20.05.26

Regulatory compliance in insurance: 2026 guide

Nearly half of European insurers faced fines or refunds due to compliance errors in recent years, and 70% plan to increase compliance investment in 2026. Yet many teams still treat regulatory compliance in insurance as a documentation exercise rather than an operational discipline. That gap between policy and practice is precisely where penalties, examinations, and reputational damage occur. This guide moves past the theory. It offers compliance officers, risk managers, and insurance professionals a clear view of the current regulatory environment, the most common failure points, and the strategies that actually hold up under scrutiny.

Table of Contents

- Key takeaways

- Regulatory compliance in insurance: the full picture

- Where compliance programmes break down

- Building an effective compliance programme

- Key frameworks shaping compliance today

- What is changing in insurance compliance

- My perspective on compliance as a business capability

- How IBSuite supports compliance-driven insurers

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Compliance is operational, not clerical | Regulators examine evidence of control execution, not just the existence of written policies. |

| Fragmented regulation demands adaptability | Jurisdictions interpret frameworks differently, requiring structured overlay methods to avoid compliance gaps. |

| Cross-functional ownership matters | Effective compliance spans underwriting, claims, IT, and finance, not just the legal or compliance team. |

| Early action reduces examination risk | Prompt scoping, testing, and remediation, particularly for MAR, substantially improves governance outcomes. |

| Automation shifts compliance from reactive to continuous | Compliance-as-a-service tools support real-time evidence collection and ongoing regulatory readiness. |

Regulatory compliance in insurance: the full picture

Regulatory compliance in insurance means satisfying the legal, financial, and operational standards set by the authorities that govern how insurers conduct business. That sounds straightforward. In practice, it covers licensing requirements, solvency and financial reporting obligations, consumer protection rules, claims handling standards, data privacy mandates, and marketing conduct requirements. Across Europe, national regulators interpret and enforce these standards with meaningful variation, which is what makes the compliance workload genuinely demanding.

The operational areas affected are broad. Consider what a mid-sized P&C insurer must manage:

- Underwriting controls: pricing adequacy, rate filing adherence, and anti-discrimination requirements

- Claims handling: timeliness standards, documentation obligations, and fair settlement practices

- Financial reporting: solvency margins, reserving accuracy, and audit trail integrity

- IT and data governance: cyber security controls, data residency requirements, and system access management

- Consumer conduct: clear communication of policy terms, marketing accuracy, and complaints handling

What distinguishes effective insurers from those that repeatedly face regulatory scrutiny is the move from event-based compliance to continuous readiness. Event-based compliance means preparing intensively for an upcoming examination, then relaxing once it passes. Continuous readiness means controls are running, documented, and tested as part of normal operations, every quarter, not just before a regulator arrives.

