08.07.26

What is the insurance value chain? A 2026 guide

The insurance value chain is defined as a systematic model that segments an insurer’s operations into distinct, sequential stages, each of which generates measurable value from product conception through to claims settlement. As defined by Gabler Versicherungslexikon, this framework gives executives a structured method for managing interdependencies across functions and identifying where competitive advantage is won or lost. For European P&C insurers facing mounting pressure on margins and rising customer expectations, understanding the value chain is no longer optional. It is the analytical foundation for every meaningful efficiency and product improvement initiative.

What is the insurance value chain and why does it matter?

The insurance value chain is the end-to-end sequence of activities an insurer performs to create, price, distribute, and service a product. Value chain analysis is a vital tool for insurance executives to identify competitive positioning and prioritise operational excellence. Each stage either adds value directly to the customer or supports those that do.

The model matters because it makes invisible costs visible. When you map the chain, you see exactly where capacity is consumed, where manual effort concentrates, and where technology can replace human intervention. Without this map, digital transformation programmes tend to automate the wrong things first.

The framework also clarifies accountability. Each stage has a distinct owner, a measurable output, and a clear handoff to the next stage. That clarity is what separates insurers who execute transformation at pace from those who spend years in pilot programmes.

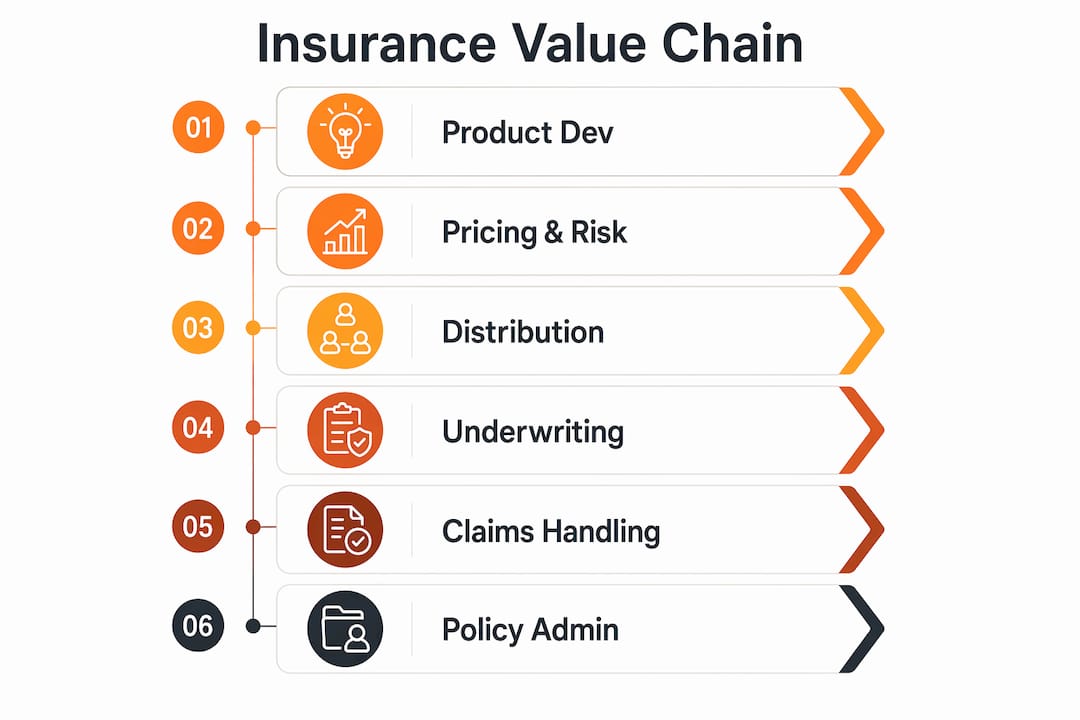

What are the key components of the insurance value chain?

The chain typically divides into six core stages. Each stage has a distinct function and a direct bearing on overall insurer performance.

| Stage | Primary function |

|---|---|

| Product development | Designing coverage structures, pricing models, and policy wordings |

| Distribution | Acquiring customers through agents, brokers, digital channels, or affinity partners |

| Underwriting | Assessing and pricing individual risks using actuarial and data-driven methods |

| Policy administration | Issuing, endorsing, renewing, and cancelling policies throughout their lifecycle |

| Claims management | Receiving, validating, settling, and closing claims efficiently and accurately |

| Customer service | Handling enquiries, complaints, and retention across all touchpoints |

Operational capacity is not spread evenly across these stages. Claims handling consumes 41% of total operational capacity, and policy management accounts for a further 32%. Together they represent nearly three quarters of an insurer’s operational effort. That concentration makes them the highest-priority targets for any efficiency programme.

