12.06.26

Digital claims processing: a guide for insurers

Digital claims processing is the automated use of AI-driven technologies to handle insurance claims from first notice of loss through to settlement, replacing manual workflows with structured, auditable, and faster operations. For property and casualty (P&C) insurers across Europe, the shift from paper-based or legacy electronic systems to true digital claims platforms is no longer a future ambition. It is a present competitive requirement. Platforms like Aetna’s Claims Assist Manager and Allianz’s Project Nemo demonstrate what is achievable: measurable reductions in cycle times, fewer errors, and better outcomes for policyholders. This guide explains the technology, the evidence, and the practical steps to get there.

What is digital claims processing and how does it work?

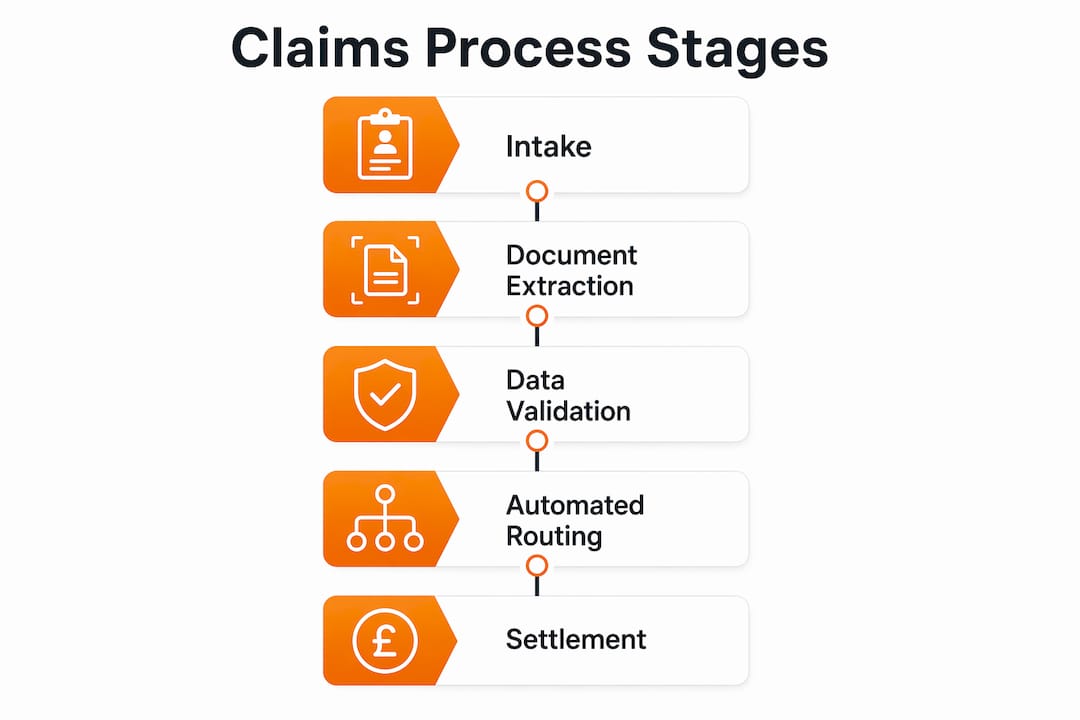

Digital claims processing, known in the industry as electronic claims management or straight-through processing, covers the full lifecycle of a claim without requiring manual intervention at each stage. A true digital claims platform handles intake, validation, fraud detection, and payment as a connected, automated sequence. Legacy systems that digitise only one step, such as electronic submission, do not qualify. The distinction matters because straight-through processing covers intake, validation, fraud detection, and payment without manual intervention at each stage, whereas legacy systems simply digitise individual steps without connecting them.

The core architecture relies on several interlocking technologies. Intelligent Document Processing (IDP) uses optical character recognition (OCR) combined with machine learning to extract structured data from claim forms, medical reports, photographs, and invoices. AI agents then classify, route, and validate that data against policy records. Digital FNOL platforms prioritise capturing structured, actionable data from the first claim notice, which is the foundation for rapid triage and downstream automation. Without clean data at intake, every subsequent step degrades in accuracy.

| Technology | Role in claims | Primary benefit |

|---|---|---|

| Intelligent Document Processing (IDP) | Extracts and structures data from documents | Eliminates manual data entry errors |

| AI classification agents | Categorise and route claims by type and complexity | Accelerates triage and reduces bottlenecks |

| Fraud detection models | Flag anomalous patterns in real time | Reduces leakage and improves accuracy |

| Workflow automation engines | Coordinate tasks across systems and teams | Cuts cycle times and removes handoff delays |

| Audit trail systems | Log every decision, override, and status change | Supports regulatory compliance and traceability |

Pro Tip: When evaluating claims processing software, ask vendors specifically whether their platform supports straight-through processing end to end or only automates individual steps. The difference in operational impact is substantial.

