather than a utility consistently outperform their peers on retention metrics. Policyholders who experience friction at the point of payment are significantly more likely to lapse at renewal, and that correlation is consistently underweighted in transformation business cases.”

Pro Tip: To build executive buy-in for billing modernisation, reframe the conversation from cost to risk. Quantify the revenue leakage your current system generates, price the regulatory exposure from compliance gaps, and model the retention impact of payment friction. Present billing transformation as revenue protection, not infrastructure spend.

How to take action: next steps for P&C excellence

The case for modernising your billing system is clear, and the technology to do so has never been more mature or accessible. IBA’s IBSuite platform delivers a fully integrated, cloud-native billing engine that connects seamlessly to policy administration and claims management within a single, API-first architecture. IBSuite supports omnichannel payment collection, configurable instalment structures, real-time reconciliation, and AI-assisted collections workflows, all maintained through Evergreen updates that ensure you are never left on an outdated release. If you are ready to understand what billing transformation could deliver for your organisation, book a platform demo with our team and we will map the opportunity against your current environment.

Frequently asked questions

What is the main function of a billing system in insurance?

An insurance billing system automates invoicing, payment processing, and account reconciliation for policies, reducing manual errors and boosting efficiency. Modern platforms go further by connecting these functions in real time with policy and claims data, eliminating the finance disconnects that legacy systems routinely produce.

How do legacy billing systems put P&C insurers at risk?

Legacy billing systems increase the risk of revenue leakage and reconciliation errors while making compliance more challenging. Billing leakage from inconsistent management represents a 4 to 5% revenue risk, alongside manual reconciliation errors and regulatory compliance complexities that accumulate silently over time.

How does AI improve insurance billing systems?

AI agents help resolve billing edge cases like delinquencies and automate time-consuming reconciliation tasks, reducing the need for manual intervention. AI agents address delinquencies dynamically, enabling insurers to apply intelligent, risk-based collections strategies that static rules-based systems cannot replicate.

Can cloud-native billing platforms enhance integration with policy and claims systems?

Yes, cloud-native billing platforms are designed for seamless integration with policy administration and claims management systems using real-time APIs rather than batch file transfers. Cloud-native platforms integrated with PAS and claims consistently demonstrate superior efficiency gains compared to legacy point-to-point architectures.

Recommended

- Billing automation guide: streamline insurance operations

- Understanding the insurance billing process for efficiency

- Insurance Billing Processes Explained: Complete Guide – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance Billing Processes – Impact on P&C Insurers