16.10.25

Digital Underwriting Workflow Guide for Seamless Automation

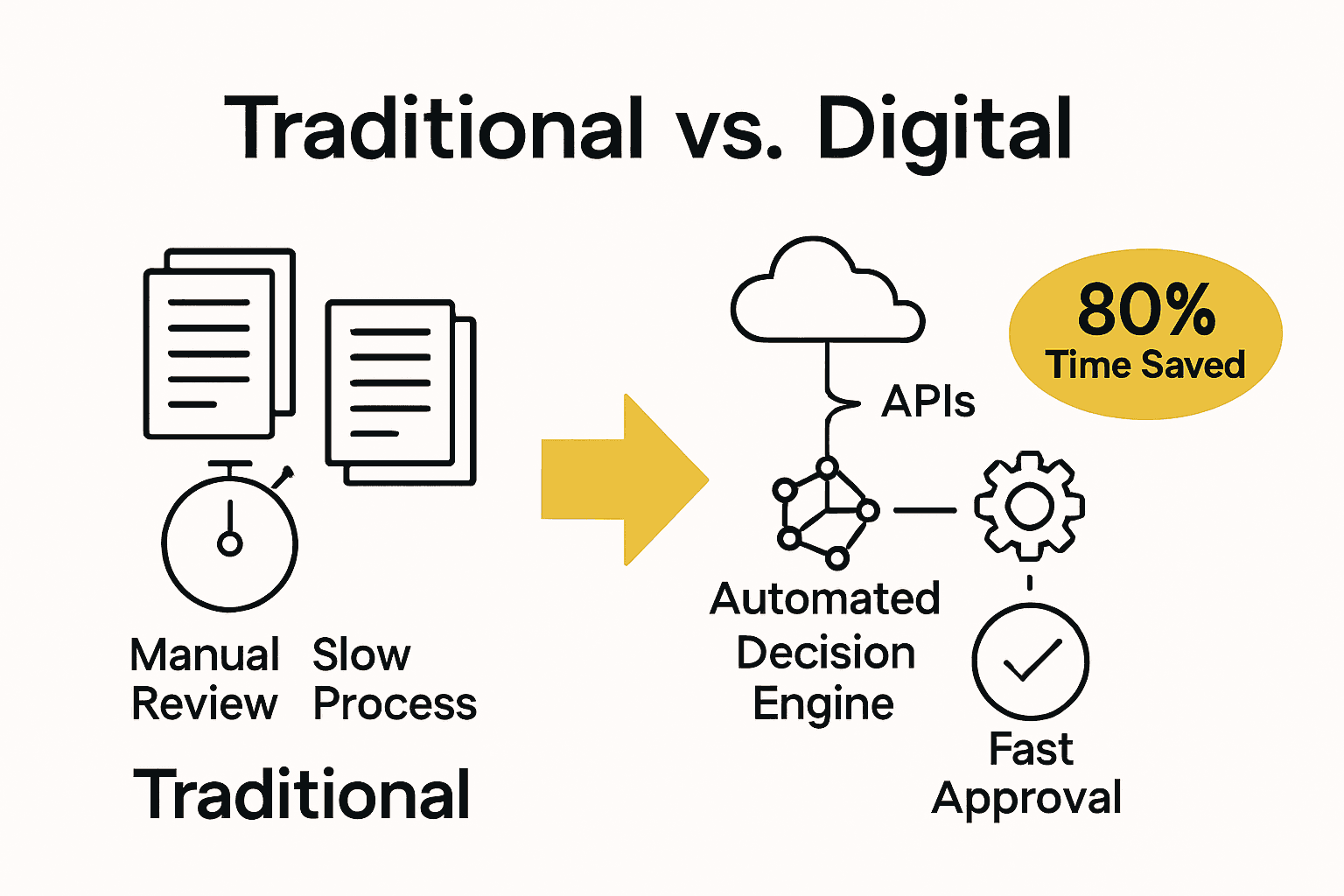

Did you know that over 60 percent of insurers say poor data integration is their biggest barrier to digital underwriting? As precision and speed become vital in risk assessment, the quality and flow of your information can turn the underwriting process into a powerful business advantage. This guide walks you through each step to help you transform scattered data and outdated workflows into a connected, intelligent, and compliant digital underwriting operation.

