03.05.26

Insurance API marketplaces: the executive guide

Most insurance leaders, when asked about digital transformation, immediately think of core system replacements, cloud migrations, or legacy policy administration overhauls. Those efforts matter enormously. But the next frontier of competitive differentiation is not inside your core platform. It is in how your systems connect outward, to brokers, partners, embedded distribution channels, and the broader insurance ecosystem. Insurance API marketplaces are reshaping that connectivity layer entirely, and the carriers who understand this shift earliest will claim the distribution advantages that others will spend years trying to recover.

Table of Contents

- Understanding insurance API marketplaces

- How insurance API marketplaces work in practice

- Benefits and strategic value for property and casualty insurers

- Implementation insights and transformation challenges

- Our perspective: what most insurance leaders miss about API marketplaces

- Ready to modernise your insurance partnerships?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Marketplace advantage | Insurance API marketplaces enable one integration for multiple providers, streamlining distribution and partner engagement. |

| Operational efficiency | APIs reduce integration burden, but standardising data formats and workflows is still crucial for success. |

| Strategic rollout | Treating new partner APIs as business experiments links technology change to tangible underwriting and distribution goals. |

| Continuous evolution | Ongoing testing and adaptation keep API marketplaces relevant as partner requirements and market opportunities shift. |

Understanding insurance API marketplaces

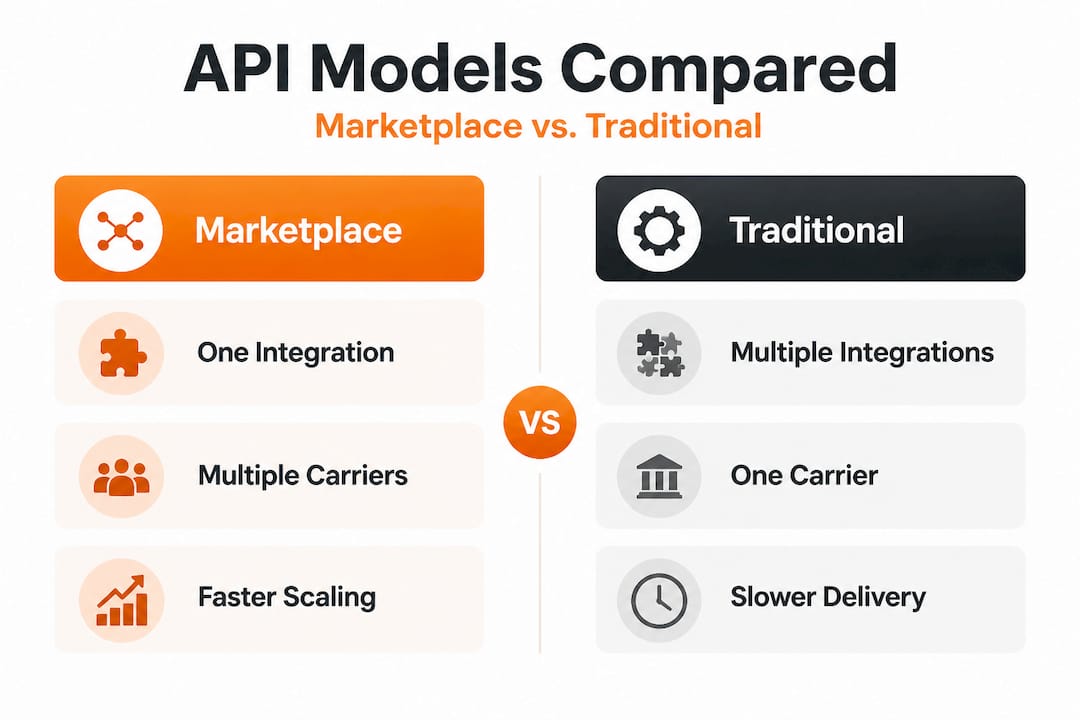

To grasp why API marketplaces are so significant, you first need a clear definition of what they actually are, and how they differ from the point-to-point integrations that most P&C insurers have been building for the past decade.

