08.01.26

Embedded Insurance: Transforming P&C Distribution Models

Traditional insurance channels are being reshaped as embedded insurance surges, now accounting for over 18 percent of new premiums in some Central European markets. For property and casualty executives, this shift presents both a strategic opportunity and a complex challenge as consumers compare integrated experiences from British insurtech leaders with local offerings. This article provides practical insights on core concepts, technology, and compliance essentials to help executives create seamless, customer-centric solutions that meet rising expectations.

Table of Contents

- Embedded Insurance Defined And Core Concepts

- Distribution Models And Key Variations

- Real-World Use Cases In Central Europe

- Technology Integration With Core Platforms

- Legal And Compliance Requirements For Insurers

- Risks, Costs, And Implementation Challenges

Key Takeaways

| Point | Details |

|---|---|

| Embedded Insurance Enhances Accessibility | Embedded insurance allows consumers to obtain coverage directly at the point of purchase, streamlining the buying process and minimising complexity. |

| Technological Infrastructure is Crucial | Insurers must adopt modern API-driven and microservices architectures to support seamless integration and facilitate rapid product innovation. |

| Navigating Regulatory Frameworks is Essential | Providers must be aware of diverse regulatory requirements across different European markets to ensure compliance and protect consumer interests. |

| Risk Management is a Top Priority | Developing robust risk assessment frameworks is necessary to address operational risks and adapt to the dynamics of embedded insurance models. |

Embedded Insurance Defined And Core Concepts

Embedded insurance represents a transformative approach to traditional insurance distribution, where insurance products are seamlessly integrated directly into the purchase of other goods or services. Regulatory frameworks in Europe underscore this model as a regulated insurance contract subject to specific licensing requirements.

At its core, embedded insurance fundamentally reimagines how consumers acquire insurance protection. Rather than purchasing coverage through separate, standalone transactions, consumers can now obtain insurance precisely when and where they need it – during the purchase of related products or services. This approach eliminates friction, reduces complexity, and provides more contextually relevant protection. Typical examples include insurance automatically included with credit card purchases, vehicle acquisitions, or bicycle rentals.

The European insurance ecosystem is rapidly evolving to embrace these innovative distribution models. Digital platforms are enabling micro-insurance offerings that can be instantly activated, creating unprecedented convenience for consumers. Insurance providers are developing strategic partnerships across diverse industry sectors to create seamless, integrated protection experiences that align closely with customer purchasing journeys.

Pro tip: When exploring embedded insurance strategies, focus on creating frictionless user experiences that add genuine value to the customer’s original transaction.

