06.07.26

Insurance distribution models 2025: the executive guide

Insurance distribution models in 2025 are defined by the convergence of direct digital channels and human advisory support into hybrid structures that serve digitally active yet advice-seeking customers. Independent channels now control the majority of new life insurance premiums, AI is replacing intuition in channel analytics, and European regulatory frameworks are rewiring how distributors are compensated. For insurance executives, the question is no longer whether to modernise distribution. It is how to do it in a way that improves profitability, customer engagement, and long-term retention simultaneously.

What are the predominant insurance distribution models in 2025?

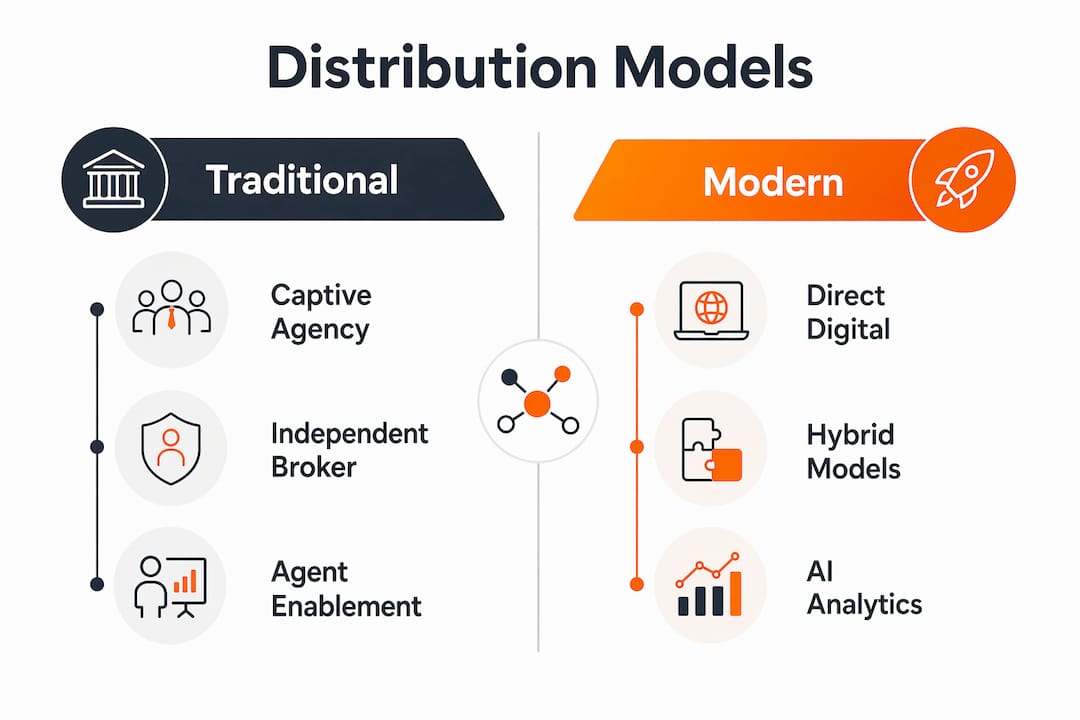

The four principal distribution models operating in the market today are captive agency, independent broker, direct-to-consumer digital, and hybrid. Each carries distinct economics, customer reach, and operational demands.

Captive agency models tie agents exclusively to one carrier. They offer brand consistency and deep product knowledge, but limit customer choice and create high fixed costs. As consumer expectations shift toward comparison and flexibility, captive models are losing ground.

Independent broker and managing general agent channels now dominate premium volume. Independent channels hold 60% of all new life insurance annual premium and close to 50% of annuity production. That structural shift places significant pricing and product power outside the carrier’s direct control, which demands a more deliberate approach to partner management.

Direct-to-consumer digital channels offer low acquisition costs and 24/7 availability, but they hit a ceiling with complex products. Customers will complete a motor or travel policy online without assistance. They will not do the same for income protection or whole-of-life cover without guidance.

Hybrid models combine a digital front end for research and initial engagement with access to a licensed adviser at the point of decision. This architecture matches how customers actually behave, and it is becoming the default design for carriers serious about digital distribution in insurance.

How the models compare on key dimensions

| Dimension | Captive agency | Independent broker | Direct digital | Hybrid |

|---|---|---|---|---|

| Customer reach | Moderate | High | High | High |

| Product complexity handled | High | High | Low | Medium to high |

| Acquisition cost | High | Variable | Low | Medium |

| Carrier control | High | Low | High | Medium |

| Regulatory alignment | Moderate | Variable | High | High |

How is customer behaviour influencing insurance distribution in 2025?

