17.06.26

Why choose flexible insurance systems in 2026

Flexible insurance systems are technology platforms that externalise rating and pricing logic as metadata, allowing insurers to modify products, pricing, and coverage rules without rewriting code. The industry term for this approach is configuration-driven architecture, and it is rapidly replacing legacy policy administration stacks across European P&C markets. The core argument for why choose flexible insurance systems is straightforward: they compress product launch cycles from months to weeks, reduce IT dependency for routine changes, and maintain the governance trails that regulators demand. This article examines the technical foundations, business impacts, and practical implementation considerations for insurance executives ready to act.

Why choose flexible insurance systems over legacy stacks

The metadata-driven framework described in the RMA reference architecture published in May 2026 integrates configuration, execution, and audit visibility through API-driven microservices. That architecture matters because it decouples pricing logic from application code entirely. When a regulator mandates a tariff adjustment or a product team wants to add a new coverage endorsement, the change lives in configuration, not in a development sprint.

Traditional IT-led change cycles for product launches in legacy environments span 6–12 months. That timeline is not a technology limitation so much as a structural one: every change requires developer involvement, testing cycles, and deployment windows. Configuration-driven platforms break that dependency by treating product rules as data rather than code.

The benefits of flexible insurance systems extend beyond speed. Governance and auditability are preserved through immutable, timestamped logs that record every configuration change. Regulators can trace exactly which rule applied to which policy at which point in time. That traceability is not a feature added on top; it is built into the architecture from the start.

How metadata-driven architectures enable real agility

The technical foundation of a flexible insurance platform rests on three principles: externalised configuration, API-first integration, and lifecycle transparency.

Externalised configuration means that rating factors, underwriting rules, and product parameters are stored as structured metadata rather than hard-coded logic. A business analyst can update a flood excess threshold in a web interface, and the change propagates immediately to quoting, policy issuance, and claims assessment without a single line of code being touched.

API-first microservices allow rating, underwriting, and claims decisions to operate as independent services. Each module communicates through defined interfaces, so upgrading the rating engine does not require rebuilding the claims module. This is the architecture that makes true modularity possible.

Lifecycle transparency is delivered through immutable audit logs. Every configuration version is timestamped and traceable, which satisfies both internal governance requirements and external regulatory demands across European markets.

- Configuration changes deploy without redeployment of the core application

- API contracts between modules remain stable even as individual services evolve

- Audit logs capture who changed what, when, and why, supporting regulatory review

- Rollback capabilities allow rapid reversal of any configuration change that produces unexpected results

Pro Tip: When evaluating a flexible platform, ask the vendor to demonstrate a live configuration change from rule authoring through to a test quote. If that cycle takes more than 30 minutes, the platform is not as configuration-driven as the marketing suggests.

