24.03.26

Understanding the insurance billing process for efficiency

Many insurance professionals mistakenly view billing as straightforward invoicing, when in reality it encompasses a sophisticated operational cycle that directly impacts cash flow, compliance, and customer retention. This guide unpacks the seven-step billing process specific to property and casualty insurance, revealing how each phase connects to operational efficiency. You will learn how automation transforms manual workflows, how to navigate midterm adjustments and regulatory complexities, and which key performance indicators reveal opportunities for improvement. Whether you are a billing specialist seeking process mastery or an executive evaluating system investments, understanding these operational nuances will help you reduce errors, accelerate payment cycles, and strengthen your organisation’s financial performance.

Table of Contents

- Key takeaways

- The insurance billing process explained: a seven-step operational cycle

- Automation versus manual workflows in insurance billing

- Handling billing complexities: midterm adjustments and regulatory requirements

- Measuring and improving billing efficiency with KPIs and benchmarks

- Discover how our platform can optimise your insurance billing

- What is the insurance billing process? FAQ

Key Takeaways

| Point | Details |

|---|---|

| Seven step cycle | The seven step cycle links policy issuance to compliance reporting, driving accurate cash flow and governance. |

| Handoff mapping | Map each billing step to system components and teams to identify handoff errors and support automated validation. |

| Automation benefits | Automation significantly reduces errors and accelerates payment cycles. |

| Midterm recalculations | Midterm policy adjustments require billing recalculations and add processing complexity. |

| Tracking KPIs | Tracking operational KPIs is essential to identify efficiency opportunities and improve performance. |

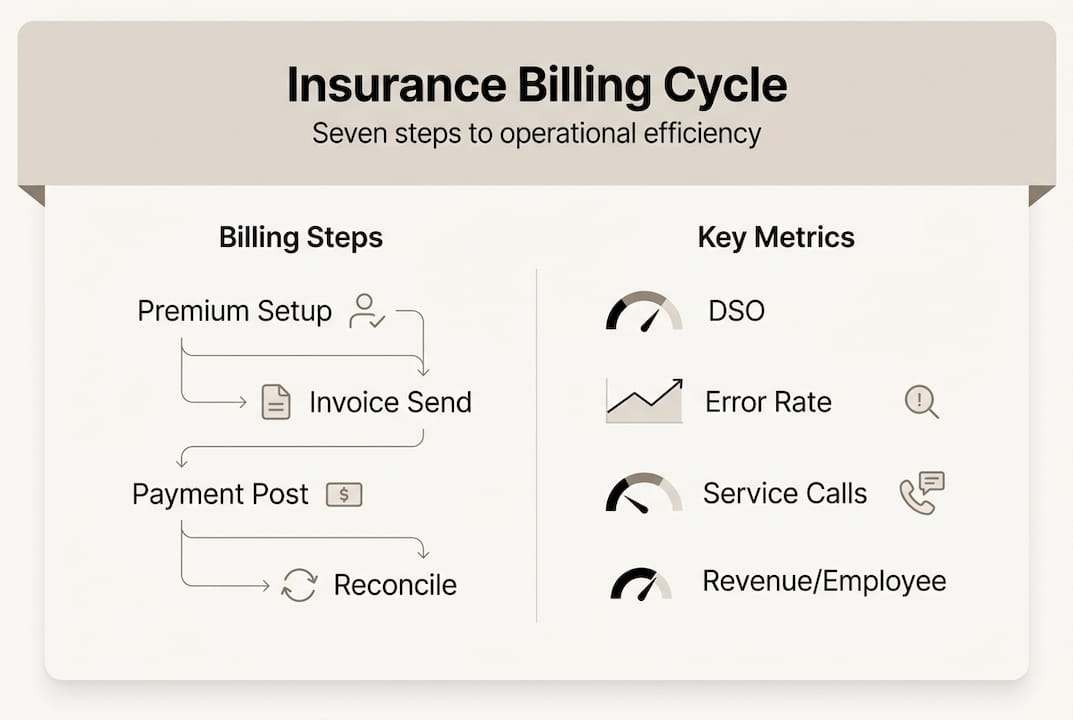

The insurance billing process explained: a seven-step operational cycle

The P&C insurance billing process operates as a continuous cycle of seven key operational steps starting with policy issuance and ending in compliance reporting. Each phase builds upon the previous one, creating dependencies that require precise coordination between systems and teams.