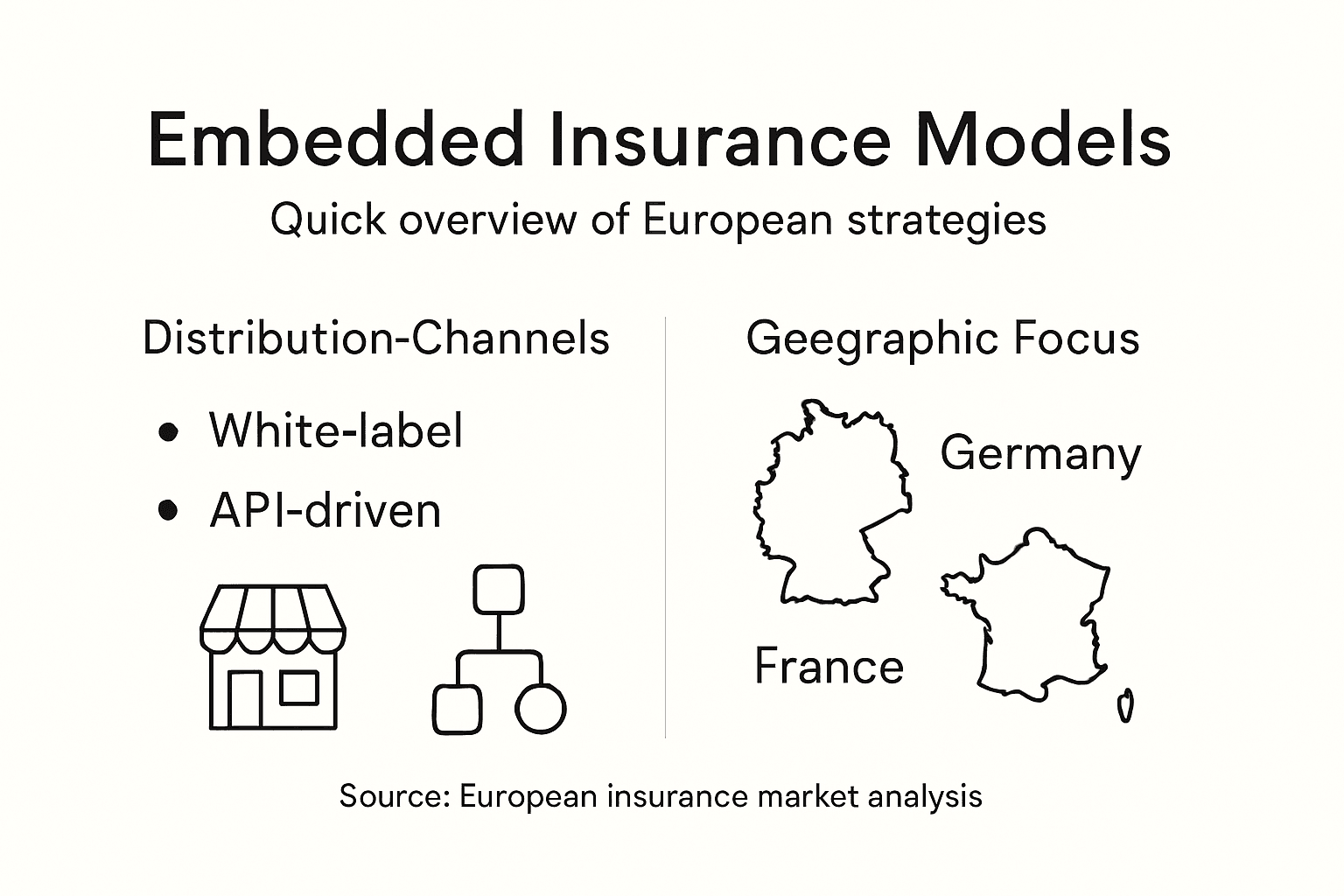

Distribution Models And Key Variations

The European embedded insurance landscape showcases multiple sophisticated distribution channels and models that are transforming traditional insurance approaches. These models range from digital API-driven platforms to strategic offline integrations, with online channels increasingly dominating market penetration across key European markets.

Distribution channels can be categorised into several primary variations. White-label solutions represent one prominent approach, where insurers provide coverage that can be branded and integrated seamlessly by partner organisations. Fintech partnerships offer another dynamic model, enabling technology platforms to embed insurance products directly into their financial service offerings. Direct integration models – particularly prevalent in e-commerce and mobility sectors – allow insurance to be activated instantly during product or service purchases.

Geographic variations play a significant role in distribution strategy. Countries like Germany, the United Kingdom, France, and the Netherlands demonstrate nuanced approaches to embedded insurance implementation. These markets exhibit unique regulatory environments, consumer expectations, and technological infrastructures that influence how embedded insurance products are designed, marketed, and distributed. Digital platforms have become critical enablers, facilitating micro-insurance offerings that can be activated with unprecedented speed and convenience.

Pro tip: When developing embedded insurance distribution strategies, prioritise understanding local market dynamics and creating frictionless integration experiences that add genuine value for both partners and consumers.

