03.01.26

Data Management in Insurance: Fuel for Digital Growth

Over 60 percent of British insurers cite poor data management as a barrier to digital transformation and compliance. For Chief Information Officers at Central European property and casualty insurance companies, the need to build agile, compliant data systems has never been more urgent. Balancing efficiency with evolving European directives means rethinking data frameworks for robust performance and transparency. This article sheds light on the challenges and opportunities that modern data management practices offer for competitive advantage.

Table of Contents

- What Is Data Management In Insurance?

- Critical Data Types In P&C Insurance

- Key Processes: From Collection To Insights

- Legal And Regulatory Frameworks In Central Europe

- Driving Digital Innovation And Operational Efficiency

- Risks, Compliance Pitfalls, And Best Practices

Key Takeaways

| Point | Details |

|---|---|

| Data Management is Essential | Effective data management transforms raw information into actionable insights, driving operational efficiency and competitive advantage for insurers. |

| Data Governance Frameworks are Crucial | Robust data governance structures ensure data quality, compliance with regulations, and protection of sensitive information. |

| Digital Transformation is Necessary | Investing in digital technologies and data analytics is vital for modern insurers to thrive in a rapidly changing market. |

| Risk Management Approaches Must Evolve | Insurers need comprehensive risk management strategies that address technological and regulatory challenges to safeguard their operations. |

What Is Data Management in Insurance?

Data management represents a strategic foundation for modern insurers, transforming raw information into actionable insights. At its core, data management involves collecting, processing, validating, and leveraging organisational data to support critical business functions. Complex data integration processes enable insurers to streamline operations and enhance decision-making capabilities across underwriting, claims, and customer service domains.

The landscape of insurance data management encompasses multiple interconnected processes designed to address significant industry challenges. Insurers typically manage data from diverse sources including customer interactions, policy documents, claims history, risk assessments, and external market information. These datasets require sophisticated validation techniques to ensure accuracy, consistency, and regulatory compliance. By implementing robust master data management frameworks, insurance organisations can eliminate data fragmentation and create unified information repositories that support strategic objectives.

Effective data management strategies in insurance focus on several key dimensions. These include data quality control, secure storage, advanced analytics capabilities, and seamless system integration. Data security and privacy protocols play a crucial role in protecting sensitive customer information while enabling sophisticated risk assessment models. Modern insurers increasingly recognise data management not just as a technical requirement, but as a fundamental competitive advantage that drives operational efficiency and customer experience.

To illustrate the core components of insurance data management, see this summary table:

| Dimension | Key Purpose | Business Benefit |

|---|---|---|

| Data Quality Control | Ensure accuracy and consistency | Reduces errors, supports trust |

| Secure Storage | Protect sensitive information | Avoids breaches, assures clients |

| Analytics Capabilities | Generate actionable insights | Drives pricing and risk gains |

| System Integration | Unify data from various sources | Boosts efficiency, context view |

Pro tip: Implement a comprehensive data governance framework that includes regular data audits, standardised collection protocols, and continuous quality monitoring to maintain high-integrity information systems.

Critical Data Types in P&C Insurance

Property and Casualty (P&C) insurers rely on multiple critical data types that form the backbone of their operational and strategic capabilities. Comprehensive data management requires understanding the intricate landscape of information sources that drive risk assessment, pricing, and customer engagement. The primary data categories include policyholder information, claims history, underwriting details, exposure characteristics, and financial transaction records.

Each data type serves a unique and essential function within the insurance ecosystem. Policyholder data encompasses personal details, contact information, demographic characteristics, and historical interactions that enable personalised risk profiling. Claims data provides insights into historical loss patterns, frequency of incidents, and potential future risk scenarios. Underwriting details capture critical risk assessment information, including property specifications, safety measures, and risk mitigation strategies that directly influence premium calculations.

Effective management of these data types requires sophisticated integration strategies and advanced analytical capabilities. Insurance distribution channels play a crucial role in collecting and validating these diverse datasets, ensuring accuracy and comprehensiveness. Modern P&C insurers must develop robust data governance frameworks that address challenges such as data fragmentation, inconsistent standards, and the complex integration of internal and external information sources.

