24.06.26

Insurance decision-making guide for P&C professionals

An insurance decision-making guide is the authoritative framework that enables professionals to choose and optimise coverage efficiently, balancing risk exposure against cost. For property and casualty insurers and their clients, the stakes are high: a poorly structured portfolio leaves catastrophic risks uncovered while wasting budget on trivial ones. This guide applies the core principles of risk management, coverage adequacy, and claims evaluation to give decision-makers a structured approach. Platforms like IBSuite support this process by integrating data across the full policy lifecycle, from underwriting to claims settlement.

What types of insurance should decision-makers prioritise?

Most professionals require four foundational insurance types: health, auto, home or renters, and life insurance. These four categories cover the majority of serious financial risks a person or business faces. Situational policies such as disability and umbrella liability extend that protection for specific risk profiles.

The logic behind this prioritisation is straightforward. Insurance exists to protect against losses that would be financially catastrophic, not to cover every minor inconvenience. Over-insuring small risks while under-insuring large ones is the fastest route to a coverage gap that matters precisely when it should not.

Here is how the four core categories compare in terms of purpose and priority:

| Insurance type | Primary risk covered | Priority trigger |

|---|---|---|

| Health | Medical costs and hospitalisation | Universal; highest financial exposure |

| Auto | Liability and vehicle damage | Required by law; asset protection |

| Home or renters | Property loss and liability | Asset or contents protection |

| Life | Income replacement for dependants | Critical for those with financial dependants |

Beyond the core four, two categories deserve attention from decision-makers with specific exposures:

- Disability insurance replaces income if illness or injury prevents work. Most professionals underestimate this risk relative to life insurance.

- Umbrella liability extends coverage beyond standard auto and home limits. It is particularly relevant for high-net-worth individuals or businesses with public-facing operations.

A common misprioritisation is purchasing extended warranties or low-value gadget cover while carrying inadequate liability limits. Financial advisors recommend auto liability coverage of at least £100,000 per person and £300,000 per accident. State or national minimums are often far below that threshold and leave significant asset exposure.

How to evaluate insurance policies beyond price

Price is the wrong starting point for policy selection. The primary mistake decision-makers make is shopping by premium rather than by coverage adequacy tailored to their specific risk profile and assets. A cheaper policy that fails at the point of claim delivers negative value.

