15.02.24

Automation and Artificial Intelligence in P&C Insurance

Insurance is commonly thought to be slow and bureaucratic. Although the industry is transforming and this is changing, historically, all processes of the insurance value chain incorporated human intervention to a certain degree. While judgement and advice are necessary for some contexts, in many others human intervention limits itself to basic data input systems or to transcription from one system to another. besides being slow, these labour-intensive tasks have other inconveniences. They are prone to errors, expensive and probably not the most rewarding.

Insurers, who started off their digital transformation journey by providing consumers with a more digital experience, are now looking to automate to reduce costs, improve efficiency, better use resources, and increase the scalability of their operation.

Automation may be applied to a great variety of processes. It comprises Robotic Process Automation (RPA) and artificial intelligence (AI) solutions such as Intelligent Document Processing (IDP), chatbots, and machine learning, that augment each other to mimic a user’s activities and/or human thought process to completely -or partially – manage business processes[1].

Looking at underwriting for instance, Deloitte found out in their Financial Services Global Outlook Survey 2020, that an increase in automation was the top alteration insurers planned to make in a 6 to 18 months time frame[2]. By doing so, carriers, burdened by legacy systems and unproductive tasks, such as manually compiling information from disparate sources and interfacing with multiple systems, hope to lower costs and increase productivity.

Insurance broker submissions, for example, are an area where handling is still high. Email submissions are read by knowledge workers who triage them and extract relevant information for downstream underwriting. The same applies to any attachments, forms, loss-run reports, spreadsheets, custom forms, and photos. However, this process is labour-intensive, time-consuming, and error-prone, and can hinder the time to bind. As a result, quotes are not turned around quickly enough for customers and not all are processed, at the risk of not quoting more complex submissions that may represent acceptable opportunities. The company thus ends up at a disadvantage compared to more agile competitors.

A submission intake solution that integrates intelligent technology may resolve these problems. It automates submission intake and triage processes and performs data capture and input tasks faster and more accurately than employees can on their own.

Claims is another area where automation and AI is being applied. Doing so carriers look to provide customers with a quicker and improved experience while making the process more efficient and saving claims expenses.

Underwriting and claims are just 2 activities part of the Insurance value chain. Other activities exist which also may be broken down into multiple processes, some of which are more prone to automation.

Although all processes may seem capable of automation in theory, not all have the same potential to be automated or offer the same benefits. So, how to know which processes are worthwhile and with which ones to start?

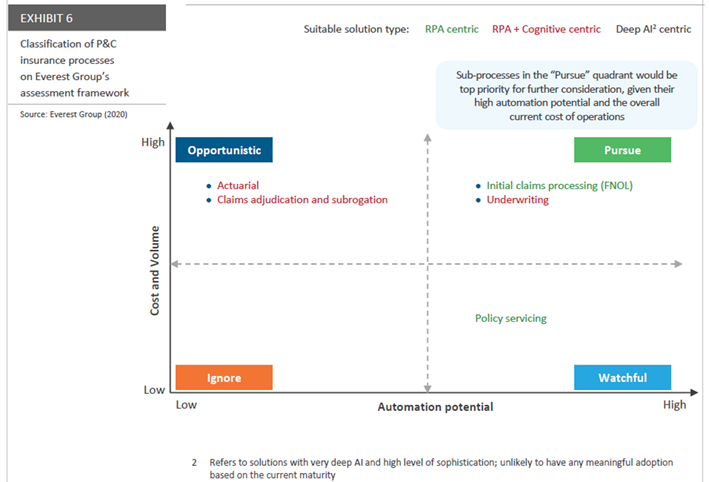

The Enterprise Value Chain Approach1 (EVCA) is a framework that enables organizations to identify and assess processes for automation to create and feed automation pipelines. It is a methodological approach that analyses activities and breaks them down into their constituent processes or value chain. Each constituent part is assessed for its suitability for automation based on a set of assessment dimensions, such as whether it is transactional or strategic, its cost and volumes. At the end of the assessment, the processes deemed unsuitable for automation are removed from the automation program, and the remaining processes are put on the list for further consideration.

Applying the EVCA, Everest Group identified five primary business processes that are integral to the P&C insurance value chain. The first step involves evaluating the financial risk of insuring an entity, which is conducted by actuaries. Actuaries use historical data to create rate tables that estimate the likelihood of an event occurring and provide the appropriate premium based on various factors and features. Next, the underwriter determines if the applicant should be insured and uses the rate table to determine the appropriate premium. After the analysis of the risk to be covered under the insurance policy, the process moves on to policy servicing and reporting. This step encompasses transactional duties, such as processing and printing the policy, preparing insurance endorsements, auditing, and resolving customer queries. The last stage is claims processing, which is a five-step process starting with the initial notice of loss, followed by claims appraisal and adjustment, settlement of claims, and salvage through subrogation and litigation.

Once the 5 process groups are identified, each constituent sub-process is further scrutinized for its automation potential as described above, to make up the graph below recommending further action based on Everest Group’s assessment framework.

The Pursue quadrant of the framework is occupied by processes with high automation potential and high overall cost and volume of operations. The first notice of loss (FNOL) process and underwriting process are both in this quadrant due to their high transactional volume and potential for automation. FNOL involves minimal judgement and has multiple technology platform deployments, making it highly automatable. Underwriting also has a high automation potential due to a fragmented technology environment and significant underwriting activity and could benefit from cognitive data processing. Automating these processes could improve efficiency, reduce cycle time, enhance fraud detection, and minimize errors.

The Claims adjudication, subrogation, and actuarial processes offer a cost-saving opportunity through automation but have limited potential, placing them in the Opportunistic quadrant of the framework. These processes are complex and require human intervention, with actuarial modelling and analysis making it difficult to digitalize. However, cognitive data processing and self-learning algorithms can improve automation adoption and enhance business performance. Claims adjudication and subrogation have lower automation potential due to unstructured process workflows and minimal standardization. The leverage of cognitive solutions can reduce manual processing requirements and drive a healthy bottom line for insurers.

Policy servicing has moderate automation potential but is in the Watch quadrant due to the already fairly digitalized and transactional nature of the process. Chatbots are in use to enhance digital customer experience, which limits further efficiencies with first-level process optimization already achieved. However, techniques such as straight-through processing and auto-flagging of cases addressed can improve cost optimization and reduce turnaround time.

It is thus fair to say that the P&C insurance value chain processes have a reasonable potential for automation due to their transactional nature and well-defined workflows. However, most of these processes are highly complex, requiring extra efforts to achieve superior benefits from automation deployment. If implemented correctly, automation can improve carriers’ bottom lines and increase market share by engaging customers in newer and better ways.

[1] Identifying Automation Opportunities for Property and Casualty Insurers, From <https://www.automationanywhere.com/company/blog/rpa-thought-leadership/identifying-automation-opportunities-for-property-and-casualty-insurers>

[2] The rise of the exponential underwriter, Leveraging a convergence of data, technology, and human capital to transform underwriting in insurance, From <https://www2.deloitte.com/us/en/insights/industry/financial-services/future-of-insurance-underwriting.html/#endnote-sup-7>