Pro tip: Implement a centralised data warehouse that standardises data collection protocols across all operational departments, enabling seamless information sharing and enhanced analytical capabilities.

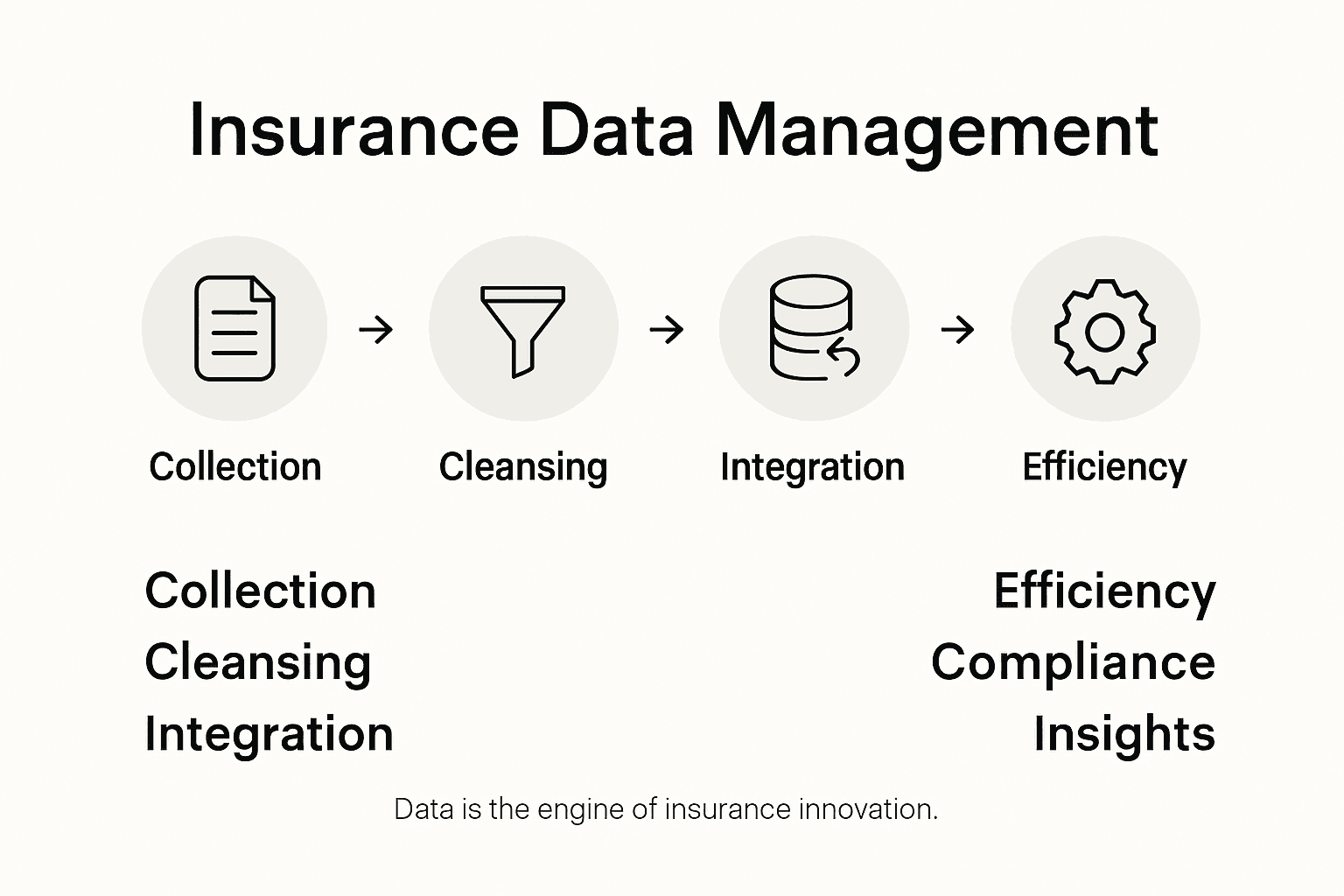

Key Processes: From Collection to Insights

The journey of data management in insurance is a sophisticated process that transforms raw information into strategic business intelligence. Key data management processes begin with comprehensive collection strategies that aggregate information from diverse sources including internal systems, customer interactions, third-party providers, and external market data. These initial collection efforts are critical for establishing a robust foundation of information that will ultimately drive organisational decision-making.

