26.06.26

Insurance back-office transformation: a 2026 guide for executives

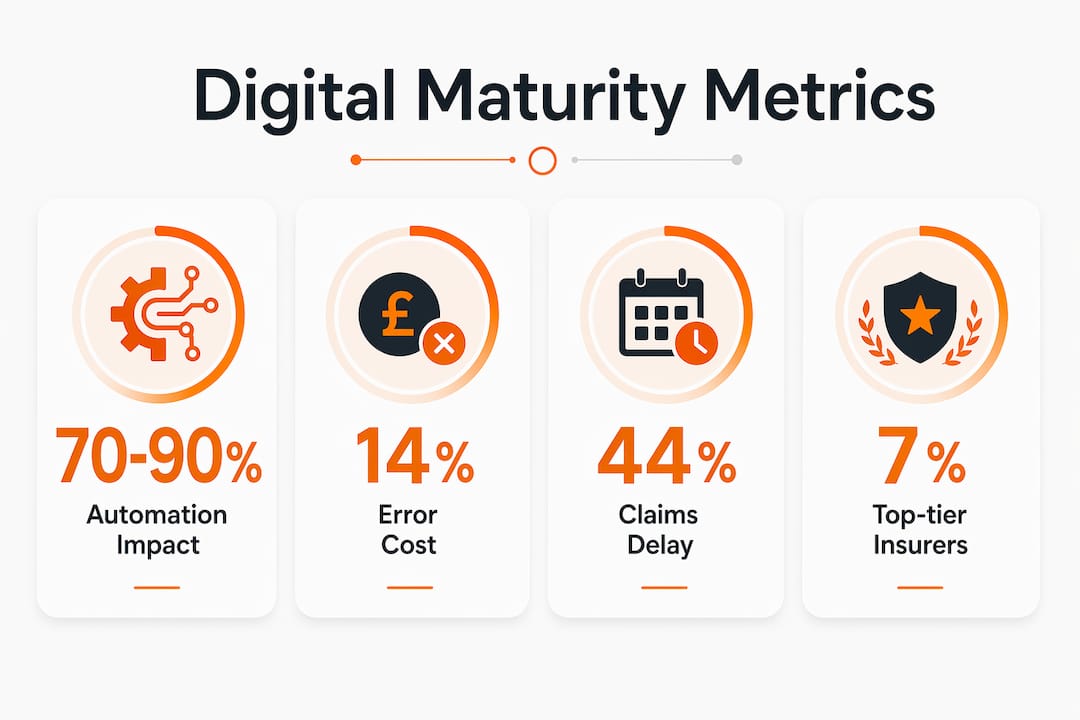

Insurance back-office transformation is the process of digitally redesigning operational tasks across the insurance value chain to reduce errors, cut costs, and build the agility needed to compete. The industry standard term for this discipline is operational modernisation, and the two concepts are used interchangeably throughout this article. European insurers currently spend 14% of operational budgets correcting manual errors and rework. That single figure explains why boards are treating back-office change as a financial priority, not an IT project. Top-performing insurers who have completed this shift report an 8.1 percentage point rise in premium revenue and a 2.6 percentage point reduction in their expense ratio compared to peers.

What are the key components driving insurance back-office transformation?

Insurance back-office transformation rests on three interdependent pillars: AI-powered automation, workflow redesign, and system integration. Remove any one of them and the effort stalls. Understanding how they interact is the starting point for any executive planning a credible programme.

AI-powered automation is the fastest route to measurable cost reduction. Back-office automation reduces manual data entry by 70–90% and delivers return on investment within the first quarter for workflows such as accounts payable, onboarding, and compliance reporting. That speed matters because it creates early proof points that sustain board confidence through longer phases of change.

Workflow redesign addresses the processes that automation alone cannot fix. Accounts payable, new business onboarding, and regulatory reporting each carry embedded inefficiencies that predate digital tools. Redesigning these workflows before automating them prevents the well-known trap of simply accelerating a broken process. Compliance automation is a particularly high-value target because regulatory reporting errors carry both financial and reputational penalties.

System integration is where most transformation programmes hit their first serious obstacle. Legacy policy administration and claims platforms were not built to share data. Middleware and API gateways allow insurers to build modern, digital-first operations around existing systems incrementally, avoiding the delays and risks of full replacement. This approach keeps the business running while new capabilities are layered on top.

