15.02.24

The benefits of a multi-core strategy for insurers

Core system modernization has picked up in the last few years for technical and economic reasons. Increased digital transformation has led insurers to create numerous apps and integrations which surface legacy constraints such as Data consistency, stability, performance, and speed to delivery. Improvement on the front end alone is not enough to implement new technologies and cater to consumers’ expectations. Achieving the full benefits of digitalization requires real-time data access as well as agile feature development in core systems. To enable this vision, most insurers must substantially overhaul their core systems and, in conjunction, transform their overall business model. Mobile first user experience, switching covers on/off, IoT connectivity, and embedding solution in 3rd party channels and ecosystems will be configured more easily and rapidly in a modern core.

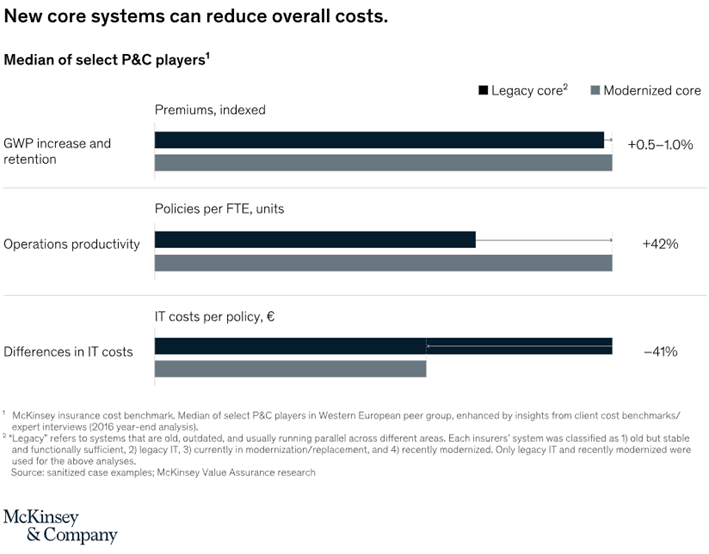

McKinsey assesses and explains the value of core system modernization in 3 areas[i] – see graph below:

Increased gross written premiums and reduced churn. Flexible, digitized product systems enable insurers to revamp their product innovation process, often resulting in a faster time to market for rate changes and new products. Likewise, digitally enabled integration capabilities can facilitate a more satisfying front-end user experience and increased support for agency and broker sales processes—a key driver of sales.

Increased operations productivity. The productivity benefits stretch beyond IT. Indeed, the disruption of introducing a new core system often motivates insurers to overhaul their operations setups and adapt workflow mechanisms, thereby improving work organization.

Reduced IT cost. Once implemented, modern IT systems can substantially reduce the cost of IT core systems by, for instance, running on commodity hardware versus the mainframe systems used today by many insurers. This last benefit will be maximized once the redundant older system is completely decommissioned.

The increased flexibility and real-time data exchange capability made possible by the implementation of a modernized core system may then be further leveraged in all processes of the insurance value chain with AI, ML, and RPA.

The potential value at stake explains why core system transformation is today a top priority of the insurance industry and should remain so for the next two to five years[ii].

The crucial question to consider when embarking on a core system modernization, a multi-year initiative, is what should I do with the core? Consolidate, rewrite, or wrap/extend an existing system or replace a system with best-of-breed COTS (commercial off-the-shelf) vendor solutions. The decision is generally based on priorities, risk appetite, investment budget, people/skill availability, vendor solution fit to its needs, time to market, IT estate, and organizational preparedness towards change. But insurers must build trade-off metrics and carefully pick the best transformation option that aligns with strategic priorities, plans, and risk appetite while not allowing organizational constraints to derail the project.

Each path to IT modernization has different pros and cons. In addition to choosing between the fundamental options described above, the timing and extent of existing policies of migration need to be considered. While many insurers develop a platform for both their existing and new business, some carriers opt to start with a greenfield implementation specifically for the new business that would provide an option to migrate the existing business later.

The latter also named The Land and Expand Approach by IBA, is becoming the most consensual amongst its insurance clients. As shown in the drawing below, this low-cost and low-risk approach consists in adding a new modern core system to launch a new digital offer that the older core could not handle.

A cloud-based solution, IBA’s IBSuite may be configured, implemented, and run alongside your existing core in as less as 5 months – see the drawing below. To allow for a quick time to market, the number of products and services configured in a first implementation is reduced as are the interfaces needed. By doing so, and with very little strain on his financial, technical, or human resources, an insurer may present a product or service to a consumer via any channel of his, of a partner, or via any marketplace or 3rd party ecosystem.

Once the first implementation of the new core is done and running smoothly, the organization may plan and roll out the new core-selected products, services, and applications that will most benefit from the capabilities of a modern system. Amongst these are top-notch functionalities related to Distribution, rating, product configuration, billing, policy admin, claims, and data insights – see the illustration below.

This hybrid design can gradually bring about valuable modernized core functions without compromising day-to-day activities. In the future, when the insurer wishes to switch out individual system components for more modern ones that will keep him on the leading edge, this approach will make it easy.

A hybrid, multi-core Innovation Platform was chosen by Klinc, a subsidiary of Zurich. This client of IBA wished to roll out a mobile-first digital experience to insure phones and other devices with advanced functionalities such as switching covers on and off usage-based and repair and replace. Their older system not permitting, Klinc opted for a greenfield project with IBA which allowed them to roll out their product to a great number of partners throughout Europe in 5 months, through a multicore strategy.

Modernizing insurance core systems is imperative to achieve the full benefits of digital transformation and, eventually, sustain an insurer’s activity. Given the digital advances in insurance—especially in personal lines—transforming the core is the next frontier. How it is done, and the choice of a new core will bind those involved. An approach that is gaining consensus and that is less disruptive is the multicore strategy. Adopting a new core alongside a legacy system permits an insurer to reap the benefits of new technology for selected applications and projects. It is a low-cost approach that limits the risk to the business and allows a gradual, as-needed basis, modernization of the technological stack of the company.

[i] In: https://www.mckinsey.com/industries/financial-services/our-insights/it-modernization-in-insurance-three-paths-to-transformation

[ii] In: https://www.mindtree.com/insights/resources/core-systems-transformation-7-modernization-best-practices