14.04.26

Future-proofing insurance systems for resilience and growth

TL;DR:

- Future-proofing insurance systems is a continuous strategic discipline involving technology, culture, processes, and governance.

- Modern, flexible systems with modular architecture, open APIs, and cloud scalability enable faster innovation and compliance.

- Organizational agility and mindset change are crucial for lasting resilience beyond just technological upgrades.

Legacy insurance systems can become liabilities almost overnight. A regulatory change, a cyber incident, or a shift in customer expectations can expose the cracks in ageing platforms faster than most executives anticipate. Many insurance leaders still treat future-proofing as a technology refresh cycle, something to revisit every few years when budgets allow. That framing is dangerously narrow. Real future-proofing is a continuous strategic discipline that touches technology, culture, processes, and governance simultaneously. This guide gives you a structured, actionable roadmap to build genuine resilience into your core systems and position your organisation for sustainable growth.

Table of Contents

- Why future-proofing insurance systems matters

- What it means to future-proof insurance systems

- Common barriers to future-proofing and how to overcome them

- Technology strategies for resilient insurance systems

- Immediate steps to future-proof your insurance systems

- A different perspective: What most insurers miss about future-proofing

- Next steps: Explore future-proof systems with IBSuite

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start with a strategy | Have a clear, board-level future-proofing vision before investing in technology. |

| Address technology and culture | Modernisation succeeds when technical upgrades and organisational buy-in go hand in hand. |

| Leverage cloud and automation | Cloud migration and AI adoption dramatically boost agility and resilience. |

| Prioritise modularity | Modular systems make future upgrades, compliance, and innovation much easier and faster. |

Why future-proofing insurance systems matters

The pressure on P&C insurers is not easing. Regulatory requirements are tightening across every major market, climate-related claims volatility is rising, and customers now expect digital-first experiences that many legacy platforms simply cannot support. The digital transformation drivers shaping the industry are accelerating, and insurers that delay adaptation risk falling behind competitors who are already launching products in weeks rather than months.

Legacy systems carry a compounding cost that rarely appears clearly on a balance sheet. There is the direct cost of maintaining outdated infrastructure, the indirect cost of slower product launches, and the strategic cost of being unable to respond to market disruption. Together, these create a risk profile that should concern any board.

Consider what is at stake:

- Compliance exposure: Older systems struggle to adapt to new regulatory frameworks quickly, creating audit risk and potential fines.

- Cyber vulnerability: Unpatched legacy platforms are prime targets. Insurers hold vast quantities of sensitive personal and financial data, making them high-value targets.

- Innovation lag: When your core platform cannot support new products or distribution channels, competitors fill that gap.

- Talent drain: Skilled engineers and data professionals do not want to work on outdated technology stacks.

“The pace of digital disruption in the insurance industry is accelerating, requiring faster adaptation.” This is not a distant forecast. It is the operating reality for every P&C insurer right now.

The importance of modernising systems extends beyond operational efficiency. It is a board-level strategic priority with a measurable return on investment. Insurers that modernise core platforms report faster time-to-market, lower IT maintenance costs, and improved customer retention. Future-proofing is not a cost centre. It is a growth enabler.