Step one begins with premium calculation, where underwriting data flows into rating engines that compute amounts based on coverage selections, risk assessments, applicable taxes, regulatory fees, earned discounts, and chosen payment plans. This calculation must account for jurisdiction-specific requirements and product-specific rating factors, making accuracy critical from the outset.

Step two generates invoices that reflect calculated premiums, payment terms, due dates, and accepted payment methods. Modern systems produce invoices dynamically, incorporating policy-specific details and customer preferences for format and delivery channels. These documents serve as both financial records and customer communications.

Step three delivers billing documents through channels including email, customer portals, and mobile applications. Multi-channel delivery ensures customers receive invoices through their preferred method whilst maintaining audit trails for compliance purposes. Delivery confirmation mechanisms track receipt and engagement.

Step four processes payment initiation and authorisation across multiple channels such as direct debit, credit cards, bank transfers, and agent-facilitated payments. Payment gateways validate transaction details, check account balances, and apply security protocols before authorising fund transfers. This phase includes fraud detection and payment plan verification.

Step five posts confirmed payments to customer accounts, updating policy status and triggering downstream processes. Posting accuracy determines whether policies remain active, lapse, or require collection actions. Systems must handle partial payments, overpayments, and payment reversals whilst maintaining precise account balances.

Step six reconciles billing records with payment receipts, identifying discrepancies between expected and received amounts. Reconciliation processes detect posting errors, payment mismatches, and system failures that could lead to revenue leakage or customer disputes. Daily reconciliation prevents accumulation of unresolved exceptions.

Step seven generates compliance reports for regulatory bodies, documenting premium collections, policy counts, and financial transactions according to jurisdiction-specific requirements. Regulatory reporting deadlines vary by territory, requiring systems to maintain multiple reporting templates and submission schedules.

Pro Tip: Map each billing step to specific system components and responsible teams to identify handoff points where errors commonly occur, then implement automated validation checks at these transition points.

Automation versus manual workflows in insurance billing

Practitioners favour automation for 70% error reduction and faster customer experiences, whilst executives highlight the need for process redesign and change management to realise full benefits. This distinction reveals that technology alone cannot transform billing operations without addressing underlying workflows and organisational readiness.

Automated billing systems eliminate manual data entry across invoice generation, payment processing, and account reconciliation. Humans typing premium amounts, due dates, and payment allocations introduce transcription errors that automated workflows prevent entirely. Systems validate data at each step, rejecting incomplete or inconsistent records before they propagate through downstream processes.

Customer payment experiences improve dramatically when automation enables real-time payment confirmation, instant policy updates, and immediate receipt delivery. Manual workflows require customers to wait hours or days for payment verification, during which coverage status remains uncertain. Automated systems confirm transactions within seconds, reducing anxiety and support enquiries.

Cash flow acceleration occurs because automated posting eliminates the delay between payment receipt and account crediting. Manual workflows batch payments for periodic processing, creating float periods where collected premiums sit unrecognised. Automated posting updates accounts immediately, improving working capital availability and financial reporting accuracy.

Lapse rate reduction follows from automated payment reminders, grace period tracking, and reinstatement workflows. Manual systems rely on staff to monitor approaching due dates and contact customers, a process prone to oversights. Automated systems send scheduled reminders, process late payments without intervention, and trigger appropriate actions based on payment status.

Executives must manage organisational change because automation shifts staff from transaction processing to exception handling and customer service. Employees accustomed to manual workflows may resist new systems or struggle to adapt to changed responsibilities. Successful implementations include training programmes, revised performance metrics, and clear communication about role evolution.

Process redesign becomes essential as automation exposes inefficiencies that manual workflows masked through workarounds and informal adjustments. Legacy processes often include unnecessary approval steps, redundant data entry, and manual reconciliation that automated systems eliminate. Organisations must rethink workflows from first principles rather than simply automating existing manual steps.

“Automation transforms billing from a labour-intensive transaction process into a strategic capability that enhances customer relationships and financial performance.”

- Automated validation rules prevent incorrect premium calculations from reaching customers

- Real-time payment processing reduces days sales outstanding by 30 to 40 percent

- Exception-based workflows allow staff to focus on complex cases requiring judgement

- Integrated systems eliminate data synchronisation delays between billing and policy administration

- Audit trails capture every system action, supporting compliance and dispute resolution

Handling billing complexities: midterm adjustments and regulatory requirements

Midterm endorsements and cancellations prompt automatic premium recalculations, whilst compliance requirements vary widely across jurisdictions, adding layers of operational complexity that systems must handle seamlessly. These exceptions test billing platform flexibility and staff expertise.