How does digital claims processing improve efficiency and accuracy?

The evidence from European and global insurers is consistent: automation applied across the full claims lifecycle produces significant, measurable gains. Allianz’s Project Nemo cut total claims processing time by 80% for food spoilage claims using seven specialised AI agents coordinating coverage verification through to settlement. That figure represents not a marginal improvement but a structural change in how claims operations function.

Zoom Insurance achieved a 70% reduction in processing time and 85% fewer manual data entry errors after deploying an AI-driven IDP solution. Settlement cycles fell from 14 days to under 72 hours. For policyholders, that difference is the gap between a frustrating experience and a trust-building one. For insurers, it translates directly into reduced operational cost and improved retention.

The benefits extend beyond speed:

- Fraud detection: Predictive intelligence embedded in claims workflows enables earlier risk detection and consistent decision-making across the claim lifecycle, catching anomalies that manual review would miss under volume pressure.

- Accuracy at scale: Automated claims submission removes the transcription errors that accumulate when staff re-key data from documents into systems. Zoom Insurance’s 85% error reduction illustrates this directly.

- Consistency during peak volumes: Automated systems do not slow down during catastrophe events or seasonal spikes. Structured data capture at FNOL maintains service consistency even when claim volumes surge.

- Customer satisfaction: Faster decisions reduce the anxiety policyholders experience after a loss. Shorter cycle times correlate directly with higher net promoter scores in claims satisfaction surveys across European insurers.

The combined effect of AI document processing and workflow automation can cut claim settlement times from weeks to days. That is not an incremental gain. It is a redefinition of what claims service looks like.

What is the right balance between automation and human oversight?

Automation does not replace claims expertise. It redirects it. Routine intake and data-gathering tasks become fully automated, freeing expert assessors to focus on nuanced, emotionally sensitive, or legally complex cases where human judgement is irreplaceable. This human-in-the-loop model is the standard that leading European insurers are building towards.

The practical mechanism is configurable routing. Claims below a defined complexity or value threshold proceed through automated channels without adjuster involvement. Claims that exceed those thresholds, or that trigger anomaly flags, are routed to human review with full context already assembled by the AI system. AI systems preserve human adjuster decision authority through configurable routing thresholds and confidence scoring, so adjusters receive only the cases that genuinely require their expertise.

Audit trails are non-negotiable in this model. Multi-agent AI systems log inputs, recommendations, overrides, and final claim status in immutable, queryable records that support regulatory audits and transparency requirements. For European insurers operating under Solvency II and national regulatory frameworks, this traceability is not optional. It is a compliance requirement.

The risks of over-automation are real and worth naming directly:

- Routing thresholds set too broadly push complex claims through automated channels without adequate review, increasing error rates and complaints.

- AI models trained on historical data can embed existing biases into claim decisions, requiring regular model audits.

- Document input quality directly affects AI extraction certainty; systems without automatic rerouting of uncertain extractions will produce silent errors.

- Customer-facing automation without a clear escalation path to a human creates frustration when policyholders have questions that fall outside standard workflows.

Pro Tip: Set your automation confidence threshold conservatively at first. A system that routes 60% of claims straight through with high accuracy is more valuable than one routing 90% with frequent errors. Expand automation coverage as model performance is validated.

What practical steps can insurers take to implement digital claims solutions?

Implementation begins with an honest assessment of the current state. Most European insurers operate a mix of legacy policy administration systems, point solutions for specific claim types, and manual workarounds that have accumulated over years. Before selecting claims automation solutions, map the actual claim journey end to end and identify where manual steps, data re-entry, and handoff delays occur. The gaps you find will define your requirements.

When evaluating claims processing software, prioritise platforms that offer API-first architecture. This allows integration with existing policy administration, billing, and CRM systems without requiring a full core systems replacement as a prerequisite. IBSuite, built on AWS with an API-first design, is an example of a platform designed specifically for this kind of phased integration within the P&C insurance context.

The table below contrasts two common implementation approaches:

| Approach | Description | Best suited for | Key risk |

|---|---|---|---|

| Big-bang replacement | Replace legacy claims system entirely in one programme | Insurers with highly fragmented legacy estates | High disruption, long delivery timelines |

| Phased integration | Automate specific claim types or stages incrementally | Insurers with stable core systems needing targeted gains | Scope creep if phases are not clearly defined |

A phased approach typically delivers faster return on investment and lower operational risk. Begin with high-volume, low-complexity claim types where automation confidence is highest, such as motor glass claims or straightforward property damage. Measure cycle time, error rate, and customer satisfaction at each phase before expanding scope.