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Map All Data Sources | Create an inventory of all internal and external data sources to enhance underwriting accuracy and efficiency. |

| 2. Automate Decision Workflows | Use intelligent automation to streamline decision-making processes and reduce manual interventions, ensuring consistent risk evaluations. |

| 3. Prioritize Real-Time Data | Focus on integrating data sources that offer verified real-time information for more reliable risk assessments and compliance. |

| 4. Implement Robust API Integrations | Connect to external sources through APIs to enable seamless data flow and enrich risk assessment capabilities effectively. |

| 5. Rigorously Test Automation Systems | Conduct comprehensive testing of automated workflows to verify accuracy and performance against established benchmarks. |

Table of Contents

- Step 1: Assess Underwriting Requirements And Data Sources

- Step 2: Configure Digital Workflows In Your Insurance Platform

- Step 3: Integrate Apis And Connect External Systems

- Step 4: Automate Decision Rules And Validation Processes

- Step 5: Test And Verify Workflow Performance And Accuracy

Step 1: Assess underwriting requirements and data sources

Getting your digital underwriting workflow right starts with knowing exactly what data you need and where to find it. This step is about creating a comprehensive map of your information landscape that will power intelligent risk assessment and decision making.

Begin by conducting a thorough inventory of all potential data sources relevant to your underwriting process. These typically include internal systems like policy administration platforms, claims databases, and customer relationship management tools. External sources are equally critical. Think about credit reporting agencies, motor vehicle records, property information registries, and specialized insurance databases that offer granular risk insights.

The goal is to create a holistic view of data availability. Make a detailed spreadsheet tracking each potential data source and categorize them based on key attributes like data type (personal information, financial records, property details), update frequency, reliability score, and integration complexity. This systematic approach helps you understand what information you currently have access to and what gaps exist in your data collection strategy.

Here’s a summary of common underwriting data sources and their key attributes:

| Data Source Type | Example Systems | Update Frequency | Integration Complexity |

|---|---|---|---|

| Internal | Policy admin Claims databases CRM tools |

Real-time Daily Weekly |

Low to Medium |

| External | Credit bureaus Property registries Insurance databases |

Real-time Monthly Ad hoc |

Medium to High |

| Regulatory | Compliance databases Government records |

Periodic Annually |

High |

Pro Tip: Not all data is created equal. Prioritize sources that provide verified, real time information and have robust data governance practices.

Consider working closely with your IT and data architecture teams to assess technical integration capabilities. Modern underwriting platforms can streamline data collection by offering API connectors and automated data retrieval mechanisms. These tools can significantly reduce manual data entry and minimize potential errors.

Don’t forget to evaluate data privacy and compliance requirements during this assessment. Different jurisdictions have varying regulations about data collection and usage in insurance underwriting. Ensure your data sources and collection methods meet all legal standards.

Once you have mapped your data ecosystem, you will be ready to design workflow automation that transforms raw information into actionable underwriting intelligence. The next step involves selecting the right technologies to process and analyze these diverse data streams efficiently.

Step 2: Configure digital workflows in your insurance platform

Now that you have mapped your data sources, it is time to transform those insights into seamless digital workflows that drive efficiency and accuracy in your underwriting process. This step is about designing intelligent automation that turns raw data into actionable risk assessments.

Start by breaking down your current underwriting workflow into discrete steps and decision points. Identify where manual interventions currently slow down processing and where automation can create significant improvements. Modern insurance platforms allow you to create customized workflow rules that automatically route information, trigger specific actions, and make preliminary risk assessments based on predefined parameters.

Your workflow configuration should focus on creating intelligent decision trees that can handle different scenario types. For instance, you might design workflows that automatically approve low risk policies, flag complex cases for manual review, and route high risk applications through additional verification processes. This approach ensures consistent decision making while freeing up underwriting talent to focus on more nuanced risk evaluations.

Pro Tip: Build flexibility into your workflows. Insurance markets change rapidly, and your digital processes should adapt quickly without requiring extensive reprogramming.

Digital insurance platforms offer powerful workflow configuration tools that allow granular control over process automation. Look for solutions that provide visual workflow designers, allowing you to map processes through intuitive drag and drop interfaces. These tools enable non technical team members to understand and modify workflow logic without deep programming knowledge.

Consider implementing machine learning algorithms that can continuously improve workflow performance by analyzing past decisions and identifying optimization opportunities. These intelligent systems learn from historical data, gradually refining risk assessment criteria and reducing manual intervention over time.

As you configure these workflows, maintain a strong focus on compliance and auditability. Ensure that each automated step creates clear documentation trails and can demonstrate adherence to regulatory requirements. Your digital workflows should not just be efficient they must also be transparent and defensible.