Once collected, the data undergoes rigorous validation and cleansing processes designed to ensure exceptional quality and reliability. Data validation involves multiple systematic checks to eliminate inconsistencies, remove duplicate entries, and standardise information formats. This meticulous approach guarantees that subsequent analytical processes rely on accurate, trustworthy data. Advanced insurance analytics then transform these refined datasets into actionable insights, enabling insurers to make informed strategic decisions about risk assessment, pricing models, and customer engagement.

The final stage of the data management journey focuses on advanced analytical capabilities that extract meaningful business intelligence. Sophisticated analytical tools and machine learning algorithms can uncover hidden patterns, predict potential risks, and generate nuanced insights that drive competitive advantage. Modern insurers must invest in integrated data platforms that support seamless information flow, enabling real-time decision-making and adaptive business strategies across underwriting, claims processing, and customer service domains.

Pro tip: Develop a cross-functional data governance committee that includes representatives from IT, operations, and strategic planning to ensure holistic data management approaches and alignment with organisational objectives.

Legal and Regulatory Frameworks in Central Europe

Legal and regulatory frameworks in Central Europe represent a complex and dynamic ecosystem of interconnected European Union directives and regional regulations. The primary objective of these frameworks is to ensure market stability, consumer protection, and sustainable digital transformation within the insurance sector. Solvency II stands as a cornerstone regulation, mandating rigorous risk-based capital requirements and comprehensive governance standards that insurers must meticulously implement to maintain financial resilience and operational integrity.

The regulatory landscape is characterised by multiple layers of legislative oversight, with key institutions like the European Insurance and Occupational Pensions Authority (EIOPA) playing a pivotal role in harmonising supervisory practices. Digital transformation regulations increasingly focus on balancing technological innovation with robust consumer protection mechanisms. Critical legislative frameworks such as the General Data Protection Regulation (GDPR), the emerging Artificial Intelligence Act, and sector-specific digital laws collectively shape how insurers manage data, deploy technologies, and interact with customers.

Central European insurers must navigate an increasingly complex compliance environment that demands sophisticated governance mechanisms. The regulatory approach emphasises transparency, operational resilience, and ethical technology deployment. Insurers are required to implement comprehensive data management strategies that not only meet legal requirements but also build trust through responsible data handling practices. This involves developing advanced compliance frameworks that can adapt to evolving regulatory expectations while maintaining competitive technological capabilities.

The following table compares critical regulatory frameworks relevant to Central European insurers:

| Framework | Focus Area | Impact on Insurers |

|---|---|---|

| Solvency II | Capital and risk management | Strong financial stability |

| GDPR | Data privacy protection | Strict handling of personal data |

| AI Act (emerging) | Responsible AI governance | Careful AI model deployment |

| Local Digital Laws | National compliance specifics | Regional adaptations required |

Pro tip: Establish a dedicated regulatory compliance team with cross-functional expertise in legal, technological, and operational domains to ensure holistic and proactive regulatory alignment.

Driving Digital Innovation and Operational Efficiency

Digital innovation in insurance represents a transformative journey that goes beyond technological implementation, fundamentally reimagining how insurers create value, interact with customers, and optimise operational processes. Advanced technologies such as artificial intelligence, machine learning, blockchain, and cloud computing are driving unprecedented changes in the insurance landscape. These technologies enable insurers to automate complex workflows, generate real-time insights, and deliver highly personalised customer experiences that were previously impossible.

The strategic implementation of digital technologies requires a holistic approach that encompasses technological infrastructure, organisational culture, and data management capabilities. Operational efficiency is no longer about incremental improvements but radical transformation of core business processes. Modern insurers must develop agile technological ecosystems that can rapidly adapt to changing market conditions, regulatory requirements, and customer expectations. This involves integrating sophisticated data analytics, developing seamless digital platforms, and creating flexible technological architectures that support continuous innovation.