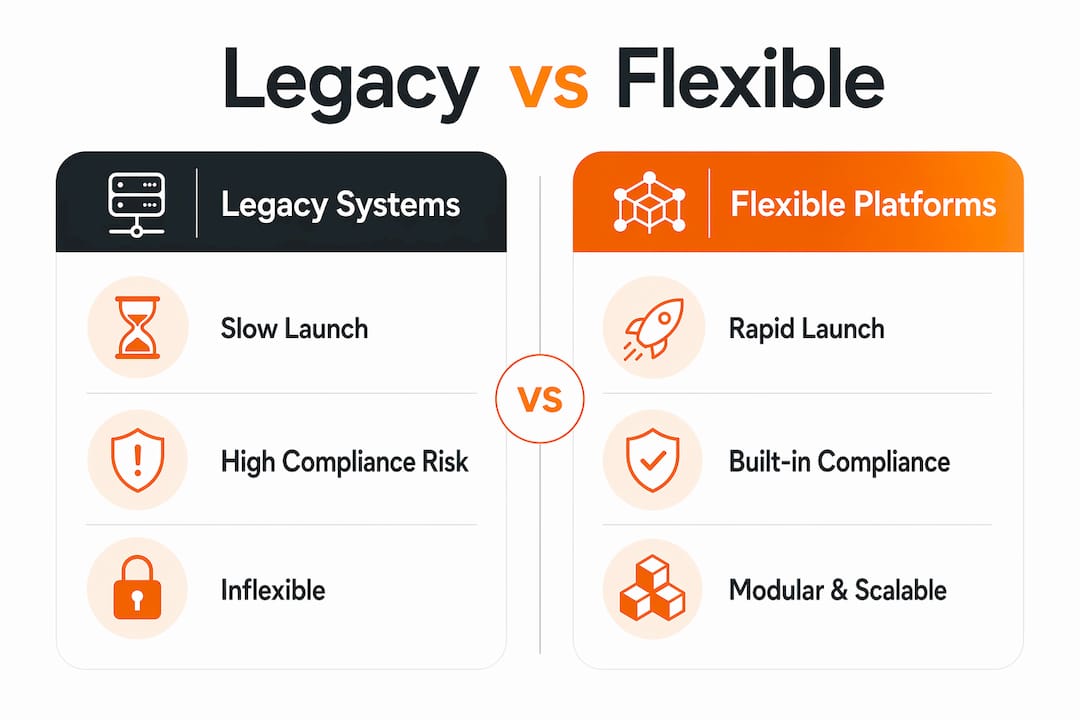

Legacy systems vs. flexible platforms: a direct comparison

The performance gap between legacy stacks and modern configuration-driven platforms is measurable. Product configuration cycles in legacy environments run 6–12 months; flexible configurators reduce that to 6 weeks to 3 months. That difference compounds over time: an insurer launching four products per year instead of one gains a structural competitive advantage that is very difficult to reverse.

| Dimension | Legacy Systems | Flexible Platforms |

|---|---|---|

| Product launch cycle | 6–12 months | 6 weeks to 3 months |

| Change ownership | IT development teams | Business analysts |

| Configuration method | Code changes and deployments | No-code rule authoring |

| Audit and traceability | Manual documentation | Automated, timestamped logs |

| Compliance workflow | Separate process | Embedded in configuration |

| Scaling individual modules | Full system involvement | Independent module scaling |

Duck Creek’s Agentic Product Configurator reports a 50% reduction in configuration effort, with timelines compressed from months to weeks. That figure reflects an AI-driven workflow spanning requirements generation, configuration, validation, and deployment, all with governance controls embedded throughout.

The compliance dimension is where legacy systems carry the most hidden cost. When a regulatory change arrives, a legacy insurer must open a development ticket, wait for prioritisation, build and test the change, and deploy it. A flexible platform insurer updates a configuration rule, validates it against test cases, and publishes. The difference in regulatory response time can be measured in weeks versus days.

Pro Tip: Do not evaluate flexible platforms solely on time-to-market claims. Ask specifically how compliance workflows and human-in-the-loop validation are handled within the configuration process. Governance is where many platforms fall short of their promises.

Modularity and scalability: tailoring coverage without rebuilding

Modular insurance platforms allow insurers to mix and match product components, including coverages, limits, and deductibles, without rebuilding entire product structures. That capability is the technical foundation for genuinely tailored insurance plans. A commercial lines insurer can offer a base property product and allow brokers to attach liability, business interruption, or cyber endorsements through configuration, not custom development.

The scalability argument is equally concrete. Modular architectures support independent scaling of individual components. During a claims surge following a weather event, the claims processing module can scale independently without touching the quoting or billing services. That operational efficiency is impossible in a monolithic legacy system where all components share the same infrastructure.

Integration of AI, machine learning, and IoT data feeds is also significantly simpler in a modular architecture. Each innovation connects to a specific module through a defined API rather than requiring a whole-system integration project. An insurer adding telematics-based pricing, for example, connects the telematics data feed to the rating module alone.

The customer experience benefit follows directly from this technical flexibility. When underwriters can configure tailored policies without IT involvement, response times to brokers and customers improve. Flexible underwriting rules allow more precise risk assessment, which means better pricing for lower-risk customers and more accurate premiums across the portfolio. You can explore what to look for in modern insurance platforms when assessing modularity in practice.

How to implement flexible insurance systems successfully

Successful adoption of a flexible insurance system depends on decisions made before a single module goes live. The most common failure mode is implementing a flexible rating engine while leaving downstream policy administration, billing, and claims systems code-bound. End-to-end configuration propagation is the defining requirement: if a product rule change does not flow automatically through to billing and claims, the time-to-market gains evaporate at the point of policy issuance.

Here are the implementation priorities that separate successful deployments from expensive partial ones:

- Map the full change path before selecting a platform. Identify every system that a product rule change must touch, from quoting through to financial reporting. Any system that requires a code change to reflect a configuration update is a bottleneck that will limit your agility.

- Define what stays in code and what becomes configurable. Not everything should be metadata. Core business logic that rarely changes and carries high risk if misconfigured should remain in code. Pricing factors, coverage rules, and product parameters are the right candidates for externalisation.

- Prioritise no-code rule authoring interfaces. The rule authoring interface is the single biggest predictor of long-term product velocity. Business analysts who can author and maintain rules without developer support sustain the pace of product innovation independently of IT capacity.

- Embed compliance workflows in the configuration process. Regulatory demands require traceability, rollback capabilities, and explainability. Human-in-the-loop validation controls should be a standard feature of the configurator, not a separate compliance layer added afterwards.