Pro Tip: Distinguish between digitisation and digital transformation before you budget. Digitisation converts paper to data. Digital transformation redesigns the operating model around that data. Funding the first while expecting the second is the most common cause of disappointed boards.

| Component | Technology | Primary impact |

|---|---|---|

| AI-powered automation | Machine learning, RPA | 70–90% reduction in manual data entry |

| Workflow redesign | BPM platforms, process mining | Elimination of embedded inefficiencies |

| System integration | Middleware, API gateways | Legacy continuity during modernisation |

| Compliance reporting | Regulatory automation tools | Reduced penalty risk and audit time |

How do top-performing insurers measure digital maturity?

Digital maturity in insurance is defined by execution quality, not by the volume of technology investment. The ACORD 2026 Insurance Digital Maturity Study makes this distinction clearly. Only 7% of the world’s largest insurers reach the top tier of digital maturity, yet those firms consistently outpace average insurer profitability. The gap between the 33% who are fully digitised and the 7% who are truly mature reveals that technology deployment and business performance are not the same thing.

What separates the top tier from the rest comes down to four characteristics:

- End-to-end digital integration. Top performers connect sales, underwriting, policy administration, claims, and finance into a single data flow. Siloed digitisation produces islands of efficiency that do not compound.

- ACORD data standards adoption. Standardised data structures allow AI and automation tools to scale across business lines without custom integration work for each new deployment.

- Operating model alignment. Outperforming insurers over-index on automation and digitisation of their operating models, not just their customer-facing channels.

- Continuous measurement. Mature insurers track transformation outcomes with the same rigour applied to underwriting results. KPIs are set before programmes begin, not after.

Understanding digital maturity in insurance as a competitive differentiator rather than a compliance exercise changes how executives allocate resources. Firms that treat maturity as a destination tend to plateau. Firms that treat it as an ongoing discipline keep compounding the gains.

What organisational challenges block effective back-office transformation?

Technology is rarely the primary reason transformation programmes fail. Organisational barriers such as leadership misalignment, resistance to change, and weak governance block effective transformation far more often than technology gaps do. This is the finding that most executive teams underestimate when they begin.

The most common failure pattern follows a predictable sequence:

- A transformation programme is launched as a technology project with an IT sponsor but no C-suite ownership.

- Individual business units run parallel digitisation efforts with incompatible data models.

- Early automation wins are not connected to enterprise-wide outcomes, so momentum fades.

- The programme is declared complete when the technology goes live, before business outcomes are measured.

A federated governance model addresses this directly. Central standards and KPIs are set at group level. Local teams retain the authority to execute within those standards. This balance prevents both the rigidity of top-down mandates and the fragmentation of fully devolved programmes.

Exception handling deserves specific attention. Failure to plan for exceptions in AI automation leads to operational stalls when the system encounters a case it cannot resolve. Well-designed workflows include automated escalation paths that route complex cases to human reviewers without interrupting the broader process. This is not a technical detail. It is a governance decision about where human judgement sits in the operating model.

Pro Tip: Before launching any automation programme, map every exception scenario for the target workflow. Define the escalation path, the responsible owner, and the resolution time target. Automation without exception governance creates new bottlenecks rather than removing old ones.

The capacity to sense market changes and realign resources quickly is what separates successful transformation initiatives from those that stall after the initial deployment. Executives who build this sensing capability into their governance model sustain transformation momentum. Those who do not find themselves repeating the same programme every three years.

What strategies should European insurers adopt to accelerate back-office change?

European insurers face a specific set of constraints that shape how transformation should be sequenced. Regulatory complexity across multiple jurisdictions, legacy system estates that predate modern APIs, and skills gaps in data engineering all affect the pace and approach. The strategies that work acknowledge these constraints rather than ignoring them.

Incremental integration consistently outperforms all-at-once system replacement. Replacing a core policy administration platform in a single programme carries execution risk that most insurers cannot absorb. Layering modern capabilities via API gateways over existing systems allows the business to capture automation benefits in months rather than years. The legacy system continues to operate while the new layer handles specific workflows.

Targeting quick-return workflows first builds the internal credibility that sustains longer programmes. Accounts payable automation, new business onboarding, and claims triage are consistently the highest-return starting points. Each delivers measurable cost reduction within a single quarter, creating the financial case for the next phase. The drivers of digital transformation in European insurance increasingly include regulatory pressure on expense ratios, which makes these early wins doubly valuable.