Consumer research habits have fundamentally changed what distribution must deliver. 92% of customers research life insurance online, yet 75% want human guidance at the moment of purchase. That gap between research behaviour and purchase behaviour is the single most important design constraint for any distribution strategy.

Carriers that ignore this gap build either a fully digital channel that converts poorly on complex products, or a fully agent-led channel that loses customers who started their research online and found a competitor first. Neither extreme works.

Technology is beginning to fill part of that gap. Only 11% of insurance shoppers currently use virtual assistants or chatbots during their journey, but those who do report satisfaction scores 132 points higher than non-users. That is a significant uplift from a tool that remains dramatically underdeployed. The implication is clear: carriers that invest in well-designed digital assistance can improve customer engagement without replacing the human adviser.

Pro Tip: Map your customer journey by product line, not by channel. A customer buying motor insurance has a different decision path than one buying life cover. Designing one hybrid model for both will underserve both.

The practical lesson is that distribution design must follow customer intent, not internal organisational convenience. Customers want self-service for research and speed, and human expertise for trust and complexity. Building that combination is the core challenge of customer engagement in insurance for 2025 and beyond.

What role does AI play in optimising insurance distribution models?

AI transforms distribution from an intuition-driven activity into a data-driven discipline. Carriers that treat distribution as a granular profitability challenge outperform those managing channels by instinct alone. The difference is measurable at the channel level, the agent level, and the product level.

Channel-level analytics

AI measures profitability, loss ratios, and retention rates per channel with a granularity that manual reporting cannot match. A carrier might discover that a particular broker segment generates high premium volume but poor loss ratios, or that a digital channel acquires customers who lapse within 18 months. Without AI-driven analytics, those patterns stay hidden inside aggregated reports.

Embedding insurance within retail or technology platforms is one of the fastest-growing distribution experiments in Europe. AI makes those partnerships evaluable. It tracks volume, profitability, and risk profile from embedded channels so executives can decide which partnerships to scale and which to exit.

Agent enablement

AI augments human agents by providing real-time, predictive insights that help them act as empathetic advisers rather than transactional clerks. An agent who knows, before a renewal call, that a customer is at high risk of lapsing can have a very different conversation than one working from a standard renewal script. That shift in the quality of the advisory interaction directly improves retention.

Pro Tip: Prioritise AI tools that surface insights within the agent’s existing workflow. If agents must switch between systems to access predictive data, adoption rates will be low regardless of the tool’s quality.

Digital-first brokers are already combining API data connections with regulatory and risk data sources to automate risk profiling, compressing underwriting timelines significantly. That capability is moving from specialist brokers into mainstream distribution as platform infrastructure matures.

How are regulatory trends shaping insurance distribution in 2025?

European regulatory frameworks are shifting from volume-based oversight to customer-centric accountability. The direction of travel mirrors reforms seen in markets like India, where regulatory frameworks now link distributor incentives to persistency and product complexity rather than raw sales volume. European regulators are applying similar logic through conduct-of-business rules and product governance requirements.

The practical effect is a shift from volume-based compensation to value-based incentive structures. Agents and brokers who sell policies that lapse quickly will earn less. Those who build durable books of business will earn more. That alignment between distributor behaviour and policyholder outcomes is the intended result.

Shifting to value-based incentives linked to customer lifetime value and retention is not just a regulatory response. It is also the correct commercial decision for carriers using AI-driven retention strategies, because it aligns agent motivation with the metrics that AI is optimising.

The talent dimension compounds the regulatory challenge. The distribution talent pipeline faces a succession crisis as experienced advisers retire and younger recruits expect different working conditions, digital tools, and career structures. Carriers that do not overhaul recruitment, onboarding, and development now will face a capability gap precisely when hybrid distribution demands the most from their adviser workforce.

Key regulatory priorities for executives to track:

- Persistency-linked compensation structures replacing flat commission models

- Product governance requirements demanding evidence of customer suitability

- Conduct-of-business rules increasing documentation and audit obligations

- Succession planning requirements for regulated adviser networks

What practical steps can executives take to optimise distribution strategies?

Optimising distribution is a sequenced process, not a single technology decision. The following steps reflect what carriers with mature distribution analytics actually do.

- Establish granular channel metrics. Measure acquisition cost, loss ratio, and customer lifetime value per channel and per product line. Aggregate data conceals the channels that are destroying margin.

- Design hybrid experiences by product complexity. Simple products can be fully digital. Complex products need a digital research phase followed by an adviser handoff. Build the handoff point into the customer journey deliberately, not as an afterthought.