An insurance API marketplace is a unified digital environment where multiple carriers, MGAs, and product providers expose their capabilities through standardised application programming interfaces. Rather than a broker or distribution partner needing to build a separate technical connection to each carrier individually, they connect once to the marketplace layer and immediately gain access to a wide catalogue of quotes, products, and binding workflows. The API-first approach in insurance principles that underpin these marketplaces mean the architecture is designed from the ground up for interoperability, not bolted on as an afterthought.

This is a fundamentally different model from traditional API integration. In conventional B2B API integrations, each connection is bespoke. A broker integrates with Carrier A through one schema, then builds an entirely separate integration for Carrier B with different fields, different response formats, and different authentication flows. The maintenance burden alone can consume significant engineering resource over time. Insurance ecosystems, by contrast, build marketplace-like API layers where partners can submit once, receive multiple quotes, compare, and bind in their own workflow.

Key components of a mature insurance API marketplace:

- A standardised schema layer that normalises data across carrier-specific formats

- A catalogue of available products and carriers accessible through a single entry point

- Real-time quoting engines that return comparable results simultaneously

- Binding and policy issuance workflows integrated directly into the API responses

- Authentication, logging, and audit trails supporting regulatory compliance

- Versioning controls that allow marketplace updates without breaking partner integrations

The table below shows how this model compares to traditional integrations at a glance.

| Feature | Traditional API integrations | Insurance API marketplace |

|---|---|---|

| Number of connections | One per carrier/partner | One integration, multiple carriers |

| Schema standardisation | Carrier-defined, bespoke | Normalised across the marketplace |

| Maintenance burden | High, duplicated per partner | Centralised, shared maintenance |

| Time to add a new carrier | Weeks to months | Days, sometimes hours |

| Quoting workflow | Sequential, separate systems | Simultaneous, unified comparison |

| Broker/partner experience | Fragmented, inconsistent | Consistent, streamlined |

Developing a robust API strategy for insurers means recognising that the marketplace model is not just a technical convenience. It is a strategic enabler of distribution scale.

How insurance API marketplaces work in practice

Defining the concept is one thing. Seeing how it operates in a live distribution context is where the value becomes tangible for executives making investment decisions.

Consider the management liability market. Limit, a specialist platform, launched API-enabled access to Cowbell and Counterpart, allowing brokers to submit a single application, receive multiple quotes, compare, and bind instantly across both offerings. That workflow, which previously required two separate submissions with different forms and different follow-up processes, collapsed into one. The time saving per transaction is significant, but the cumulative effect across thousands of submissions is transformational.

Here is how a typical API marketplace workflow operates from submission to binding:

- Partner submission: A broker or distribution partner submits a standardised risk application through their own platform or workflow tool, which connects to the marketplace via a single API endpoint.

- Normalisation layer: The marketplace receives the submission and translates it into each carrier’s specific data requirements, handling the schema mapping behind the scenes.

- Simultaneous quoting: The marketplace sends requests to multiple carriers concurrently and collects responses in real time, rather than sequentially.

- Comparison and selection: The broker receives a normalised comparison view, showing premiums, coverage terms, and carrier ratings side by side within their own workflow.

- Binding: Once a selection is made, the binding instruction is passed back through the API to the selected carrier, triggering policy issuance and documentation without manual re-entry.

- Confirmation and audit trail: Policy documents and confirmation data are returned to the broker’s system automatically, with a full audit record maintained for compliance purposes.

This is precisely the kind of architecture underpinning the most innovative insurance marketplace models emerging across the industry. The financial API innovation driving fintech broadly applies here too: standardised connectivity reduces friction, and reduced friction drives volume.

Embedded insurance is another compelling application. When a digital property platform wants to offer landlord liability insurance at the point of lease signing, or when an e-commerce platform wants to bundle goods-in-transit cover at checkout, an API marketplace makes this commercially viable. The embedding partner does not need to understand the intricacies of each carrier’s underwriting rules. They connect once, and the marketplace handles the rest.

Pro Tip: Before committing to an API marketplace architecture, map the compliance touchpoints in your distribution workflow carefully. Jurisdictions may require explicit disclosure at specific steps, and your API design should accommodate these requirements natively rather than retrofitting them later.

Understanding what to look for in modern insurance platforms when evaluating marketplace capability is essential at this stage, particularly around latency standards, error handling, and regulatory logging built into the platform by design.