Treating transformation as a continuous practice rather than a project is the single most important strategic shift available to European insurance executives. Digital transformation in insurance requires continuous, organisation-wide redesign of operating models for measurable business outcomes. Firms that close a transformation programme and move on lose the compounding benefits that accrue to those who keep iterating.

| Strategy | Approach | Expected outcome |

|---|---|---|

| Incremental integration | API gateway over legacy systems | Faster deployment, lower execution risk |

| Quick-return workflow targeting | Accounts payable, onboarding, claims triage | ROI within first quarter |

| Federated governance | Central KPIs, local execution authority | Coordinated change without rigidity |

| Continuous transformation | Ongoing operating model iteration | Sustained competitive advantage |

| Data standards adoption | ACORD-aligned data architecture | AI and automation scale across business lines |

Key takeaways

Insurance back-office transformation succeeds when governance, data standards, and incremental automation are combined as a continuous discipline rather than a one-time project.

| Point | Details |

|---|---|

| Manual errors carry a direct cost | Insurers spend 14% of operational budgets on rework, making automation a financial priority. |

| Digital maturity is about execution | Only 7% of large insurers reach top-tier maturity; investment volume alone does not drive outcomes. |

| Governance determines success | Federated models with central KPIs and local authority outperform both top-down and siloed approaches. |

| Incremental integration reduces risk | API gateways over legacy systems deliver automation benefits without full platform replacement. |

| Transformation is a discipline | Firms that treat modernisation as ongoing compound gains; those that treat it as a project plateau. |

Why the governance question matters more than the technology question

The conversations I find most revealing with insurance executives are not about which platform to buy. They are about who owns the transformation outcome. In my experience, the firms that struggle most are those where the chief information officer is accountable for delivery but the chief financial officer controls the budget and the chief operating officer owns the affected processes. Nobody is wrong in that structure. But nobody is fully right either.

The technology available to European insurers in 2026 is genuinely capable. AI automation tools, API-first platforms, and cloud-native core systems can deliver the efficiency gains the research describes. The constraint is almost never the technology. It is the absence of a single executive who can say, with authority, what the operating model should look like in three years and hold the organisation to that picture through quarterly budget cycles and personnel changes.

I have also observed a pattern worth naming directly. Firms that launch transformation with a strong governance model but modest technology ambitions consistently outperform firms that invest heavily in technology without resolving governance first. The insurance operations transformation literature supports this, but it is also simply what the data shows when you compare outcomes across programmes.

The practical advice I would offer any executive reading this is to spend the first 90 days of any transformation programme on governance design, not technology selection. Define who owns the outcome. Define what the KPIs are. Define the escalation path when local teams resist central standards. Get those three things in writing before a single vendor is engaged. The technology decision becomes significantly easier once the governance structure is clear.

— Tuna

How IBSuite supports back-office modernisation for P&C insurers

Ibapplications has built IBSuite specifically for property and casualty insurers who need to modernise operations without replacing every system at once. IBSuite is an API-first, cloud-native platform covering the full insurance value chain, from underwriting and policy administration through to claims, billing, and financial sub-ledger. It connects to existing systems via standard APIs, which means European insurers can book a demo and see how incremental integration works in practice before committing to a full programme. IBSuite also supports ACORD data standards natively, which removes one of the most common barriers to scaling AI automation across business lines.

FAQ

What is insurance back-office transformation?

Insurance back-office transformation is the process of redesigning operational workflows across policy administration, claims, compliance, and finance using automation, digitisation, and modern integration tools. The goal is measurable improvement in cost, speed, and accuracy across the insurance value chain.

How much do manual errors cost insurers?

Insurers spend 14% of operational budgets correcting manual errors and rework, and 44% of firms experience claims settlement delays of more than 60 days as a direct consequence. Eliminating these costs is the primary financial case for back-office automation.

What differentiates top-tier digital maturity in insurance?

Top-tier insurers, representing just 7% of large carriers, achieve superior profitability through end-to-end digital integration and consistent execution rather than higher technology spend. ACORD data standards adoption and operating model alignment are the two most consistent differentiators.

Why do back-office transformation programmes fail?

The most common causes are leadership misalignment, siloed digitisation efforts, and the absence of a federated governance model. Programmes that treat transformation as a technology project rather than an operating model change consistently underdeliver on their business case.

What is the fastest way to generate ROI from back-office automation?

Targeting accounts payable, new business onboarding, and compliance reporting first delivers return on investment within the first quarter. AI-powered automation in these workflows reduces manual data entry by 70–90%, creating early financial proof points that sustain board support for broader programmes.

Recommended

- Insurance IT strategy 2025: a P&C executive guide

- Insurance Claims Transformation: Digital Impact 2026

- Insurance Operations Transformation: Complete Expert Guide – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance Digital Transformation Guide for Effective Change – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System