Reflecting on innovation across sectors, McKinsey states the following analogy[i]:

“The question is not how fast tech companies will become car companies, but how fast we will become a tech company.” This is how the board member of a global car company recently articulated the central issue facing most incumbents today: how to operate and innovate like a tech company… IT is not a cumbersome estate “that gets in the way,” but an enabler and driver of continuous innovation and adaptation… These platforms are each managed individually, can be swapped in and out, and, when “assembled,” form the backbone of a company’s technology capability… This modular, platform-based IT setup of tech companies is what enables them to accelerate and innovate. They can experiment, fail, learn, and scale quickly: they can get products to market 100 times faster than their more lumbering peers (think weeks instead of months).

Sibylle Fischer, Director Strategic Venturing / Startup Scouting at Baloise Group, adds[ii]:

‘Today, cloud-based software and software platforms, open-API technologies, microservices, machine learning and A.I. are all helping to redefine everything we know about insurance — from the way we onboard customers, to how we process claims, to how we sell products and services. But to succeed and make the most out of the ever-evolving opportunities new technologies offer, insurers need to take decisive action. That means:

1. Moving fast and pursuing aggressive strategies that roll out digital acceleration in core tech that touch on virtually all aspects of their business;

2. Forgoing their traditional, on-premise systems for next-gen cloud-native platforms that will help future-proof many of their most essential business functions, and;

3. Looking across their business units (beyond IT) at where and how they can adopt next-gen core platform solutions to accommodate the kinds of open, real-time, personalized multi- and cross-channel experiences today’s customers demand.

The companies that can succeed at doing so will be in the best position to scale, compete, and introduce new revenue streams and business models into their ecosystem – now and in the future.’

Five to six years ago, when CIS modernization was being talked about for half a decade already, a study by Deloitte and LIMRA[iii] showed that the top 3 influential factors of core system transformation were – and probably continue to be:

1. Product strategy and objectives or being able to launch new products and/or alter existing ones easily and fast and make them available via the right distribution channel;

2. Technological relevance. Built on ageing languages, databases, architectures, and legacy systems lack flexibility and carry significant technological debt;

3. Service enablement and the capability of digitizing services to deliver an improved customer experience.

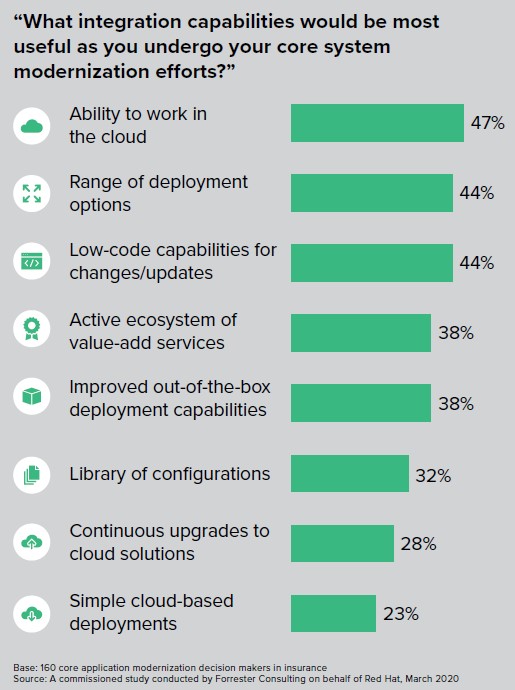

In 2020, when Forrester[iv] questioned insurers on what they thought were the most useful integrations capabilities – a basic aspect of any system – as they underwent core system modernization efforts, the responses emphasized facilitators related to:

- Deployment: simple, out of the box and range of options

- Maintenance: the cloud, low-code capabilities, continuous updates

- Ecosystems

- Library of configurations

The advantages of SaaS

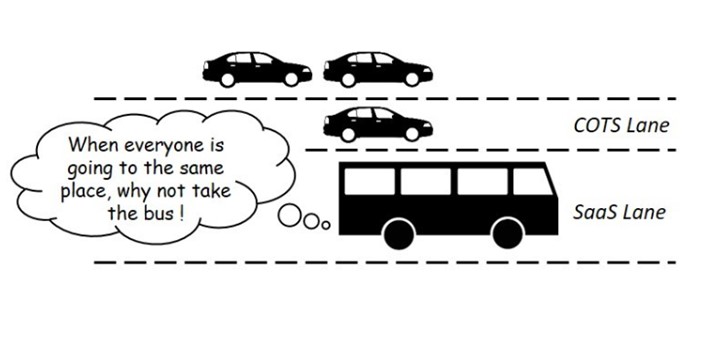

While insurers easily consider it for peripherical functions, some are still sceptical about considering SaaS products when the subject is core modernization. Differentiating themselves in the market by the uniqueness built into their core, the fear of losing this difference by adopting a standard software makes them hesitant.

Not looking at SaaS, and with building their core on-prem out of budget, insurers turn to Commercial Off The Shelf (COTS) solutions. While cheaper and fast implemented than modern homebuilt systems, due to the standardization of many of the core insurance processes, COTS core systems tend to be very similar between vendors. Extra coding is then necessary, which seriously impacts initial investment, and timeline while cluttering the code base.

The advantages of SaaS when compared to other types of core system solutions are:

- Standard modules,

- APIs library to easily connect, including to low-code differentiation layers such as digital interfaces (e.g., mobile apps, bots, voice apps, etc.);

- Quicker and cheaper onboarding

In addition to standard processes and products that may be made unique through differentiation layers, choosing the right SaaS partner saves costs, improves service capabilities, and helps you meet your customers’ expectations.

Cloud as an enabler

“Products that are built with true cloud-first approach will usher in the next disruption in insurance core systems space … Big opportunities and next wave of transformations await products that are built on foundations of cloud and SaaS best practices and principles.” [v]

McKinsey figures [vi] that cloud adoption enables carriers to standardize, automate and benefit from:

- 30 to 40% reduction of IT overhead costs;

- Optimized IT asset usage by scaling processes up and down as needed;

- Improved overall flexibility of IT in meeting business needs through the use of business features made available by cloud providers;

- Increased quality of service through the “self-healing” nature of the standard solutions (i.e.: automatically allocating more storage to a database).

Overall, Cloud-native technology accelerates innovation, simplifies operations, works seamlessly with other systems and helps deliver personalized products and better customer experiences.

Sources:

[i] In: McKinsey & Cy, Reaching the next normal of insurance core technology, June 2020, p.73

[ii] In: What’s Next for Innovation in Core Insurance

[iii] In: Legacy systems and modernization, Deloitte & LIMRA, 2017, p.3

[iv] In: Core System Modernization: Time For A New Roadmap, Forrester commissioned by Red Hat, May 2020, p.7

[v] SaaS core systems will enable Insurers to differentiate; Post by Sankar M, Associate Director at Cognizant; February 16, 2020

[vi] In: McKinsey & Cy, Reaching the next normal of insurance core technology, June 2020, p.40