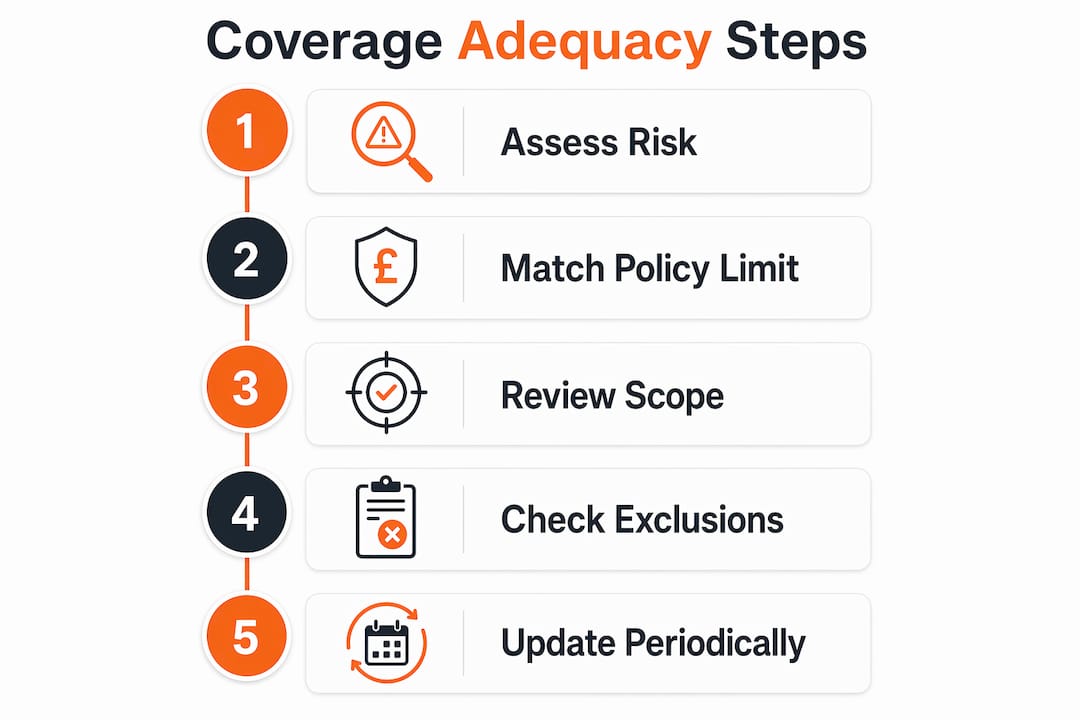

Coverage adequacy

Coverage adequacy means the policy limit and scope match the actual financial risk being protected. A home insured for its purchase price rather than its rebuild cost is underinsured. An auto policy at the legal minimum leaves personal assets exposed in a serious accident. Decision-makers should map their largest potential losses first, then confirm coverage limits exceed those figures.

Health insurance adds another layer of complexity. Plan types such as HMO, PPO, EPO, and POS differ significantly in network restrictions and specialist access. A PPO offers greater flexibility but carries higher premiums. An HMO reduces cost but requires referrals for specialist care. The right choice depends on how frequently the insured accesses specialist services.

Claims process assessment

A policy’s real value only becomes visible at the point of a claim. Insurers with proven fast and fair settlement records add measurable value beyond what the premium figure suggests. Decision-makers should review verified claims satisfaction data and check whether the insurer has a reputation for disputing legitimate claims.

The evaluation framework for any policy should cover these criteria:

- Coverage limits: Do they exceed your maximum probable loss?

- Exclusions: What specific scenarios does the policy not cover?

- Claims reputation: What do verified reviews say about settlement speed and fairness?

- Network or provider access: For health plans, does the network include your preferred providers?

- Renewal terms: Can the insurer change terms or premiums significantly at renewal?

Pro Tip: Request a sample claims scenario from any prospective insurer. Ask them to walk through exactly how a specific loss event would be handled, including timelines and documentation requirements. Their answer reveals more than any brochure.

Understanding how modern claims processes work at a platform level also helps decision-makers set realistic expectations and identify insurers whose operations match their standards.

Understanding total cost of ownership in insurance

Total cost of ownership is the correct metric for comparing insurance plans. It includes premiums, deductibles, co-pays, coinsurance, and expected utilisation costs. Calculating true plan cost beyond the advertised premium often reverses the apparent ranking of options.

The core trade-off is between low-premium, high-deductible plans and high-premium, low-deductible plans. The right choice depends on expected utilisation:

- Low utilisation scenario: A high-deductible plan saves money annually because the lower premium outweighs the higher deductible you rarely trigger.

- High utilisation scenario: A low-deductible plan reduces out-of-pocket exposure when you access services frequently, making the higher premium worthwhile.

- Chronic condition scenario: High-deductible plans can be worse for those with ongoing medical needs. The deductible resets annually, creating repeated high costs.

- Emergency fund consideration: A high-deductible plan only works if you hold sufficient liquid reserves to cover the deductible without financial strain.

Employers typically cover 70–80% of health insurance premiums. That figure sounds generous, but out-of-pocket maxima can make the actual annual cost significantly higher in years with heavy utilisation. Decision-makers should model both a low-use and a high-use year before selecting a plan.

The practical rule is this: never select a deductible level higher than the amount you can fund from savings within 30 days. A plan that looks efficient on paper becomes a liability if a claim forces you into debt to meet the deductible.

How to integrate risk assessment and portfolio reviews

Insurance portfolios require active management, not a one-time purchase decision. An annual audit is the minimum standard for maintaining coverage that fits current circumstances. A policy that was appropriate 12 months ago may now be over-priced, under-scoped, or simply misaligned with a changed risk profile.

The triggers that mandate an immediate review include:

- A significant change in income or assets

- Marriage, divorce, or the birth of a dependant

- Purchase or sale of property

- A new business venture or change in professional liability exposure

- Retirement or a major shift in employment status

Personalised risk profiling is the foundation of good portfolio management. Generic coverage recommendations ignore the specific combination of assets, liabilities, health status, and dependants that define each individual or organisation’s actual exposure. A freelance consultant and a manufacturing business may both need liability cover, but the limits, exclusions, and policy structures differ substantially.

| Review trigger | Action required |

|---|---|

| Income increase | Raise life and disability cover to match new earnings |

| New property | Add or update home or contents insurance |

| New dependant | Review life insurance sum assured |

| Business change | Reassess professional and public liability limits |

| Annual renewal | Compare market alternatives and check for coverage gaps |

Bundling policies with a single insurer often reduces total premium cost and simplifies administration. The trade-off is reduced flexibility to switch individual lines. Decision-makers should model the bundled discount against the cost of best-in-class individual policies before committing.