Benefits and strategic value for property and casualty insurers

The business case for insurance API marketplaces becomes clearest when you examine the value from the perspective of each stakeholder group involved in the distribution chain.

Marketplace adoption reduces time to market and integration cost, but the real competitive advantage lies in the compounding network effect: every new carrier or partner added to the marketplace increases its value exponentially for all existing participants.

The table below maps specific benefits to each stakeholder category.

| Stakeholder | Primary benefit | Secondary benefit |

|---|---|---|

| Insurance executives | Faster product launch cycles | Lower cost of distribution expansion |

| IT and architecture teams | Reduced point-to-point integration debt | Centralised version and schema control |

| Brokers and MGAs | Single workflow for multiple markets | Improved comparison and selection speed |

| End clients/policyholders | Faster quotes and binding | More competitive options in one place |

| Compliance and operations | Centralised audit trail | Standardised regulatory reporting inputs |

Core digital transformation advantages for P&C carriers:

- Distribution reach without headcount: Adding a new distribution channel through a marketplace API connection does not require proportional growth in your integration or operations teams.

- Reduced time to market: New products or endorsements can be made available to all marketplace partners simultaneously, rather than rolling out sequentially across individual connections.

- Data quality improvements: Standardised submission schemas reduce incomplete applications and data errors that slow underwriting workflows.

- Competitive intelligence: Aggregate marketplace data reveals where your products are winning, where they are being displaced, and why, at a granularity that bilateral integrations cannot provide.

- Ecosystem flexibility: As distribution channels shift, whether to embedded, digital MGA, or direct digital, the marketplace layer adapts without requiring a full re-architecture.

It is worth noting, as integration complexity research makes clear, that API marketplaces reduce integration complexity, but handling carrier-specific variants still requires mapping and translation layers. This is not a reason to avoid the marketplace model. It is a reason to invest in getting the normalisation layer right from the outset, with proper governance and schema discipline. Understanding API integration types helps architects choose the right approach for each carrier relationship within the marketplace.

The competitive edge through APIs that leading carriers are building right now is not primarily about technology. It is about the business operating model that the technology enables. Carriers who treat their API layer as a strategic asset, rather than an IT deliverable, are the ones compounding distribution advantages quarter after quarter. Robust API testing in microservices architectures also plays a critical role in maintaining marketplace reliability as the partner catalogue grows.

Implementation insights and transformation challenges

Knowing the value is one thing. Knowing how to realise it without accumulating new forms of technical debt is quite another.

Here are the key implementation steps for launching or maturing an insurance API marketplace capability:

- Define your marketplace scope: Decide upfront whether you are building a carrier-side API to expose your products to a marketplace, or whether you are building the marketplace layer itself to aggregate multiple carriers. These are distinct architectural decisions with different governance implications.

- Establish a canonical data model: Before connecting any partners, define your normalised schema. Every carrier-specific data requirement will be mapped against this canonical model, so it must be designed with flexibility in mind.

- Build the normalisation and translation layer: This is the engine room of any API marketplace. Invest in robust mapping tools and version-controlled transformation rules for each carrier relationship.

- Implement centralised testing frameworks: Use insurance software testing disciplines to validate each new carrier integration against your canonical model before going live. Regression testing after schema changes is non-negotiable.

- Design for failure and latency: Define what happens when a carrier API returns slowly or errors. Client-facing workflows must degrade gracefully rather than breaking entirely when a single carrier has an outage.

- Establish KPIs before launch: Define success metrics for each new carrier or partner integration before switching it on, covering underwriting outcomes, conversion rates, and operational throughput.

- Create a governance model for ongoing schema change: Carrier APIs evolve. Build a process for managing schema updates, communicating changes to all downstream partners, and testing changes before they reach production.

The most instructive example here comes from how Markel approaches new API integrations. Rather than treating each new partner connection as a routine IT delivery, many insurers treat new API integrations as hypotheses tested against underwriting, distribution, and claims outcomes. Each integration is a business experiment with a hypothesis, a measurement framework, and a defined decision point. That discipline is what separates carriers building genuine competitive capability from those simply accumulating integrations.