- Integrate AI into agent workflows. Deploy predictive tools that surface renewal risk, cross-sell opportunity, and customer sentiment within the systems agents already use. Standalone AI dashboards that agents must log into separately will not be adopted.

- Redesign incentive structures. Align agent and broker compensation with retention and customer lifetime value, not just new business volume. This both prepares for regulatory change and improves the quality of the book.

- Address the talent pipeline now. Identify which adviser cohorts are within five years of retirement. Build recruitment and development programmes that attract younger advisers with digital fluency and client-facing skills.

Advisers place only 49%–54% of their life insurance business with their primary carrier. AI-driven, high-intent lead generation reduces that leakage by giving advisers better-qualified prospects from the carrier’s own digital channels. That is a direct improvement in carrier loyalty without changing the compensation structure.

Pro Tip: Audit your partner relationships using the same profitability metrics you apply to internal channels. A high-volume distribution partner with poor loss ratios and low retention is a liability, not an asset.

Executives should also evaluate distribution partner performance using structured frameworks that go beyond premium volume. Profitability per partner, retention rates, and product mix all determine whether a partnership creates or destroys long-term value.

Key takeaways

Hybrid distribution, AI-driven analytics, and value-based incentives are the three structural changes that will separate high-performing European insurers from the rest by the end of 2025.

| Point | Details |

|---|---|

| Hybrid models are now the default | Combining digital self-service with adviser access matches how customers actually research and purchase insurance. |

| Independent channels dominate premium volume | Independent brokers control the majority of life insurance premiums, demanding structured partner management. |

| AI replaces intuition in channel decisions | Granular profitability and retention analytics per channel outperform any manual reporting approach. |

| Regulatory direction is toward value-based pay | Linking distributor compensation to persistency and customer lifetime value is both a regulatory requirement and a commercial advantage. |

| Talent succession is an urgent risk | Carriers must rebuild adviser recruitment and development pipelines before the experience gap becomes a capability crisis. |

Why I think most carriers are still solving the wrong distribution problem

The debate in most carrier boardrooms centres on which channel to invest in next. Digital or agent? Direct or broker? That framing misses the point entirely.

The real problem is that most carriers do not know, at a granular level, which of their existing channels is profitable, which is destroying margin, and which customers are worth retaining. They are making channel investment decisions on incomplete information and then wondering why the returns disappoint.

I have seen carriers pour significant budget into digital channel build-outs while their independent broker relationships, which generate the majority of their premium, are managed by a spreadsheet and a quarterly review call. That imbalance is where the real opportunity sits.

The carriers that will lead by 2026 are not necessarily the ones with the most sophisticated digital front ends. They are the ones that have built the analytics infrastructure to understand their distribution economics at the channel, partner, and product level, and then used that understanding to make deliberate decisions about where to invest, where to exit, and how to design incentives that align everyone in the chain with long-term profitability.

Technology is the enabler. But the strategic clarity has to come first.

— Tuna

How Ibapplications supports modern distribution strategies

Ibapplications builds IBSuite, a cloud-native, API-first platform that supports the full insurance value chain, including sales, policy administration, CRM, and billing. For carriers rethinking their distribution architecture, IBSuite provides the integration layer that connects digital channels, adviser workflows, and partner management into a single operational environment. The platform’s AI and automation capabilities support agent enablement and customer journey analytics without requiring carriers to replace their existing systems wholesale. If you are evaluating how a modern core platform can support your distribution goals, book a demo to see IBSuite in practice.

FAQ

What are the main insurance distribution models in 2025?

The four principal models are captive agency, independent broker, direct-to-consumer digital, and hybrid. Hybrid models, which combine digital self-service with adviser access, are the fastest-growing structure among European carriers.

Why do independent brokers dominate life insurance distribution?

Independent channels control the majority of new life insurance annual premium because they offer customers product choice and comparison that captive models cannot match. That market position gives brokers significant leverage over carriers.

How does AI improve insurance distribution performance?

AI measures profitability, retention, and loss ratios per channel with granularity that manual reporting cannot achieve. It also equips agents with predictive insights that improve renewal conversations and reduce customer lapse rates.

What does value-based compensation mean for insurance distributors?

Value-based compensation links agent and broker earnings to customer retention and lifetime value rather than new business volume alone. Regulatory frameworks across Europe are moving in this direction to align distributor incentives with policyholder outcomes.

How serious is the talent succession risk in insurance distribution?

The risk is significant. A large cohort of experienced advisers is approaching retirement, and recruitment pipelines have not kept pace. Carriers that do not rebuild their adviser development programmes now will face a capability gap at the moment hybrid distribution demands the most from their human workforce.