Midterm policy changes occur when customers modify coverage limits, add or remove vehicles, change addresses, or adjust deductibles during active policy periods. Each change triggers recalculation of earned versus unearned premium, requiring systems to prorate charges based on effective dates and apply appropriate short-rate penalties or return premium calculations. Endorsement billing must account for payment plan impacts, adjusting future instalments or generating supplemental invoices.

Cancellation scenarios introduce additional complexity through flat cancellation, short-rate cancellation, and pro-rata cancellation methods. Flat cancellation retains the entire premium regardless of coverage period consumed. Short-rate cancellation applies penalties for early termination initiated by policyholders. Pro-rata cancellation returns unearned premium proportionally when insurers cancel policies. Systems must apply the correct method based on cancellation reason and jurisdiction rules.

Multi-policy arrangements complicate payment allocation when customers hold several policies with different premium amounts, due dates, and payment plans. Single payments covering multiple policies require systems to split amounts correctly across accounts, applying payments according to priority rules that may vary by insurer. Payment shortfalls introduce allocation decisions that affect which policies remain active.

Jurisdiction-specific compliance obligations impose distinct requirements for premium taxes, regulatory fees, surplus lines taxes, and stamping fees. Each territory maintains unique rates, calculation methods, and remittance schedules. Billing systems must maintain current tax tables, apply correct rates based on risk location, and generate jurisdiction-specific reports for regulatory submissions.

Payment mismatches arise from partial payments, overpayments, payment reversals, and misapplied amounts. Detection requires comparing expected payment amounts against received amounts, investigating variances, and determining appropriate corrective actions. Unresolved mismatches accumulate as suspense items that distort financial reporting and create reconciliation backlogs.

Pro Tip: Monitor billing exceptions daily to avoid revenue leakage, focusing on endorsements awaiting premium calculation, payments in suspense, and policies approaching lapse without payment confirmation.

| Complexity type | Operational impact | System requirement |

|---|---|---|

| Midterm endorsements | Require premium recalculation and payment plan adjustment | Automated proration and instalment recalculation |

| Policy cancellations | Demand return premium calculation and refund processing | Configurable cancellation methods by jurisdiction |

| Multi-policy payments | Need intelligent allocation across accounts | Payment splitting rules and priority hierarchies |

| Regulatory compliance | Impose jurisdiction-specific tax and fee calculations | Maintained tax tables and reporting templates |

- Endorsement processing time directly impacts customer satisfaction and operational costs

- Policy administration systems must trigger billing recalculations automatically upon coverage changes

- Payment suspense accounts require daily review to prevent aged items and audit findings

- Compliance calendars track reporting deadlines across all operating jurisdictions

Measuring and improving billing efficiency with KPIs and benchmarks

Operational KPIs include days sales outstanding, error rates, and service calls, whilst revenue per employee benchmarks range from £145,000 to £290,000 depending on organisation size and automation maturity. These metrics provide objective measures of billing performance and reveal improvement opportunities.

Days sales outstanding measures the average time between invoice generation and payment receipt. Lower DSO indicates faster cash conversion and better working capital management. Industry benchmarks suggest DSO below 30 days represents strong performance, whilst DSO exceeding 45 days signals collection issues or payment plan problems. Tracking DSO by payment method, customer segment, and policy type identifies specific bottlenecks.

Error rates quantify billing mistakes including incorrect premium calculations, misapplied payments, duplicate invoices, and posting errors. Error rates below 2% represent acceptable performance for manual workflows, whilst automated systems should achieve error rates below 0.5%. High error rates trigger customer complaints, require correction work, and damage insurer reputation.

Customer service calls related to billing questions indicate process clarity and communication effectiveness. Frequent enquiries about payment due dates, amount calculations, or account balances suggest confusing invoices or inadequate self-service tools. Monitoring call volume by topic reveals which billing aspects cause customer confusion.

Revenue per employee benchmarks measure organisational efficiency by dividing total revenue by staff count. Smaller organisations typically generate £145,000 to £180,000 per employee, whilst larger organisations with greater automation achieve £220,000 to £290,000 per employee. Significant deviations from peer benchmarks indicate potential efficiency gaps or operational excellence.

