25.05.26

What is claims adjudication in P&C insurance?

Claims adjudication is one of the most consequential processes in insurance operations, yet it is persistently misunderstood. Many practitioners treat it as a single moment when a claim is approved or denied. In reality, claims adjudication is the insurer’s decision process to evaluate each claim against policy scope, coverage evidence, and applicable rules before producing a binding outcome. For insurance professionals and business analysts working in property and casualty insurance, understanding how adjudication actually works is the foundation for diagnosing bottlenecks, reducing costs, and improving settlement speed.

Table of Contents

- Key takeaways

- What claims adjudication means in P&C insurance

- The adjudication gates that determine outcomes

- Automation and manual review in adjudication operations

- Using adjudication data to improve claims performance

- My perspective on what teams get wrong

- Take the next step in claims efficiency

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Adjudication is a decision engine | Claims adjudication evaluates coverage, evidence, and policy rules to produce a binding pay or no-pay outcome. |

| Multiple gates exist in every claim | Each adjudication stage acts as a checkpoint; failure at any gate determines whether a claim is approved, denied, or pended. |

| Automation reduces cycle time | Straight-through processing for simple claims cuts manual workload significantly; exceptions should be the minority, not the norm. |

| Reason codes drive analytics | Accurate capture of adjudication reason codes is mandatory for meaningful denial reporting and root-cause analysis. |

| Gate-level failure data is more useful | Tracking which specific rule fails, rather than just the final outcome, gives analysts the sharpest lever for process improvement. |

What claims adjudication means in P&C insurance

Claims processing and claims adjudication are not the same thing, even though many teams use the terms interchangeably. Claims processing is the full workflow: intake, coverage verification, adjudication, payment execution, and file closure. Adjudication is specifically the decision point within that workflow. It is where the insurer determines whether to pay, how much to pay, or whether to reject the claim entirely.

Think of processing as the pipeline and adjudication as the valve that controls what flows through.

In P&C insurance, the adjudication decision sits between coverage verification and payment. Once a claim has been registered and initial documentation gathered, the adjudicator, whether human or automated, applies the policy terms to the facts of the loss. This involves checking whether the policy was active at the time of the incident, whether the cause of loss is a covered peril, whether any exclusions apply, and whether the claimed amount falls within policy limits.

A straightforward example: a policyholder submits a claim for storm damage to a commercial property. The adjudicator confirms the policy was in force on the date of the storm, verifies that windstorm is a covered peril under the policy schedule, checks that no relevant exclusion applies (such as flood, which may require a separate endorsement), and confirms the repair estimate sits within the sum insured. Each of these is a discrete check, not a single judgement call.

Adjudication logic is commonly automated for high-volume, low-complexity lines, with exception-based manual review handling cases that fall outside predefined rules. This blend is standard across modern P&C operations, and the ratio between automated and manual handling is one of the clearest indicators of operational maturity.