This table compares common embedded insurance distribution models in Europe:

| Model Type | Example Sector | Implementation Speed | Integration Complexity |

|---|---|---|---|

| White-label | Retail/e-commerce | Moderate | Medium |

| Fintech Platform | Banking/fintech | Fast | Medium |

| Direct Integration | Mobility/travel | Very fast | High |

Real-World Use Cases In Central Europe

The Central European embedded insurance market is witnessing transformative innovations driven by strategic insurtech partnerships that leverage advanced technological ecosystems. Insurers are developing sophisticated integration strategies targeting high-potential market segments such as electronics, mobility, and consumer goods, with a focused approach on creating seamless, contextually relevant protection experiences.

In Germany, Austria, and France, embedded insurance solutions are demonstrating remarkable adaptability. Specific use cases include smartphone purchase protection integrated directly at point of sale, travel insurance activated through mobility platforms, and electronic device coverage bundled with retail purchases. These implementations showcase how embedded insurance can transform traditional risk protection by making coverage more accessible, immediate, and tailored to individual consumer needs.

Technological innovation plays a critical role in these implementations. Advanced API platforms enable real-time insurance activation, while sophisticated data analytics allow for hyper-personalised risk assessment. Insurers are creating ecosystem partnerships that extend beyond traditional boundaries, collaborating with e-commerce platforms, mobile service providers, and consumer electronics retailers to deliver integrated insurance solutions that feel natural and intuitive to modern consumers.

Pro tip: Focus on creating embedded insurance products that solve genuine consumer pain points rather than simply adding another layer of complexity to purchasing decisions.

Technology Integration With Core Platforms

Insurers are rapidly transforming their technological infrastructure to support advanced embedded insurance frameworks, recognising that modern distribution models demand sophisticated, flexible core systems. The integration process requires a comprehensive approach that goes beyond simple software upgrades, involving fundamental reimagining of technological architectures to enable seamless, real-time insurance product delivery.

API-driven architectures represent the cornerstone of successful technology integration. These sophisticated platforms enable dynamic underwriting, instantaneous policy management, and frictionless claims processing by creating interconnected technological ecosystems. Microservices architecture allows insurers to develop modular, adaptable systems that can quickly respond to market changes, consumer needs, and emerging regulatory requirements. This approach enables rapid product innovation and supports the complex, multi-channel distribution models characteristic of embedded insurance.

The transition from legacy IT systems poses significant challenges for European insurers. Modernisation demands not just technological upgrades, but a cultural shift towards more agile, data-driven operational models. Advanced platforms must support complex integrations with e-commerce systems, mobility platforms, and consumer technology ecosystems. Real-time data flows, sophisticated risk assessment algorithms, and seamless digital experiences are no longer optional but fundamental requirements for competitive embedded insurance offerings.

Here is a summary of core embedded insurance technology features and their business impact:

| Technology Feature | Primary Function | Business Impact |

|---|---|---|

| API-driven architecture | Real-time product integration | Faster market launches, fewer errors |

| Microservices architecture | Modular, scalable infrastructure | Easier updates, improved resilience |

| Real-time data analytics | Dynamic risk assessment | More accurate pricing, reduced losses |

| Platform interoperability | Seamless partner ecosystem links | Wider distribution, better experience |

Pro tip: Prioritise building flexible, API-first technology infrastructures that can rapidly integrate with diverse partner ecosystems and support continuous innovation.

Legal And Compliance Requirements For Insurers

Embedded insurance providers must navigate a complex regulatory landscape, with specific compliance considerations governing insurance distribution across European markets. The Insurance Distribution Directive (IDD) establishes a comprehensive framework that mandates transparency, proper licensing, and stringent consumer protection standards for all parties involved in insurance product integration.

Regulatory oversight extends beyond traditional insurance distribution channels, requiring meticulous attention to licensing requirements for digital platforms and non-traditional insurance intermediaries. The Dutch market provides a compelling example, where the Authority for Financial Markets (AFM) has established nuanced guidelines distinguishing between licensed intermediaries and platform providers. These regulations demand rigorous risk management protocols, ensuring that embedded insurance products maintain consumer interests at their core, regardless of the distribution mechanism.