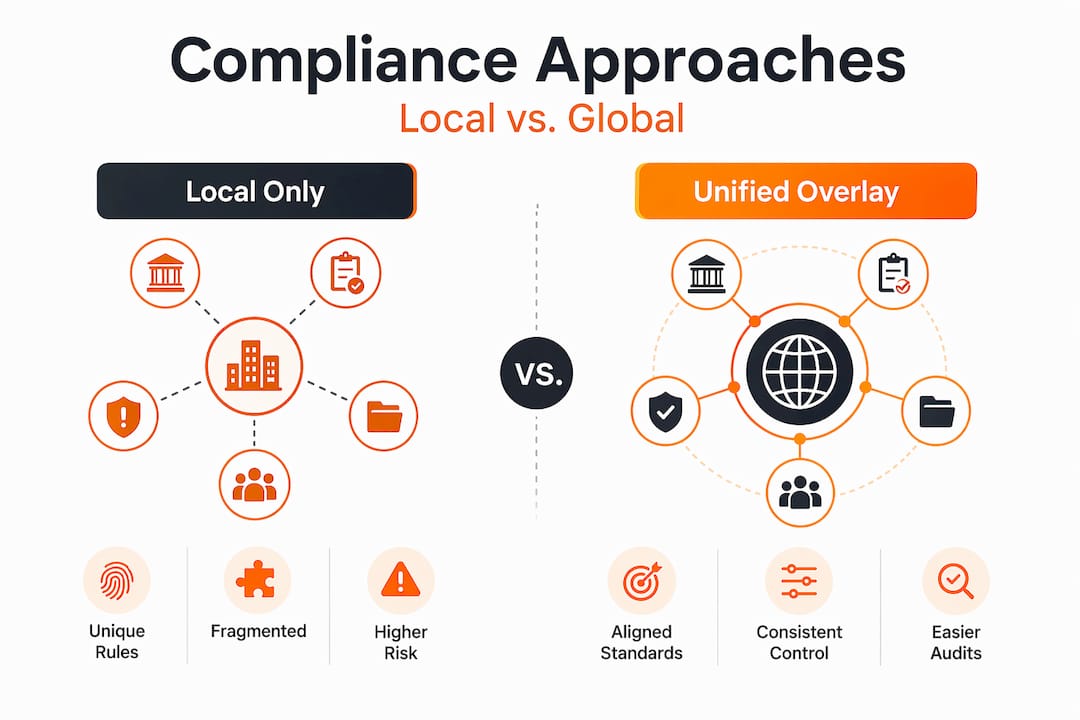

Fragmented adoption of frameworks across jurisdictions amplifies this challenge. Different regulators may adopt the same model regulation but interpret its requirements differently, enforce them on different timescales, and prioritise different operational areas during examinations. Insurers operating across multiple markets face genuine complexity in maintaining a consistent compliance posture without duplicating effort.

Where compliance programmes break down

Most compliance failures do not stem from wilful misconduct. Compliance failures typically arise from operational gaps and documentation errors, the kinds of breakdowns that occur when processes are poorly designed, teams are siloed, or responsibilities are unclear.

Here are the most common pitfalls practitioners encounter:

- Checklist mentality. Teams produce policies and procedure documents and consider the work complete. Regulators are not satisfied with documentation alone. They want to see that controls were actually executed, on time, by the right people, with evidence to prove it.

- Siloed ownership. Compliance is treated as a legal or compliance department function. When underwriting, claims, and IT do not understand their compliance obligations, gaps accumulate silently.

- Jurisdiction-specific blind spots. Assuming that compliance in one market transfers cleanly to another is a common and costly mistake. State-level or country-level variation can be significant, particularly in conduct-of-business and consumer protection rules.

- Inadequate evidence management. Regulators expect centralised, timestamped evidence during examinations. When evidence is scattered across spreadsheets, shared drives, and email chains, assembling a defensible audit trail becomes genuinely difficult, and gaps become visible.

- Reactive remediation. Problems surface during examinations rather than during internal testing cycles. By that point, the insurer is managing regulatory relationships under pressure rather than from a position of transparency.

Pro Tip: The most credible compliance programmes treat internal testing as a rehearsal for regulatory examination. If your team cannot produce timestamped evidence of control execution within 24 hours of a request, that is a gap worth fixing before a regulator finds it.

The cost of these failures extends beyond financial penalties. Regulatory findings consume significant management time, damage relationships with distribution partners, and can restrict product launches or market access. Reframing compliance as a performance capability rather than a cost centre changes how teams invest in it and what they build.

Building an effective compliance programme

Sustainable compliance does not come from adding more headcount to the compliance team. It comes from building a structured, documented, and continuously monitored operating model that distributes accountability across the organisation. Here is how to construct one that holds up.

Define your compliance architecture

Start with a clear inventory of your regulatory obligations across every market you operate in. Map each obligation to the business process it affects, the control that addresses it, the owner of that control, and the evidence that demonstrates execution. This mapping exercise surfaces gaps that checklists miss and creates the foundation for ongoing monitoring.