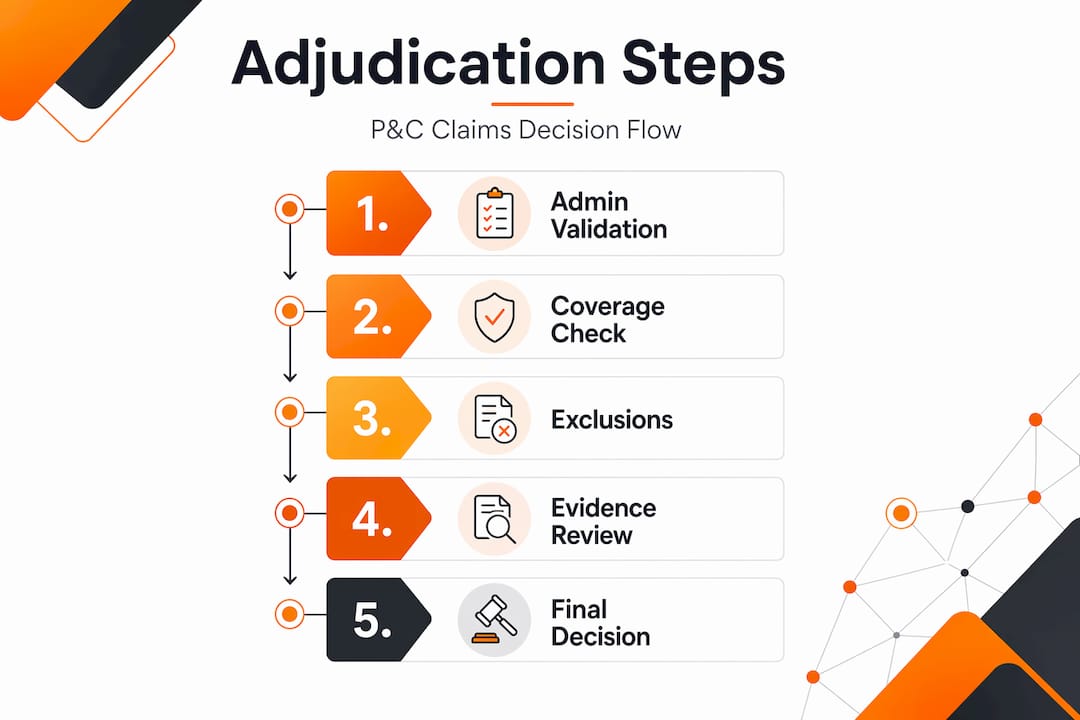

The adjudication gates that determine outcomes

Every claim passes through a sequence of evaluation checkpoints before a final decision is reached. Business analysts often refer to these as “gates.” Failure at any gate produces a specific outcome: approval, denial, adjustment, or a temporary hold known as a pend.

The table below maps the core adjudication gates to their typical failure outcomes in a P&C context:

| Adjudication gate | What is checked | Failure outcome |

|---|---|---|

| Administrative validation | Policy active, correct insured, documentation complete | Pend or rejection for missing information |

| Coverage eligibility | Is the peril covered under the policy schedule? | Denial for non-covered peril |

| Exclusions review | Do any policy exclusions apply to this loss? | Denial or partial adjustment |

| Prior obligations | Was notice given within required timeframe? | Denial for late notification |

| Endorsements and conditions | Do any special conditions or endorsements modify cover? | Adjusted payment amount |

| Quantum assessment | Is the claimed amount supported by evidence and within limits? | Payment adjusted to validated figure |

Claims may be approved, denied, or adjusted after each of these checks, with reason codes attached to every outcome. Those reason codes are not administrative formalities; they are the primary data source for understanding why claims fail and where process improvements will have the most effect.

Pended claims represent a distinct category. A pend is not a denial. It is a temporary hold that stops automatic processing to request further documentation or specialist input. Confusing pends with denials in your reporting will skew your denial rate and obscure the real drivers of cycle time.

Pro Tip: Map every adjudication failure back to the specific gate that triggered it, not just the final label of “denied” or “pended.” This single change to your reporting framework will reveal the most common failure points and tell you exactly where to focus rule tuning or training efforts.

Automation and manual review in adjudication operations

The operational question for most P&C claims teams is not whether to automate adjudication, but how to manage the boundary between straight-through processing and manual intervention effectively.

Straight-through processing applies where claims meet a defined set of criteria: the policy is unambiguous, the peril is clearly covered, the loss is within a predictable range, and no flags are raised by the rules engine. For these claims, automated adjudication produces a decision without human involvement, often within seconds. High exception rates increase claims cycle times significantly, which is why reducing the volume of claims that fall out of straight-through processing is one of the primary levers for operational efficiency.

Manual adjudication handles the cases that automation cannot resolve cleanly. These include large or complex losses, disputed claims, cases with ambiguous coverage language, and claims where fraud indicators have been raised. Large claims enter manual adjudication queues triggered by external intervention rules, with SLA tracking applied to each status to maintain performance accountability.

Here is a practical sequence for optimising your adjudication workflow:

- Audit your exception rate. Establish what percentage of claims exit straight-through processing and why. Most teams find that a small number of rule gaps account for a large proportion of exceptions.

- Classify your manual queue. Separate genuine complexity (large losses, disputes) from avoidable exceptions (data quality issues, missing documentation at intake). These require different solutions.

- Tune your rules engine. Work with claims specialists to update adjudication rules based on recent case outcomes. Rules that were accurate two years ago may no longer reflect current policy wordings or regulatory requirements.

- Introduce AI-assisted triage. Predictive models can flag claims likely to require manual review before they enter the adjudication queue, allowing earlier specialist allocation. The role of automation in P&C claims continues to expand as these models mature.

- Track SLA compliance by queue type. Manual adjudication performance depends entirely on whether the right claims are routed to the right specialists within the right timeframe. SLA data by claim type reveals where routing logic needs adjustment.

Technology matters here, but the rules that govern the system matter more. A well-calibrated rules engine with accurate policy data will outperform a poorly configured AI system every time.

