13.07.26

Microservices in insurance: a practical guide for 2026

Microservices in insurance are modular, independently deployable software components that replace monolithic core systems with fine-grained services, each handling a single business function. European insurers are already proving the model works at scale. Generali GC&C increased underwriting efficiency by 80% and cut licensing costs by 60% after moving to a cloud-native microservices platform. Helvetia Italy Group reduced time-to-market by 30% for new products using a microservices-based Digital Integration Hub. These are not incremental gains. They signal a fundamental shift in how insurance IT is built, governed, and scaled.

How does microservices architecture work in insurance systems?

Microservices architecture decomposes a core insurance platform into small, independent services. Each service owns a single business capability, such as rating, policy issuance, claims intake, or billing. Services communicate via APIs and can be deployed, updated, or replaced without touching the rest of the system.

Monolith vs microservices: the core difference

Traditional insurance platforms bundle every function into one tightly coupled codebase. A change to the rating engine requires retesting the entire system. A failure in billing can bring down policy administration. Microservices remove that dependency by giving each function its own runtime, data store, and release cycle.

Domain-driven design is the standard method for defining service boundaries in insurance. Each service maps to a bounded context, for example, underwriting, claims, or customer management. This prevents services from growing into mini-monoliths over time.

| Characteristic | Monolithic system | Microservices architecture |

|---|---|---|

| Deployment | Full system release | Independent per service |

| Failure impact | System-wide | Isolated to one service |

| Scaling | Scale everything | Scale individual services |

| Technology choice | Single stack | Per-service flexibility |

| Change velocity | Slow, high-risk | Fast, low-risk |

An API-first approach in insurance is what makes this modularity practical. APIs define the contract between services and between the platform and external partners, such as brokers, aggregators, and regulators. Cloud-native deployment on platforms like AWS, using containers and orchestration tools, provides the infrastructure for running dozens of services reliably at scale.

Pro Tip: Start by mapping your existing system to bounded contexts before writing a single line of new code. Insurers who skip this step often replicate their monolith’s problems in a distributed form.

What are the benefits of microservices for insurance operations and innovation?

The benefits of microservices for insurance extend well beyond IT. They reshape underwriting speed, product agility, cost structure, and customer experience simultaneously.

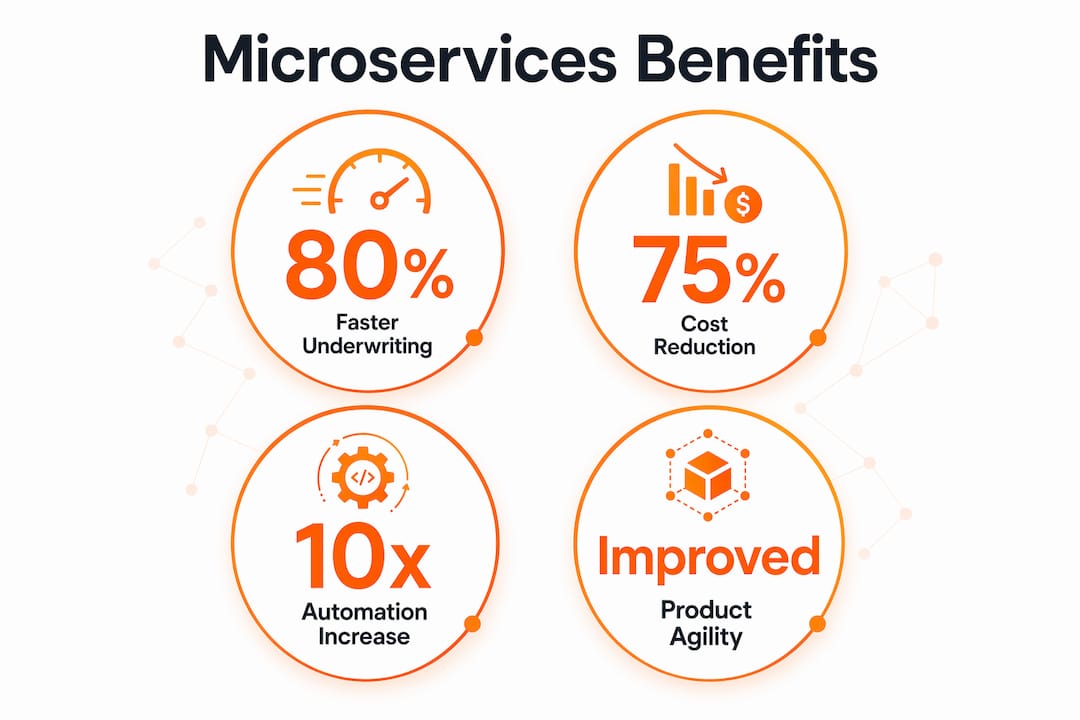

Generali GC&C’s results illustrate the operational upside clearly. The insurer cut support costs by 75% alongside the 80% underwriting efficiency gain. Those figures reflect what happens when teams stop maintaining a fragile monolith and start deploying focused services that do one thing well.