The distribution stage is often underestimated. Insurers who treat distribution as a passive channel rather than an active value-creating function miss significant opportunities to gather risk data, personalise products, and reduce acquisition costs. Modern insurtech solutions are transitioning insurers from monolithic systems to modular, API-first architectures precisely to make distribution more flexible and data-rich.

Pro Tip: Map your internal capacity allocation against the six stages before committing to any automation investment. If your data shows a different concentration than the 41%/32% benchmark, that divergence itself is a diagnostic finding worth investigating.

How is modern technology transforming the insurance value chain?

Technology is reshaping every stage of the chain, but the gains are uneven and the barriers are real. AI implementation across the value chain is projected to generate productivity gains of up to 30% over the next three to five years. That figure represents a structural shift in how insurers compete on cost.

Digital transformation can reduce operating costs by 10–20%, with claims processing specifically improving by 20–30%. These are not marginal gains. They represent the difference between an insurer that can price competitively and one that cannot.

The current state of automation reveals how much headroom remains:

- Straight-through processing rates sit just above 50% for policy administration and under 10% for claims handling.

- Over 90% of claims handling events still require manual intervention.

- Most automation projects fail to deliver expected returns because they are built on inaccurate process data rather than verified process intelligence.

The last point is the one most executives underestimate. Automating a broken process at speed produces broken outcomes at scale. The drivers of digital transformation in insurance are well understood, but execution consistently falls short when process insight is missing.

Agentic AI represents the next frontier. Rather than automating discrete tasks, agentic systems act as an orchestration layer across the entire chain, making decisions, routing work, and escalating exceptions without human prompting. Insurance cores must evolve into intelligent cores that support agentic AI orchestration while retaining compliance logic and regulatory governance. That requirement places significant demands on legacy system architectures.

Pro Tip: Before deploying any AI tool in claims or policy administration, audit your straight-through processing rate by process variant, not by average. Averages hide the long tail of complex cases that consume disproportionate effort.

What strategic approaches are insurers adopting to leverage the value chain fully?

Technology adoption alone does not produce sustainable competitive advantage. The main barrier to digital transformation is structural realignment rather than technology availability. Embedding AI requires process redesign, not just software installation.

Leading European insurers are adopting four strategic approaches to extract full value from the chain:

-

Agentic-First redesign. Agentic-First operating models require re-engineering core business processes around AI capabilities rather than bolting AI onto existing workflows. Incremental add-ons yield limited improvement. Fundamental redesign is what produces measurable gains.

-

Process mining as a foundation. Process mining reduces cycle times by up to 37% and increases automation rates by approximately 35%. It works by extracting event log data from core systems to reveal exactly how processes actually run, not how they were designed to run. That distinction is critical.

-

Modular architecture adoption. Insurers moving from monolithic platforms to cloud-native, API-first systems gain the ability to update individual value chain stages without disrupting the whole. This architectural shift is a prerequisite for the speed of product innovation that modern distribution demands.

-

End-to-end operating model repositioning. Success with AI comes from repositioning the entire operating model to harness agentic AI end-to-end, not from isolated applications in one department. Insurers who treat AI as a claims tool or an underwriting tool, rather than as an enterprise capability, consistently underperform on ROI.

Pro Tip: Use process mining to identify your top five process variants by volume before selecting automation candidates. Process mining uncovers hidden inefficiencies that no stakeholder interview or process map will surface.

How can executives apply value chain insights to improve efficiency?

The insurance process value chain is most useful when it moves from a conceptual model to an operational diagnostic tool. Executives who use it well follow a consistent pattern.

They start with capacity data. Knowing that claims and policy management consume the majority of operational effort tells you where automation delivers the highest return. Knowing your own organisation’s specific split tells you whether you are above or below industry norms and why.

They then prioritise by automation readiness, not by ambition. A process with high volume, low complexity, and clean data is a better first automation candidate than a high-value but exception-heavy process. Digitising insurance processes works best when sequenced by readiness rather than by perceived strategic importance.