Using adjudication data to improve claims performance

For business analysts, the most valuable output of the adjudication process is not the payment decision. It is the structured data that accompanies every decision. Adjudication reason codes tied to plan rules are the raw material for meaningful denial analytics, exception trend reporting, and process benchmarking.

Getting value from this data requires a few disciplines that are often overlooked:

- Accurate reason code capture at point of decision. Incorrect or generic codes corrupt your analytics. If your system allows adjusters to select “other” as a reason code, that category will gradually absorb the most instructive data in your dataset.

- Gate-level failure tracking. Business analysts should track which gates cause failures rather than only monitoring final approval or denial rates. A high denial rate at the exclusions gate points to a different problem than a high denial rate at the administrative validation stage.

- Adjudication variability analysis. Similar claims can produce different outcomes when routing attributes differ, such as coverage tiers, network contracts, or policy endorsements. Identifying this variability helps you find inconsistency in rule application, which is often a training issue rather than a system issue.

- Cycle time by adjudication outcome. Segment your average handling time by outcome type. Pended claims typically inflate cycle time figures disproportionately; understanding this allows more accurate benchmarking and SLA setting.

- Customer-facing communication. Transparent, timely communication about adjudication outcomes drives measurable improvements in satisfaction. When customers understand why a claim has been pended or adjusted, and what they can do next, complaint volumes fall. The customer experience in modern claims processes is directly shaped by how well adjudication outcomes are communicated.

Dashboards that surface these metrics at team and individual level give operations managers the visibility to act quickly when failure rates shift. The goal is to treat adjudication not as a back-office function but as a measurable, improvable process with clear performance indicators.

My perspective on what teams get wrong

I have seen adjudication treated as the claims team’s equivalent of a rubber stamp. Something that happens after the real work of investigation is done. That framing causes real harm to operations.

When you treat adjudication as a single approval step rather than a multi-gate decision engine, you lose the diagnostic value that lives inside the process. The teams I have seen make the most meaningful improvements to cycle time and cost are not the ones who invested in faster adjudication. They are the ones who invested in understanding where and why their adjudication was failing.

The other mistake I see regularly is measuring adjudication health by final paid or denied counts alone. Those headline numbers tell you almost nothing useful. What tells you something useful is your exception rate by claim type, your average time-in-status for pended claims, and the distribution of failure reasons across your adjudication gates. These are the numbers that point to fixable problems.

Balancing regulatory compliance with operational speed is genuinely difficult, and I would not pretend otherwise. But the teams that get it right do so by keeping their rules engines current and their data clean, not by adding more manual reviewers to an already strained process.

— Tuna

Take the next step in claims efficiency

Understanding the claims adjudication process is the starting point. Applying that understanding through the right platform is where operational gains become real. Ibapplications builds P&C insurance platforms that support the full claims lifecycle, from intake through to adjudication and payment, with automation and rules-based decision logic built in. If you want to see how a modern claims workflow handles adjudication at scale, book a demo with the Ibapplications team. You can also explore their detailed guide on streamlining claims processing for further operational insight.

FAQ

What is claims adjudication?

Claims adjudication is the process by which an insurer evaluates a submitted claim against policy terms, coverage rules, and evidence to produce a binding decision to pay, deny, or adjust the claim. It is a structured decision process, not a single administrative step.

How does claims adjudication work in P&C insurance?

The adjudication process moves a claim through a series of gates: administrative validation, coverage eligibility, exclusions review, prior obligations, endorsements, and quantum assessment. Each gate applies specific rules, and failure at any point produces a defined outcome such as denial or a temporary pend.

What is a pended claim in adjudication?

A pended claim is one placed on temporary hold during adjudication, usually because additional documentation or specialist review is required. A pend is distinct from a denial and should be tracked separately in reporting to avoid distorting denial rate metrics.

Why do similar claims sometimes receive different adjudication outcomes?

Different adjudication outcomes for similar claims typically result from differences in routing attributes such as coverage tiers, policy endorsements, or contractual conditions. Identifying this variability is a key task for business analysts reviewing adjudication consistency.

What is the importance of claims adjudication for operational efficiency?

Adjudication is the point in the claims workflow where the most data is generated about why claims succeed or fail. Accurate reason code capture and gate-level failure tracking allow operations teams to target process improvements precisely, reducing both cycle time and unnecessary manual handling.

Recommended

- Insurance Claims Automation: Complete Overview for P&C Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Role of Automation in Claims: Transforming P&C Insurance

- How can pet insurers improve customer satisfaction through claims automation? – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Automation and Artificial Intelligence in P&C Insurance – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System