- Plan the integration with your existing policy administration system carefully. A phased approach that replaces one module at a time reduces risk and allows the organisation to build configuration capability incrementally.

Pro Tip: Involve your compliance and actuarial teams in the platform selection process from the start. The platforms that look most attractive to IT often lack the governance features that compliance teams require. Aligning both perspectives early prevents costly rework later.

For a practical view of how insurance product configurators operate in 2026, the Ibapplications content library provides detailed guidance on reducing implementation timelines and costs.

Key takeaways

Flexible insurance systems deliver competitive advantage only when configuration-driven architecture spans the full insurance value chain, not just the rating engine.

| Point | Details |

|---|---|

| Metadata-driven architecture | Externalising rating logic as metadata removes IT bottlenecks from routine product and pricing changes. |

| Time-to-market compression | Configuration-driven platforms reduce product launch cycles from 6–12 months to as little as 6 weeks. |

| No-code rule authoring | Business analysts who own rule authoring sustain product velocity independently of IT development capacity. |

| End-to-end integration | Configuration changes must propagate through policy admin, billing, and claims to deliver real agility gains. |

| Embedded governance | Audit trails, rollback capabilities, and human-in-the-loop controls are non-negotiable for regulatory compliance. |

The case for flexibility is stronger than most executives realise

Having worked closely with insurers navigating core system modernisation, I have observed a consistent pattern: the organisations that treat flexible architecture as a technology project consistently underperform those that treat it as a business capability. The distinction matters enormously.

When a product team can launch a new endorsement in three weeks without raising an IT ticket, the relationship between product and technology changes fundamentally. Product managers start thinking in terms of market experiments rather than annual roadmaps. That shift in thinking is where the real competitive advantage lives, and it is invisible in any vendor demonstration.

The uncomfortable truth about flexible insurance systems is that the technology is rarely the limiting factor. The limiting factor is almost always organisational. Insurers that have spent decades routing every product change through IT development teams have built processes, governance structures, and cultural expectations around that model. Introducing a no-code configurator does not automatically change those habits. The insurers I have seen extract the most value from flexible platforms are those that deliberately restructured their product and IT teams to take advantage of the new capability.

Investing in flexible systems also reduces technical debt in ways that are difficult to quantify upfront but become very visible over time. Every configuration change that does not require a code deployment is a change that does not add to the maintenance burden of the codebase. Over three to five years, that compounds into a significantly leaner and more maintainable system. The insurers still running monolithic legacy stacks are not just slower to market. They are spending an increasing proportion of their IT budget simply maintaining the status quo.

— Tuna

How ibsuite supports flexible, modular insurance operations

Ibapplications has built IBSuite specifically to address the configuration and agility challenges that European P&C insurers face. The policy administration module is designed as a modular, API-first component that allows product teams to configure coverages, rules, and pricing without IT involvement. Changes propagate through to billing, claims, and financial reporting automatically, which is the end-to-end integration that most platforms promise but few deliver consistently.

IBSuite’s claims management module scales independently, supports configurable workflows, and maintains full audit trails for regulatory purposes. For insurers evaluating a move away from legacy stacks, IBSuite offers a phased adoption path that reduces transition risk while delivering measurable agility improvements from the first module deployed.

FAQ

What is a flexible insurance system?

A flexible insurance system is a configuration-driven platform that stores rating, pricing, and product rules as metadata rather than hard-coded logic. This allows insurers to modify products and pricing without developer involvement or system redeployment.

How much faster can insurers launch products with flexible systems?

Configuration-driven platforms reduce product launch cycles from the 6–12 months typical of legacy systems to 6 weeks to 3 months. The reduction depends on the complexity of the product and the maturity of the insurer’s configuration capability.

How do flexible systems handle regulatory compliance?

Leading flexible platforms embed compliance workflows directly in the configuration process, including immutable audit logs, rollback capabilities, and human-in-the-loop validation. These controls satisfy European regulatory requirements for traceability and explainability without requiring separate compliance processes.

What is the biggest risk when implementing a flexible insurance system?

The most significant risk is implementing a flexible rating engine while leaving downstream systems code-bound. If policy administration, billing, or claims require code changes to reflect a configuration update, the time-to-market gains are lost at the point of policy issuance.

Can modular insurance platforms integrate with AI and IoT data?

Modular architectures connect AI, machine learning, and IoT data feeds to specific modules through defined APIs, making integration significantly more straightforward than whole-system projects. An insurer adding telematics pricing, for example, connects the data feed to the rating module alone without affecting other services.

Recommended

- Modern Insurance Platform Benefits – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Embracing Compliance through Next-Generation Insurance Platforms – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Why Modernizing Insurance Systems is Crucial for Growth – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Future-Proofing Insurance: – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System