Apply a repeatable overlay method

For insurers operating across multiple jurisdictions, a repeatable overlay approach is the practical solution to fragmented regulation. Build your core compliance framework around the most demanding standard in your markets, then document the jurisdiction-specific variations as overlays. This avoids duplicating effort while maintaining precision.

Invest in cross-functional compliance ownership

Compliance obligations that touch underwriting, claims, IT, and finance cannot be managed by a compliance team operating in isolation. Each function needs to understand its specific obligations, own the controls that address them, and participate in evidence collection. Regular cross-functional compliance forums, not just annual training sessions, make this work in practice.

| Approach | What it looks like | Outcome |

|---|---|---|

| Reactive, siloed compliance | Annual audits, legal team owns all compliance | Gaps surface during examination; high remediation cost |

| Structured operating model | Mapped controls, cross-functional owners, quarterly testing | Continuous readiness; examination-confident teams |

| Automated, integrated compliance | Real-time evidence collection, automated monitoring | Lowest operational burden; fastest audit response |

Pro Tip: When building cross-functional compliance ownership, tie compliance responsibilities into job descriptions and performance reviews. Accountability that exists only in a compliance manual is rarely acted upon.

Technology plays a growing role here. Compliance automation tools now support real-time evidence collection, automated control testing, and centralised audit trails that regulators can access directly. For insurers still managing compliance through spreadsheets, the operational case for investment is clear. The practical strategies for solving compliance challenges developed by teams that have made this transition consistently point to reduced examination findings and faster regulatory response times.

Key frameworks shaping compliance today

Understanding which regulations actually drive your workload is the foundation of effective prioritisation. Several frameworks are shaping compliance demands for insurers across markets right now.

| Framework | Scope | Key requirement |

|---|---|---|

| MAR (Annual Financial Reporting Model Regulation) | Insurers exceeding £500m gross written premium | Enterprise-wide internal controls covering underwriting, claims, IT, and finance |

| Solvency II (Europe) | All authorised European insurers | Capital adequacy, risk governance, and supervisory reporting |

| GDPR / data protection regulations | All insurers handling personal data in Europe | Lawful data processing, breach notification, and rights management |

| Conduct of business rules | Consumer-facing insurance products | Marketing accuracy, fair treatment, and complaints handling |

| CMS 2026 documentation rules | ACA agents and brokers | New verification and documentation standards for the 2027 plan year |

The Annual Financial Reporting Model Regulation (MAR) deserves particular attention. MAR applies to insurers exceeding certain premium thresholds and requires enterprise-wide internal controls that go well beyond financial reporting. Underwriting processes, claims management systems, IT access controls, and financial reporting all fall within scope. Teams that treat MAR as a finance function project consistently underestimate the work and face difficult timelines.

Early, cross-functional action on MAR reduces examination risk significantly. That means scoping the full enterprise impact in the first quarter of a compliance cycle, assigning cross-functional owners, beginning control testing early, and maintaining a live remediation tracker rather than addressing issues in a final sprint.

Separately, CMS 2026 rule updates tighten documentation and marketing standards for insurance agents and brokers, with new requirements applying from the 2027 plan year. Insurers distributing through intermediary channels need to build these requirements into their distribution compliance frameworks now, before distribution partners are caught unprepared.

Early coordination with regulators before formal enforcement actions offer far better risk mitigation outcomes than waiting for scrutiny to arrive. Where there is genuine uncertainty about how a requirement applies, proactive engagement tends to generate clearer guidance and goodwill.

What is changing in insurance compliance

The direction of travel in regulatory compliance across the insurance industry is unmistakable. Regulators are moving away from periodic snapshot reviews towards expectations of continuous operational readiness. That shift has real implications for how compliance programmes are resourced and structured.

Several trends are worth tracking closely:

- Compliance-as-a-service adoption. The move towards automated compliance tools that provide real-time evidence collection and continuous monitoring is accelerating. Insurers using these platforms report faster audit preparation and fewer examination findings.

- Cyber security compliance integration. Data breaches and IT control failures are now a primary focus for regulators, not a secondary concern. Cyber security obligations are being folded into mainstream compliance frameworks rather than managed as a separate workstream.