UNIQA demonstrates the automation potential. The insurer automated policy updates so that 10 of 19 customer request types now complete without manual intervention, with processing time under two minutes. That means customers receive policy changes faster than most insurers can even locate the relevant record in a legacy system.

Insurers adopting composable, modular architectures are projected to implement new features 80% faster than competitors still running legacy monoliths. That speed advantage compounds over time, as each new product or regulatory change requires less effort to ship.

The key benefits for insurance professionals and IT leaders include:

- Underwriting speed: Modular rating and rules engines update independently, cutting turnaround times significantly.

- Cost reduction: Targeted scaling and independent licensing reduce infrastructure and support spend, as Generali’s 60% licensing cost cut demonstrates.

- Faster product launches: Helvetia Italy Group’s 18% reduction in project costs came alongside a 30% faster time-to-market, showing that speed and cost savings are not a trade-off.

- Automation at scale: Microservices provide the foundation for automating repetitive tasks across policy administration, claims, and billing.

- AI readiness: Discrete services expose clean data and logic boundaries, making it far simpler to attach machine learning models or AI decisioning layers.

- Regulatory compliance: Services can be updated independently to meet DORA or GDPR requirements without a full platform release.

- Partner integration: API-driven services connect directly to broker portals, aggregators, and third-party data providers without custom middleware.

Pro Tip: Prioritise the services that directly differentiate your business, such as pricing and underwriting rules, for early microservices investment. Commodity functions like document generation are better integrated via APIs than rebuilt from scratch.

How to design and implement microservices architecture in insurance

Good microservices design in insurance starts with a clear distinction between two types of capability. Differentiating capabilities are the functions where your business competes: pricing logic, underwriting appetite, claims triage rules. Standard utility functions are the commodity work every insurer does: document storage, payment processing, identity verification. Proper microservices design separates these two categories and treats them differently.

Differentiating capabilities deserve purpose-built microservices with full ownership by your product teams. Standard utility functions are better integrated via APIs from specialist providers. Building commodity functions from scratch is expensive and adds maintenance burden without competitive return.

A practical implementation follows these steps:

- Map your domain. Use domain-driven design to identify bounded contexts across your insurance value chain. Underwriting, policy administration, claims, billing, and CRM each represent a natural service boundary.

- Prioritise the migration sequence. Begin with services that cause the most pain in your current system, or those that block new product launches. Do not attempt a full rewrite in one programme.

- Choose your modernisation path. A hybrid Greenfield and Brownfield approach is the most effective strategy for most European insurers in 2026. Greenfield builds new capabilities on microservices from day one. Brownfield wraps or replaces legacy components incrementally.

- Establish a central integration layer. This layer maintains stable behaviour for partners, customers, and regulators while the underlying services migrate. It acts as a buffer between the old and new worlds.

- Define your migration playbook. Live migration must be treated as a business-critical operation, not a technical exercise. The playbook should specify behavioural contracts, rollback procedures, and acceptance criteria for each service.

- Engage stakeholders early. Compliance, operations, and distribution teams all have dependencies on the systems you are changing. Governance checkpoints prevent costly surprises.

The benefits of a multi-core strategy for insurers align directly with this approach. Splitting a legacy monolith into focused cores, one for personal lines, one for commercial, one for claims, mirrors the bounded context principle and makes the transition manageable.

Pro Tip: Treat your migration playbook as a living document. The insurers who succeed with live migration update their playbook after every service cutover, capturing what changed and what the next team needs to know.

What are the common challenges of adopting microservices in insurance?

Microservices introduce distributed system complexity that monoliths do not have. Debugging a failure across 30 independent services is harder than tracing an error in a single codebase. Observability is the answer, but most insurance IT teams underinvest in it at the start.

Observability focused on business behaviour, such as quote completion rates, rating outcomes, and claims cycle times, is more valuable than infrastructure metrics alone. If a service degrades, you need to know whether it is affecting customer outcomes before your partners or regulators notice.

The main challenges insurance IT leaders face when adopting microservices architecture include:

- Distributed complexity: More services mean more failure points, network calls, and configuration to manage. Container orchestration and service mesh tools address this, but require investment in platform engineering skills.

- Commodity over-build: Teams sometimes build custom microservices for functions that already exist as mature API products. This wastes budget and creates long-term maintenance debt.

- Regulatory compliance during migration: DORA and GDPR require documented controls and audit trails. Compliance through next-generation platforms must be designed in from the start, not retrofitted.