Staff training is frequently underestimated. Adjusters who understand how AI routing decisions are made, and who trust the audit trail, adopt new workflows far more effectively than those who feel the system is a black box. Invest in training that explains the logic of confidence scoring and routing thresholds, not just the mechanics of the new interface.

Post-deployment, monitor four metrics consistently: straight-through processing rate, average cycle time by claim type, fraud detection rate, and customer satisfaction score. These four indicators give a complete picture of whether the digital transformation of claims is delivering its intended operational and commercial outcomes.

Key takeaways

Digital claims processing delivers its greatest value when automation, human oversight, and clean data architecture operate together as a single system rather than as separate initiatives.

| Point | Details |

|---|---|

| End-to-end automation matters | Straight-through processing covering intake to payment outperforms point-solution automation significantly. |

| Case studies confirm the gains | Allianz cut processing time by 80%; Zoom Insurance reduced errors by 85% and cycle times from 14 days to 72 hours. |

| Human oversight is structural, not optional | Configurable routing thresholds and audit trails keep adjusters in control of complex claims and satisfy regulatory requirements. |

| Phased implementation reduces risk | Starting with high-volume, low-complexity claim types builds confidence and delivers faster return on investment. |

| Data quality at FNOL determines downstream accuracy | Structured capture at first notice of loss is the single most important factor in automation performance. |

Where automation meets judgement: a perspective from the field

The conversation about digital insurance claims too often divides into two camps: those who believe automation will handle everything eventually, and those who resist change because claims is “a people business.” Both positions miss the point.

What I have observed working with insurers across Europe is that the real challenge is not the technology. The technology works. Allianz’s Project Nemo and Zoom Insurance’s IDP results are not outliers. They are reproducible with the right platform and the right data discipline. The challenge is organisational. Insurers that struggle with implementation almost always have the same problem: they have not defined where human judgement is genuinely required and where it is simply habit.

The drivers of digital transformation in insurance consistently point to customer experience as the primary commercial justification, and rightly so. But the internal justification for executives should be equally clear: automation does not just reduce cost. It improves the quality of human decisions by ensuring adjusters only see the cases that need them. An adjuster reviewing 20 complex claims per day makes better decisions than one processing 80 mixed-complexity claims under time pressure.

My caution is on data governance. Insurers that invest in AI platforms without first addressing the quality of their FNOL data, their document management practices, and their policy data integrity will find that automation amplifies existing problems rather than solving them. The technology is only as good as what you feed it. Fix the data discipline first, then automate.

— Tuna

How IBSuite supports digital claims for P&C insurers

Ibapplications built IBSuite specifically for P&C insurers who need to move beyond legacy claims systems without a disruptive full-replacement programme. IBSuite’s API-first, cloud-native architecture connects claims, policy administration, billing, and CRM within a single platform, enabling the kind of end-to-end electronic claims management that case studies from Allianz and Zoom Insurance demonstrate. The platform supports configurable routing, audit trail compliance, and Evergreen updates that keep pace with regulatory change across European markets. If you are evaluating claims automation solutions for your organisation, book a demo to see how IBSuite addresses the specific operational challenges your claims team faces.

FAQ

What is digital claims processing?

Digital claims processing is the use of AI, automation, and intelligent document processing to manage insurance claims from first notice of loss through to settlement without manual intervention at each stage. It differs from basic electronic submission by connecting intake, validation, fraud detection, and payment into a single automated workflow.

How does automated claims submission reduce errors?

Automated claims submission eliminates manual data re-entry by extracting structured information directly from documents using OCR and machine learning. Zoom Insurance recorded an 85% reduction in manual data entry errors after deploying an AI-driven IDP solution.

Do digital claims platforms replace human adjusters?

Digital claims platforms do not replace adjusters. They route routine, low-complexity claims through automated channels while directing complex, high-value, or anomalous claims to human review with full context already assembled. This model improves both efficiency and the quality of adjuster decisions.

What should insurers look for in claims processing software?

Insurers should prioritise API-first architecture, end-to-end straight-through processing capability, configurable routing thresholds, built-in audit trails, and fraud detection integration. Platforms that automate only individual steps without connecting the full claims lifecycle deliver significantly lower operational gains.

How long does it take to see results from claims automation?

Results vary by implementation scope, but phased deployments targeting high-volume, low-complexity claim types typically show measurable cycle time reductions within the first three to six months. Allianz’s Project Nemo and Zoom Insurance both reported significant gains within their initial deployment phases.

Recommended

- Insurance Claims Automation: Complete Overview for P&C Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- How can Insurers improve customer experience with modern claims processes? – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Role of Automation in Claims: Transforming P&C Insurance

- Insurance Claims Transformation: Digital Impact 2026