Pro Tip: Use a structured insurance portfolio review at each annual renewal. Map every active policy against your current risk profile and flag any coverage that no longer matches a real exposure.

Platform-based management tools, such as IBSuite, consolidate policy data, claims history, and renewal dates in one place. That visibility makes it far easier to identify gaps, duplications, and inefficiencies across a portfolio.

Key takeaways

Effective insurance decisions require matching coverage to actual risk, not selecting the lowest premium available.

| Point | Details |

|---|---|

| Prioritise the core four | Health, auto, home or renters, and life insurance cover the majority of serious financial risks. |

| Evaluate beyond price | Assess coverage limits, exclusions, claims reputation, and network access before selecting any policy. |

| Calculate total cost of ownership | Include premiums, deductibles, co-pays, and expected utilisation to compare plans accurately. |

| Conduct annual portfolio reviews | Life changes invalidate existing coverage; review at every major life event and at each renewal. |

| Match deductibles to liquid reserves | Never set a deductible higher than the amount you can fund from savings within 30 days. |

Where most professionals get this wrong

The single most common error I see is treating insurance as a commodity purchase. Decision-makers compare headline premiums, select the cheapest option, and move on. That approach works until it does not, and when it fails, it fails at the worst possible moment.

The second error is the inverse: over-insuring trivial risks. Extended warranties, low-value gadget cover, and travel insurance for non-refundable costs below a few hundred pounds consume budget that should protect against genuinely catastrophic exposure. Insurance functions as leverage against large losses, not a maintenance contract for small ones.

What actually works is a disciplined framework applied consistently. Map your largest potential losses. Confirm your coverage limits exceed those figures. Check the insurer’s claims record with the same rigour you apply to the premium. Then review the whole picture every year. The professionals who do this well treat their insurance portfolio the same way they treat any other financial asset: with regular attention and a clear decision rationale.

Digital platforms have made this process significantly more manageable. Tools that consolidate policy data, automate renewal alerts, and surface claims automation insights reduce the administrative burden of active portfolio management. The result is better decisions made faster, with fewer gaps.

— Tuna

How IBSuite supports smarter insurance decisions

Ibapplications builds IBSuite specifically for property and casualty insurers who need full visibility across their policy and claims operations. The platform covers the complete insurance value chain, from underwriting and rating through to claims settlement and financial reporting. That end-to-end view is precisely what decision-makers need to manage portfolios with confidence rather than guesswork.

For professionals evaluating their own technology infrastructure, the IBSuite insurance platform offers API-first integration, Evergreen updates, and AWS-hosted security. It reduces IT complexity while enabling faster product launches and better claims outcomes. Ibapplications has supported insurers in this way since 2010, and the platform continues to evolve alongside regulatory and market demands.

FAQ

What are the four essential types of insurance?

Health, auto, home or renters, and life insurance cover the majority of serious financial risks. Most individuals and businesses should hold all four before considering additional policies.

Why is the claims process as important as the premium?

A policy’s value is only realised at the point of a claim. Insurers with poor claims reputations may delay or dispute legitimate settlements, making a cheaper premium a false economy.

What is total cost of ownership in insurance?

Total cost of ownership includes all premiums, deductibles, co-pays, and coinsurance across a policy year. It reveals the true cost of a plan beyond the advertised premium figure.

How often should an insurance portfolio be reviewed?

An annual review is the minimum standard. Any significant life event, such as a change in income, a new dependant, or a property purchase, should trigger an immediate reassessment.

What is the biggest mistake in insurance selection?

Prioritising price over coverage adequacy is the most common error. The best policy matches coverage limits and exclusions to your specific risk profile, not simply the lowest available premium.

Recommended

- Insurance Claims Automation: Complete Overview for P&C Insurers – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Optimizing Cloud Insurance Platforms for P&C Success

- Effective insurance CRM: a step-by-step guide for P&C leaders

- Insurance Risk Management Explained: Best Practices – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System