- Digital transformation and compliance alignment. Cloud adoption in insurance brings genuine compliance benefits, including better system access controls, automated logging, and audit-ready architectures, but only when implementation is done with regulatory requirements in mind from the outset.

- Compliance as enterprise risk management. Leading insurers are integrating compliance monitoring into their broader enterprise risk frameworks. Compliance findings feed risk registers. Risk assessments inform compliance prioritisation. The two disciplines operate as one.

The insurers best positioned for 2026 and beyond are those that have stopped treating compliance as a project and started treating it as a permanent operating capability.

My perspective on compliance as a business capability

In my experience working with insurers across different markets, the most persistent misconception I encounter is that compliance is fundamentally a legal function, something to be managed at arm’s length from the people actually running the business.

What I have seen is the opposite. The insurers that perform best under regulatory scrutiny are those where compliance is owned at the operational level. Underwriters understand their filing obligations. Claims handlers know the documentation standards they are expected to meet. IT teams build audit trails into systems by default, not as an afterthought. That kind of embedded ownership cannot be mandated from a compliance department. It has to be built through sustained cross-functional engagement.

The other thing I would push back on is the idea that investment in compliance is purely a cost. When you have real-time evidence of control execution, clean audit trails, and documented remediation, you are also building the operational transparency that improves governance, reduces operational risk, and builds confidence with distribution partners and senior management. That is not a cost. It is infrastructure.

What I have learned, sometimes the hard way, is that the worst time to discover a compliance gap is during an examination. Build internal testing cycles that are rigorous enough to surface problems first, and treat every finding as an opportunity to improve the operating model rather than a crisis to contain.

— Tuna

How IBSuite supports compliance-driven insurers

For insurers where claims management is a critical compliance touchpoint, the right platform makes a measurable difference. IBSuite by Ibapplications is built with regulatory compliance requirements integrated throughout, including full audit trail capture, timestamped evidence of control execution, and structured documentation that holds up under examination.

The IBSuite claims management platform supports the kind of continuous operational readiness that regulators now expect, giving compliance officers visibility into claims handling practices in real time rather than retrospectively. For teams working through the compliance challenges common to insurers building or modernising core systems, IBSuite’s cloud-native architecture means compliance capabilities are built in, not bolted on. To see how it works in practice, you can book a demonstration with the Ibapplications team.

FAQ

What does regulatory compliance in insurance actually involve?

Regulatory compliance in insurance covers the full range of legal, financial, and operational obligations insurers must meet, including licensing, financial reporting, consumer protection standards, claims handling rules, and data governance. It applies across all business functions, not just finance or legal.

Why do insurance compliance programmes fail?

Most failures stem from operational gaps rather than intent. Compliance failures arise when controls exist on paper but are not executed and evidenced in practice, leaving insurers unable to demonstrate compliance during regulatory examinations.

What is the MAR regulation and who does it apply to?

The Annual Financial Reporting Model Regulation (MAR) applies to insurers exceeding certain premium thresholds and requires enterprise-wide internal controls across underwriting, claims, IT, and finance. It is not solely a finance regulation, and teams that treat it as one tend to underestimate its scope.

How can insurers manage compliance across multiple jurisdictions?

A repeatable overlay method is the most practical approach. Build your compliance framework around the most demanding standard in your markets, then document jurisdiction-specific variations as structured overlays to avoid duplicating effort while maintaining precision across each market.

What is compliance-as-a-service in insurance?

Compliance-as-a-service refers to automated platforms that provide continuous evidence collection and real-time monitoring of control execution. These tools replace periodic manual audits with ongoing compliance visibility, reducing examination risk and operational burden for insurers.

Recommended

- Solving insurance compliance challenges: 5 proven strategies

- Embracing Compliance through Next-Generation Insurance Platforms – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Cloud Security and Compliance for Insurers: Navigating 2025 Risks – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Understanding Insurance Compliance Automation Explained – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System