Payment plan adoption rates show the percentage of customers choosing instalment payments versus paying annually. Higher adoption rates provide steadier cash flow but increase processing costs and lapse risk. Optimal adoption rates balance customer preference with operational efficiency, typically ranging from 60% to 75% depending on market segment.

| Organisation size | Revenue per employee | Days sales outstanding | Error rate | Service calls per 1,000 policies |

|---|---|---|---|---|

| Small (under 50 staff) | £145,000 to £180,000 | 35 to 45 days | 1.5% to 3.0% | 45 to 60 |

| Medium (50 to 200 staff) | £180,000 to £220,000 | 30 to 40 days | 1.0% to 2.0% | 30 to 45 |

| Large (over 200 staff) | £220,000 to £290,000 | 25 to 35 days | 0.5% to 1.5% | 20 to 35 |

- Establish baseline metrics before implementing process changes to measure improvement accurately

- Segment KPIs by product line, distribution channel, and customer type to identify specific issues

- Review billing optimisation opportunities quarterly based on KPI trends

- Benchmark against peer organisations to set realistic improvement targets

- Link operational KPIs to staff incentives to drive continuous improvement

Managers should establish regular KPI review cadences, examining metrics weekly for operational monitoring and monthly for trend analysis. Significant deviations from targets trigger root cause investigations and corrective action plans. Sharing KPI dashboards with billing teams creates transparency and accountability whilst highlighting improvement successes.

Discover how our platform can optimise your insurance billing

Our IBSuite platform delivers comprehensive billing automation designed specifically for property and casualty insurers seeking operational excellence. The system handles the complete billing lifecycle from premium calculation through compliance reporting, eliminating manual workflows that introduce errors and delays. Real-time payment processing and automated reconciliation reduce days sales outstanding whilst improving cash flow predictability. Built-in compliance frameworks maintain current regulatory requirements across multiple jurisdictions, automatically applying correct tax rates and generating required reports. Integrated KPI dashboards provide visibility into billing performance, highlighting exceptions and trends that require management attention. The platform connects seamlessly with policy administration, claims, and financial systems, ensuring data consistency across your entire operation. Booking a personalised demo allows you to explore how our billing automation capabilities address your specific operational challenges whilst our team shares proven optimisation strategies that reduce costs and enhance customer satisfaction.

What is the insurance billing process? FAQ

How does insurance billing differ from claims processing?

Billing manages premium collection and payment processing for active policies, whilst claims processing handles loss payments to policyholders after covered events occur. Billing operates continuously throughout policy terms, whereas claims processing activates only when losses are reported. The two functions use separate systems but must share policy data to verify coverage at claim time.

Why are midterm billing changes necessary?

Midterm changes reflect policy modifications that alter risk exposure and premium requirements during active coverage periods. When customers add vehicles, increase limits, or change addresses, insurers must recalculate premiums to match current risk levels. Failing to adjust billing for coverage changes creates premium shortfalls or overcharges that affect profitability and customer satisfaction.

What are typical timelines for payment posting?

Automated systems post electronic payments within minutes of receipt, updating policy status and account balances in real time. Manual workflows batch payments for daily or weekly processing, creating delays of one to five business days between receipt and posting. Cheque payments require additional time for bank clearance before posting occurs, typically adding two to three business days.

How does automation impact customer billing experience?

Automation provides instant payment confirmation, immediate policy updates, and real-time access to billing history through customer portals. Customers receive automated reminders before due dates, reducing missed payments and policy lapses. Self-service payment options eliminate phone calls and waiting for business hours, whilst automated receipt delivery provides immediate transaction documentation.

Which billing KPIs should operations managers monitor regularly?

Managers should track days sales outstanding to measure collection speed, error rates to assess accuracy, and customer service calls to gauge process clarity. Revenue per employee reveals overall efficiency, whilst payment plan adoption rates indicate customer preferences and processing volumes. Exception counts for suspended payments, failed transactions, and unresolved discrepancies highlight operational issues requiring immediate attention.

Recommended

- What is insurance billing in P&C? A clear 2026 guide

- What is insurance billing automation? P&C benefits 2026

- Insurance Billing Processes Explained: Complete Guide – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance Billing Processes – Impact on P&C Insurers

- Insurance Claims — Claims Management | Seaventis — AI-Powere