Cross-border embedded insurance offerings introduce additional complexity, necessitating careful navigation of national regulatory variations within the European Union. Providers must demonstrate comprehensive understanding of jurisdictional differences, particularly regarding product suitability, consumer protection, and data privacy requirements. This demands a sophisticated approach to compliance that goes beyond mere technical adherence, requiring genuine commitment to transparent, ethical insurance distribution practices that prioritise customer interests and maintain the integrity of the financial services ecosystem.

Pro tip: Develop a robust compliance framework that anticipates regulatory evolution, combining technological flexibility with proactive risk management strategies.

Risks, Costs, And Implementation Challenges

Embedded insurance models present complex challenges, with significant operational risks emerging from technological integration and multi-party ecosystems. Financial regulators increasingly highlight the potential vulnerabilities inherent in these innovative distribution approaches, emphasising the need for robust risk management strategies that can adapt to rapidly evolving digital insurance landscapes.

Implementation challenges extend across multiple dimensions, including technological infrastructure, regulatory compliance, and partnership management. Insurers must invest substantially in developing sophisticated API architectures capable of seamless integration with diverse partner platforms. These technological investments are compounded by complex compliance requirements, which demand meticulous monitoring of anti-money laundering protocols, consumer protection standards, and data privacy regulations across different jurisdictional boundaries.

The financial implications of embedded insurance implementation are substantial. Beyond direct technological investment, insurers must factor in ongoing operational costs associated with maintaining complex digital ecosystems, managing multi-party relationships, and continuously updating risk assessment mechanisms. These costs are not merely technological but strategic, requiring significant organisational transformation, staff training, and cultural adaptation to support new digital-first insurance distribution models.

Pro tip: Develop a comprehensive risk assessment framework that integrates technological, regulatory, and operational perspectives, enabling dynamic adaptation to emerging embedded insurance challenges.

Accelerate Your Embedded Insurance Journey with Seamless Core Platform Integration

Embedded insurance reshapes property and casualty distribution by demanding agile, API-driven systems that support rapid product launches, real-time underwriting and frictionless customer experiences. If you are facing challenges in integrating complex digital ecosystems, navigating regulatory compliance or reducing IT complexity, you need a core platform designed for the future of insurance.

Insurance Business Applications (IBA) offers IBSuite—a cloud-native, end-to-end insurance platform built to empower P&C insurers to streamline operations and embrace embedded insurance models with confidence. With modular architecture, seamless API connectivity and regulatory compliance baked in, IBSuite lets you innovate faster while delivering the seamless integrations and dynamic risk assessment highlighted in the article.

Ready to transform your P&C distribution with embedded insurance capabilities that truly add value for your customers and partners? Discover how IBSuite can help you achieve this today. Book a personalised demonstration to see how we can enable your digital transformation and accelerate embedded product innovation now at Book A Demo. Learn more about our cloud-native architecture and how IBSuite supports API-driven insurance frameworks to future-proof your business.

Frequently Asked Questions

What is embedded insurance?

Embedded insurance is a model where insurance products are seamlessly integrated into the purchase of goods or services, allowing consumers to acquire coverage at the point of sale, thus enhancing convenience and relevance.

How does embedded insurance differ from traditional insurance approaches?

Unlike traditional insurance, which often requires separate transactions for coverage, embedded insurance offers real-time activation of protection during purchase, simplifying the consumer experience and reducing complexity.

What are the key benefits of using embedded insurance?

The primary benefits of embedded insurance include frictionless user experiences, enhanced accessibility to protection, contextual relevance, and improved convenience for consumers when they need coverage the most.

What challenges do insurers face when implementing embedded insurance models?

Insurers encounter various challenges, including technological integration complexities, adherence to regulatory compliance, managing multiple partnerships, and the financial implications of maintaining sophisticated digital ecosystems.

Recommended

- 7 Types of P&C Insurance Distribution for Insurers

- Digital Distribution in Insurance: Driving P&C Innovation

- 2.0, 2.5, or 3.0? – Embedded Insurance Part 2 – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Embedded Insurance and its Importance: Part 1 – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- How to Lower Insurance Costs When Buying a Car | ReVroom