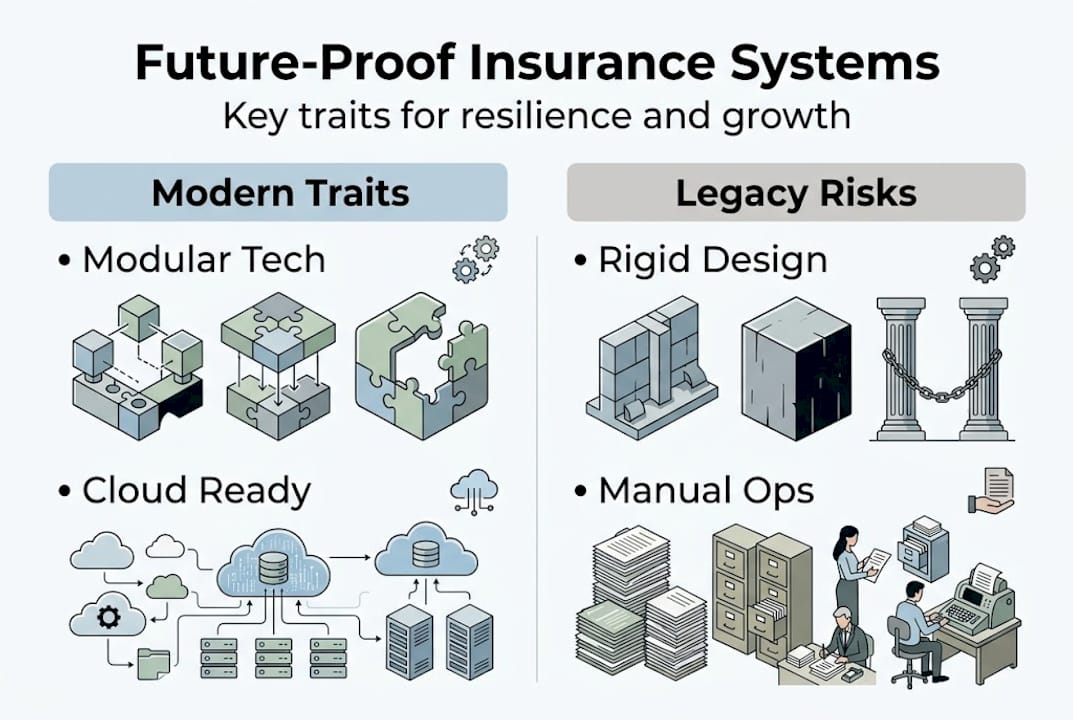

What it means to future-proof insurance systems

Future-proofing is not simply replacing old software with new software. It is designing your systems and operating model so that change, whether regulatory, technological, or market-driven, does not break your business. It means building for adaptability rather than stability alone.

Successful digitising insurance processes demands system flexibility, interoperability, and scalability for evolving demands. That translates into several concrete capabilities:

- Modularity: Core functions such as policy administration, claims, billing, and rating should operate as independent modules that can be updated without disrupting the whole system.

- API-first integration: Open APIs allow you to connect new partners, insurtech tools, and data sources without expensive custom builds.

- Automation readiness: Workflows should be designed to accept automation at any point, not retrofitted later.

- Regulatory adaptability: Compliance updates should be configurable, not hard-coded changes requiring lengthy development cycles.

| Desirable system characteristic | Legacy system weakness |

|---|---|

| Modular, loosely coupled architecture | Monolithic, tightly coupled codebase |

| Open API integration layer | Proprietary, closed integration points |

| Cloud-native scalability | On-premise with fixed capacity |

| Configurable compliance rules | Hard-coded regulatory logic |

| Real-time data access | Batch processing with data lag |

The table above illustrates why legacy platforms create compounding friction. Each weakness compounds the others, making even small changes expensive and slow.

Flexibility also matters for product and channel innovation. Insurers that can launch a new parametric product or activate a new distribution partner in days rather than quarters hold a genuine competitive advantage. Cloud scalability fundamentals are central to achieving that speed.

Pro Tip: When evaluating platforms, test them against your future business model, not just your current one. Ask vendors to demonstrate how their system handles a product line you do not yet offer.

Common barriers to future-proofing and how to overcome them

Knowing what future-proofing requires is one thing. Actually executing it inside a live insurance organisation is another challenge entirely. Organisational inertia and technical debt delay critical transformation, and they do so in ways that are often invisible until the cost becomes acute.

| Barrier | Practical solution |

|---|---|

| Technical debt accumulation | Prioritise modular replacement over full rip-and-replace |

| Legacy culture and risk aversion | Build internal transformation champions at every level |

| Resource and budget constraints | Use phased delivery to demonstrate ROI early |

| Fragmented data across silos | Invest in a unified data layer before migrating core systems |

Overcoming these barriers requires a sequenced approach. Here is a practical order of operations:

- Audit your technical debt honestly. Map every system, integration, and manual workaround. You cannot fix what you have not measured.

- Identify your transformation champions. Find leaders across underwriting, claims, IT, and finance who are motivated to drive change. They become your internal coalition.

- Tackle data fragmentation first. Unified, clean data is the foundation for automation, analytics, and compliance. Without it, new platforms underperform.

- Use change management principles to address cultural resistance. Training, communication, and visible leadership support are not optional extras.

- Pilot before you scale. Run a controlled modernisation project in one business unit or product line before committing to enterprise-wide rollout.

Resource constraints are real, but they are rarely the actual blocker. The deeper issue is usually a lack of confidence that transformation will deliver results. Early wins, even small ones, change that narrative quickly.

Pro Tip: Appoint a dedicated transformation lead who reports directly to the executive team. Transformation projects that sit inside IT departments alone rarely gain the cross-functional momentum they need.

Technology strategies for resilient insurance systems

The right technology choices compound your resilience over time. The wrong ones lock you into the same problems you are trying to escape. Cloud-first and automation-driven architectures enable resilience and faster innovation cycles, and they are now the baseline expectation rather than a differentiator.

Here are the technology pivots that matter most in 2026:

- Cloud-native platforms: Moving to cloud-native infrastructure eliminates the capacity constraints and patching burdens of on-premise systems. It also enables the elastic scaling that modern insurance volumes demand.

- AI and advanced analytics: Predictive underwriting, claims fraud detection, and customer churn modelling are no longer experimental. They are operational tools that improve margins and customer outcomes.