Pro Tip: Assign a named business owner, not just a technical lead, to each new API partner relationship. When an integration’s business KPIs are owned by someone in underwriting or distribution rather than IT alone, the quality of requirements, testing, and ongoing governance improves dramatically.

Aligning core system modernisation with API marketplace ambitions from the start avoids the common pitfall of building a modern API layer on top of a policy administration system that cannot support the data or workflow requirements the marketplace creates.

Our perspective: what most insurance leaders miss about API marketplaces

After working with P&C insurers through multiple waves of digital transformation, we have seen a pattern that limits the value most carriers capture from API marketplace investments. The technology is rarely the problem. The organisational model is.

Most carriers approach API marketplace initiatives as IT projects with a defined endpoint. A platform is selected, integrations are scoped, and a delivery date is set. When the integrations go live, the project is closed. What gets missed is that a marketplace is not a destination. It is a continuously evolving operating model. Partners change their schemas. New carriers join and old ones are retired. Underwriting rules shift. Regulatory requirements in different jurisdictions create new data obligations. A marketplace that is not actively governed becomes a liability faster than most executives anticipate.

The carriers who extract sustained competitive value from their marketplace investments treat the API layer as a living product with its own roadmap, its own user research (conducted with brokers and distribution partners), and its own executive sponsorship. The commercial shifts enabled by API-first platforms go far beyond technology. They touch distribution strategy, product design, underwriting authority structures, and partner commercial models.

The uncomfortable truth is that most API marketplace failures are failures of organisational will rather than technical capability. When no one in the business owns the broker experience across the marketplace, when schema changes are driven by IT convenience rather than distribution outcomes, and when carrier additions are measured by go-live dates rather than business performance, the marketplace becomes a cost centre rather than a growth engine.

Our strongest recommendation: appoint a marketplace product owner at a senior level, give them a cross-functional team, and hold them accountable for distribution outcomes. That single structural decision will do more for your marketplace’s long-term value than any technology choice you make.

Ready to modernise your insurance partnerships?

If this article has clarified what insurance API marketplaces can deliver for your organisation, the next step is understanding how your current core platform positions you to pursue that opportunity. IBSuite, IBA’s API-first, cloud-native insurance platform, is built precisely to enable the kind of marketplace connectivity and distribution agility described throughout this guide. From standardised API layers to evergreen integrations and end-to-end support across the full insurance value chain, IBSuite gives P&C carriers the foundation to build and scale marketplace capabilities without accumulating technical debt. Book a demo with our team to explore how a proven modernisation framework can accelerate your API marketplace journey.

Frequently asked questions

What is an insurance API marketplace?

It is a unified digital platform where insurers, brokers, and partners access multiple products, quotes, and binding workflows through standardised application programming interfaces. Insurance ecosystems build marketplace-like API layers where partners can submit once, receive multiple quotes, compare, and bind within a single workflow.

How does an API marketplace differ from traditional insurance integrations?

An API marketplace offers a single integration point for multiple carriers or partners, drastically reducing complexity compared to building separate connections for each party. As integration research confirms, API marketplaces reduce integration complexity, though carrier-specific variants still require careful mapping layers.

What are the business benefits of adopting an insurance API marketplace?

Key benefits include faster time to market, simplified partnerships, improved distribution reach, and operational scalability for property and casualty insurers, as well as compounding network effects as the partner catalogue grows.

What are common challenges with API marketplace deployment?

Differing data requirements, response formats, and integration discipline across carriers require careful schema design and ongoing testing. Carriers and partners frequently differ in required fields, response formats, underwriting rules, and timing, which must be handled by a robust normalisation layer.

How should new API integrations be rolled out?

Insurers should treat new integrations as business experiments, measuring outcomes across underwriting, distribution, and claims rather than simply tracking go-live dates. Many leading insurers already treat new API partner integrations as hypotheses tested against defined business outcomes.

Recommended

- Insurance marketplace models 2026: 50% faster launches

- API-First Core Insurance Platforms Explained: 2025 Guide – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- API Strategy for Insurers: Driving Digital Impact

- Modern Insurance Platforms: What to look for – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance terminology explained: a practical guide for fleet owners