Digitalisation models highlight the importance of understanding contextual factors that influence technological adoption. Successful digital transformation is not just about implementing new technologies but creating an integrated approach that aligns technological capabilities with strategic business objectives. Insurers must invest in building digital competencies, upskilling their workforce, and developing a culture of continuous learning and innovation that can leverage emerging technological opportunities.

Pro tip: Create a dedicated digital innovation team with cross-functional expertise that can prototype, test, and rapidly scale technological solutions across different operational domains.

Risks, Compliance Pitfalls, and Best Practices

Data transformation in the insurance sector introduces multifaceted risks that demand comprehensive and strategic mitigation approaches. These risks span technological, regulatory, and operational domains, presenting complex challenges for modern insurers. Cybersecurity vulnerabilities, data quality inconsistencies, and regulatory compliance gaps represent the most significant potential disruptions to digital transformation initiatives. Insurers must develop sophisticated risk management frameworks that anticipate and proactively address these potential threats to maintain operational resilience and protect organisational integrity.

The landscape of risk management requires insurers to implement robust data governance mechanisms that ensure systematic control and protection of information assets. Insurance compliance strategies must encompass multiple dimensions, including technical infrastructure, organisational processes, and human factors. This involves establishing clear data ownership protocols, implementing standardised quality metrics, developing automated validation mechanisms, and creating integrated governance approaches that span multiple business units and technological platforms.

Effective risk mitigation demands a holistic approach that combines technological solutions with strategic organisational capabilities. Insurers must invest in continuous employee training, develop adaptive technological architectures, and maintain rigorous compliance monitoring systems. Critical focus areas include protecting sensitive customer information, ensuring data accuracy, maintaining regulatory alignment, and developing agile response mechanisms that can quickly adapt to emerging technological and regulatory challenges. The goal is not merely compliance, but creating a resilient, proactive risk management culture that supports sustainable digital transformation.

Pro tip: Conduct quarterly comprehensive risk assessments that integrate technological, regulatory, and operational perspectives, ensuring a dynamic and proactive approach to compliance management.

Unlock the Power of Insurance Data Management for Digital Growth

The article highlights critical challenges insurers face with data fragmentation, regulatory compliance, and unlocking actionable insights from diverse data sources. If you are striving to improve data quality control, secure sensitive information, and enable seamless system integration while navigating complex Central European regulations, your digital transformation journey starts here. Achieving operational efficiency and driving innovation requires a core platform that supports end-to-end insurance processes and adapts swiftly to market demands.

Insurance Business Applications (IBA) offers IBSuite, a cloud-native, API-first platform designed specifically for property and casualty insurers seeking to accelerate digital growth through superior data management and compliance. With IBSuite you can streamline underwriting, claims, billing, and CRM to reduce IT complexity and enhance customer engagement—all while ensuring reliable regulatory adherence. Take the next step to modernise your core systems and embrace new distribution models by discovering how IBSuite can transform your insurance operations.

Explore the full benefits of IBA’s solutions today by booking a personalised demo. Don’t wait to harness data as your fuel for digital growth—act now to future-proof your insurance business with cutting-edge technology and expert support.

Frequently Asked Questions

What is data management in insurance?

Data management in insurance involves collecting, processing, validating, and leveraging organisational data to enhance decision-making, support business functions, and drive operational efficiency.

What are the critical data types in Property and Casualty (P&C) insurance?

Critical data types in P&C insurance include policyholder information, claims history, underwriting details, exposure characteristics, and financial transaction records, all of which are essential for risk assessment and customer engagement.

How do insurers ensure data quality and compliance?

Insurers implement robust data quality control measures, rigorous validation techniques, and comprehensive governance frameworks to ensure data accuracy, consistency, and adherence to regulatory requirements.

Why is digital innovation important for insurance companies?

Digital innovation is crucial for insurance companies as it transforms operations, enhances customer experience, and facilitates real-time insights, driving competitive advantage and operational efficiency.

Recommended

- Understanding Digital Maturity in Insurance Landscape – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Complete Guide to Digital Insurance Trends 2025 – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Drivers of Digital Transformation in the Insurance Industry – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- How Digital-Native Insurers Accelerate Innovation in Europe – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Top 10 Shipment Data Analysis Tools for 2025 – WISMOlabs