- Interchangeable microservices: Replacing monolithic systems with microservices means you can swap out individual components, such as your rating engine or billing module, without touching the rest of the platform.

- Automated compliance monitoring: Regulatory change management should be a system capability, not a manual process. Configurable rules engines reduce compliance risk significantly.

- Real-time data pipelines: Batch processing is a legacy constraint. Real-time data access enables faster decisions across underwriting, claims, and customer service.

Cybersecurity best practices are a non-negotiable component of any resilience strategy. Strong cybersecurity is a future-proofing must amid increased digitalisation and threats. As you add new integrations, APIs, and cloud services, your attack surface grows. Governance frameworks, third-party risk controls, and continuous security monitoring must scale in parallel with your technology estate.

Pro Tip: Ensure your security posture review happens at the same cadence as your technology roadmap review. Security that lags behind your architecture creates gaps that are expensive to close retrospectively.

Immediate steps to future-proof your insurance systems

Strategy without execution is just planning. Here is a concrete sequence of actions you can begin within the next 12 months to build measurable momentum.

- Form a cross-functional future-proofing task force with representation from IT, underwriting, claims, compliance, and finance. Give it executive sponsorship and a clear mandate.

- Conduct a system gap assessment that maps current capabilities against the characteristics in the table above. Prioritise gaps by business impact and remediation cost.

- Modularise one core process as a proof of concept. Claims intake or policy endorsements are strong candidates because they have clear inputs, outputs, and measurable cycle times.

- Launch a pilot project using your chosen modern platform in a contained environment. Measure speed, accuracy, and staff adoption carefully.

- Report results to the board within 90 days of the pilot launch. Use real data to build the case for broader investment.

A transformation roadmap for P&C insurance built on phased delivery secures leadership buy-in faster because it demonstrates value before asking for full commitment. Insurers that follow a phased approach consistently report faster results and stronger stakeholder confidence than those attempting big-bang transformations.

The task force structure is particularly important. Future-proofing decisions that sit inside a single department tend to optimise for that department’s constraints rather than the organisation’s strategic needs. Cross-functional ownership changes that dynamic fundamentally.

A different perspective: What most insurers miss about future-proofing

Most future-proofing conversations in insurance boardrooms focus almost entirely on platforms, vendors, and migration timelines. That focus is understandable but incomplete. The insurers that achieve lasting resilience are not simply the ones with the most modern technology stack. They are the ones that have built organisations capable of absorbing and exploiting change continuously.

Real resilience is cultural, not only technological.

A new platform deployed into an organisation with rigid processes and change-averse teams will underperform its potential every time. Operational agility and mindset change are as fundamental to lasting transformation as any architectural decision. Lasting transformation requires both tech reinvention and organisational mindset change.

The insurers we see succeed long-term invest in learning infrastructure alongside technology infrastructure. They run regular retrospectives on transformation projects, they share lessons across business units, and they reward experimentation rather than punishing failure. That kind of organisational learning is what converts a technology investment into a durable competitive advantage.

Next steps: Explore future-proof systems with IBSuite

If this roadmap has highlighted gaps in your current systems, IBSuite is built to address them directly. IBSuite is IBA’s cloud-native, API-first platform covering the full P&C insurance value chain, from policy administration solutions and claims management platform through to billing, rating, and CRM. It is designed for the kind of modularity, scalability, and compliance adaptability that future-proofing demands. Evergreen updates mean you stay current without disruptive upgrade cycles. If you are ready to see how IBSuite can strengthen your resilience, book a demo and speak with our team.

Frequently asked questions

What is the first step towards future-proofing insurance systems?

The first step is to assess current system gaps and assemble a cross-functional team to drive the modernisation agenda. A phased approach delivers results faster and secures leadership buy-in.

How can cloud migration support insurance system resilience?

Cloud migration increases scalability, agility, and security, reducing costs and improving the ability to respond to market demands. Cloud-first architectures enable resilience and faster innovation cycles.

What role does culture play in future-proofing?

A future-ready culture encourages change acceptance and ensures technology upgrades deliver long-term value. Lasting transformation requires both tech reinvention and organisational mindset change.

Are modular systems essential for modern insurers?

Yes, modular systems allow easier updates and innovation, adapting quickly to regulation and market shifts. System flexibility and interoperability are fundamental requirements for future-proofing.

What are some quick wins in insurance system modernisation?

Digitising key customer interactions and automating manual tasks can deliver measurable value within months. The pace of digital disruption means early movers gain compounding advantages over time.

Recommended

- Future-Proofing Insurance: 4 Key Strategies for Core System Modernization and Optimization – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Why Modernizing Insurance Systems is Crucial for Growth – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Modern Insurance Platform Benefits – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Modern Insurance Platforms: What to look for – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Business Insurance Types: Protect Your South African SME – Ready Accounting