- Interoperability during cutover: Partners and brokers expect stable API behaviour. A migration boundary must not become a compliance boundary. Stable contracts must hold throughout.

- AI integration readiness: Microservices enable AI, but only if data flows are clean and service boundaries are well defined. Poorly scoped services create data silos that block AI use cases.

Pro Tip: Invest in observability tooling before your first service goes live in production. Teams that add monitoring retrospectively spend far more time firefighting than those who instrument from day one.

Key takeaways

Microservices architecture in insurance delivers measurable gains in speed, cost, and agility when implemented with clear service boundaries, a structured migration playbook, and observability built in from the start.

| Point | Details |

|---|---|

| Proven efficiency gains | European insurers like Generali GC&C report 80% underwriting speed increases and 75% support cost reductions. |

| Faster product launches | Helvetia Italy Group cut time-to-market by 30% and project costs by 18% using a microservices integration hub. |

| Design before you build | Domain-driven design and bounded contexts prevent microservices from replicating monolith problems in a distributed form. |

| Hybrid modernisation works | Combining Greenfield and Brownfield approaches lets insurers move fast on new capabilities while stabilising legacy systems. |

| Observability is non-negotiable | Monitoring business outcomes, not just infrastructure, prevents regressions during live migration in regulated environments. |

Why microservices are a business decision, not just an IT one

I have seen insurance IT programmes framed entirely as technology upgrades, and that framing is where they go wrong. Microservices architecture changes how quickly your business can respond to a regulatory shift, how fast your pricing team can test a new product, and how much your operations team spends on manual processing. Those are business outcomes, not infrastructure metrics.

The hybrid Greenfield and Brownfield approach has become the dominant path for European insurers, and rightly so. A full rewrite is a multi-year gamble. Incremental modernisation, with a proper migration playbook and stable API contracts, lets you deliver value every quarter while reducing risk. The insurers I find most credible on this topic are the ones who treat live migration as a first-class operation, not an afterthought.

The AI angle is also worth taking seriously now, not later. Clean service boundaries and well-defined APIs are the prerequisite for attaching AI models to underwriting, claims triage, and fraud detection. Insurers who build that foundation today will integrate AI far faster than those who bolt it onto a monolith. The role of automation and AI in P&C insurance is only going to grow, and microservices are what make that integration practical.

The governance question is the one most IT leaders underestimate. Microservices give teams autonomy, and autonomy without governance produces inconsistent APIs, duplicated services, and compliance gaps. The organisations that get this right establish clear ownership, standardised service templates, and regular architecture reviews from the beginning.

— Tuna

How Ibapplications supports insurers moving to microservices

Ibapplications builds IBSuite as an API-first, cloud-native platform on AWS, designed specifically for property and casualty insurers who need modular architecture without the complexity of building it from scratch. The policy administration platform delivers a fully modular service layer covering underwriting, rating, billing, and CRM, each independently configurable to match your product and market requirements. The claims management platform brings the same modularity to claims intake, triage, and settlement, with built-in automation and integration points for third-party data providers. Both platforms include Evergreen updates and compliance support for DORA and GDPR, so your architecture stays current without manual intervention.

FAQ

What is microservices architecture in insurance?

Microservices architecture in insurance is a design approach that breaks a core insurance platform into small, independent services, each handling one business function such as rating, policy issuance, or claims. Services communicate via APIs and deploy independently, removing the tight coupling of traditional monolithic systems.

What are the main benefits of microservices for insurers?

The main benefits include faster product launches, lower support and licensing costs, improved automation, and AI readiness. Generali GC&C achieved an 80% increase in underwriting efficiency and a 75% reduction in support costs after adopting a cloud-native microservices platform.

How do insurers manage the risks of live migration to microservices?

Live migration requires a structured playbook that defines stable behavioural contracts with partners, customers, and regulators throughout the transition. Observability of business outcomes, such as quote completion and claims cycle times, is critical to detecting regressions before they cause compliance or service failures.

What is the difference between Greenfield and Brownfield microservices modernisation?

Greenfield builds new insurance capabilities on microservices from the start, while Brownfield wraps or replaces existing legacy components incrementally. A hybrid approach combining both is the most effective path for European insurers balancing innovation speed with legacy stability in 2026.

How do microservices support regulatory compliance in insurance?

Microservices allow individual services to be updated independently to meet requirements such as DORA and GDPR, without triggering a full platform release. Compliance controls and audit trails can be built into each service boundary, making regulatory updates faster and less disruptive than in monolithic systems.

Recommended

- Insurance marketplace models 2026: 50% faster launches

- Modern Insurance Platforms: What to look for – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Why choose flexible insurance systems in 2026

- API-First Core Insurance Platforms Explained: 2025 Guide – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System