Advanced analytics and AI also open new possibilities in underwriting and product development. Insurers using telematics data, IoT signals, and behavioural analytics can build personalised products that price risk more accurately and attract lower-risk customers. This is where the value chain connects directly to product strategy, not just operational efficiency.

Data quality underpins all of it. Poor data produces poor models, poor automation, and poor decisions. Insurers who invest in data governance before scaling AI consistently outperform those who do not. The back-office transformation guide for 2026 outlines how leading P&C insurers are structuring this investment.

For a practical overview of insurance terminology across the chain, the insurance glossary provides a useful reference for aligning teams on shared definitions before embarking on process redesign.

Key takeaways

The insurance value chain is the single most useful framework for identifying where operational effort concentrates and where technology investment will generate the highest return.

| Point | Details |

|---|---|

| Claims and policy management dominate capacity | These two stages consume 73% of operational effort and are the highest-priority automation targets. |

| Straight-through processing rates reveal automation gaps | Rates below 10% in claims signal major efficiency potential that most insurers have not yet captured. |

| Process mining precedes effective automation | Insurers must map actual process behaviour before scaling automation to avoid compounding existing inefficiencies. |

| Agentic-First redesign outperforms incremental AI | Bolting AI onto existing workflows produces limited gains; full process redesign around AI capabilities is required. |

| Data quality determines transformation outcomes | Insurers who govern data before scaling AI consistently outperform those who treat data quality as a secondary concern. |

The value chain is not a map. It is a mirror.

Most executives I speak with treat the insurance value chain as a diagram on a slide. They use it to communicate structure, not to drive decisions. That is a missed opportunity of the first order.

What the value chain actually does, when used properly, is reflect your organisation’s real operating logic back at you. The gap between your designed process and your actual process is where your costs live. Process mining makes that gap visible. Agentic AI closes it. But neither works if leadership treats the value chain as a static reference rather than a living diagnostic.

The insurers I have seen make genuine progress in 2025 and into 2026 share one characteristic. They stopped asking “where can we apply AI?” and started asking “which stage of our value chain is producing the most friction, and why?” That reframe changes everything. It shifts the conversation from technology procurement to process ownership, and process ownership is where accountability lives.

The uncomfortable truth is that most transformation programmes fail not because the technology is wrong, but because the process insight was never there to begin with. You cannot automate your way out of a process you do not understand. The value chain framework, used seriously, forces that understanding before the investment is made.

— Tuna

How IBSuite supports the full insurance value chain

Ibapplications has built IBSuite specifically to support every stage of the insurance value chain, from sales and underwriting through to claims, billing, and financial sub-ledger. The platform runs on AWS as a cloud-native, API-first system, which means individual value chain stages can be updated or extended without disrupting core operations. For P&C insurers looking to move beyond incremental fixes and towards a genuinely integrated operating model, book a demo with Ibapplications to see how IBSuite handles the full chain in practice. The platform’s Evergreen update model also removes the maintenance burden that typically slows down transformation programmes.

FAQ

What is the insurance value chain in simple terms?

The insurance value chain is the sequence of activities an insurer performs to create and deliver a product, from product development and distribution through to claims settlement and customer service. Each stage adds value and feeds into the next.

Which stage of the value chain offers the greatest efficiency gains?

Claims handling offers the greatest potential, consuming 41% of operational capacity with straight-through processing rates below 10%. Automating even a fraction of manual claims events produces significant cost and speed improvements.

What is process mining and why does it matter for the value chain?

Process mining extracts event log data from core systems to reveal how processes actually run, identifying inefficiencies invisible to standard analysis. It reduces cycle times by up to 37% and increases automation rates by approximately 35%.

How does an Agentic-First model differ from standard AI adoption?

An Agentic-First model re-engineers core processes around AI capabilities rather than adding AI tools to existing workflows. Standard AI adoption produces limited gains; full process redesign produces measurable, sustained improvements across the value chain.

What role does data quality play in value chain transformation?

Data quality determines the accuracy of every AI model, automation rule, and analytics output built on top of core systems. Insurers who invest in data governance before scaling AI consistently outperform those who do not.

Recommended

- Complete Guide to Digital Insurance Trends 2025 – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance API marketplaces: the executive guide

- 2025 Guide to Insurance Analytics: Transform Your Decisions – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- What is an end-to-end insurance platform: a 2026 guide