With your workflows configured, you will be ready to test and refine your automation strategy.

The next phase involves pilot testing and gradually expanding your digital underwriting capabilities across different product lines and risk segments.

Step 3: Integrate APIs and connect external systems

With your workflows designed, the next critical phase is connecting your digital underwriting platform with external data sources through robust API integrations. This step transforms your system from a standalone tool into a powerful interconnected ecosystem that can gather real time information from multiple providers.

Start by identifying the specific APIs you need based on the data sources mapped in your earlier assessment. Look for APIs from credit bureaus, property registries, vehicle databases, and industry specific information providers. Each API connection represents a potential channel for enriching your risk assessment capabilities.

Prioritize APIs that offer standardized data formats and secure transmission protocols. Modern insurance platforms typically support REST and GraphQL API architectures which provide flexible data retrieval mechanisms. Your technical team should evaluate each API connection for reliability speed and compatibility with your existing infrastructure.

Pro Tip: Always implement robust authentication and encryption protocols when connecting external APIs to protect sensitive information.

Learn strategic approaches to leveraging insurance industry APIs that can dramatically improve your underwriting efficiency. Consider developing a phased integration strategy where you start with mission critical data sources and gradually expand your API ecosystem.

Each API integration requires careful configuration. Work with your development team to establish secure authentication methods like OAuth 2.0 or API keys. Create middleware layers that can translate incoming data into standardized formats your underwriting workflows can easily process. This abstraction layer helps manage complexity and allows easier future modifications.

Test each API connection rigorously before full deployment. Simulate various data retrieval scenarios to ensure consistent performance and validate that information flows seamlessly through your configured workflows. Pay special attention to error handling mechanisms that can gracefully manage situations where external systems are unavailable or return unexpected data formats.

As you complete these integrations your digital underwriting platform will transform into an intelligent adaptive system capable of drawing insights from diverse external sources. The next step involves implementing monitoring and optimization strategies to continuously refine your API connections and data retrieval processes.

Step 4: Automate decision rules and validation processes

With your data sources connected and workflows mapped, the next pivotal phase is creating intelligent automated decision rules that transform raw information into precise risk assessments. This step is about designing a sophisticated system that can make consistent nuanced decisions without constant human intervention.

Begin by documenting your current underwriting decision criteria in granular detail. What specific parameters determine policy approval risk scoring and pricing? Traditional manual processes often rely on complex judgment but digital systems require explicit rule definitions. Work closely with your most experienced underwriters to translate their decision making expertise into clear logical statements that can be programmed into your automation framework.

Your decision rules should create multiple evaluation paths based on risk complexity. Some applications might receive instant automated approval while others get routed for additional review. Design nested conditional logic that can handle increasingly intricate scenarios progressively escalating complexity and human oversight as risk indicators become more nuanced.

Pro Tip: Create rule sets with built in flexibility allowing periodic recalibration without complete system redesign.

Explore advanced approaches to automation in property and casualty insurance that can dramatically improve decision making precision. Focus on developing rule hierarchies that combine statistical modeling with domain specific expertise.

Implement validation checkpoints within your automated decision processes. These mechanisms verify data integrity cross reference multiple information sources and flag potential anomalies before final risk assessment. Machine learning algorithms can continuously refine these validation rules by analyzing historical decision outcomes and identifying subtle pattern variations.

Consider developing a scoring mechanism that assigns confidence levels to automated decisions. This approach provides transparency about the system’s certainty and creates natural intervention points for human review when algorithmic confidence falls below predetermined thresholds.

Ensure your automated decision rules maintain strict compliance with regulatory requirements. Document each decision pathway create clear audit trails and design systems that can explain their reasoning transparent and defensible manner. The goal is creating an intelligent system that augments human expertise rather than completely replacing professional judgment.

With your decision rules configured your digital underwriting platform becomes a sophisticated risk assessment engine. The next phase involves comprehensive testing and gradual implementation to validate and refine your automation strategy.

Step 5: Test and verify workflow performance and accuracy

With your digital underwriting workflow configured, the critical next phase is rigorous testing and verification to ensure your automated system delivers consistent accurate results. This step transforms your theoretical design into a reliable operational platform that can confidently handle real world insurance scenarios.

Initiate your testing strategy with a comprehensive simulation approach. Create a diverse test dataset representing multiple risk profiles scenarios and edge cases that mirror your actual underwriting environment. Use historical data from previous manual underwriting processes as a benchmark to validate your automated workflow performance. This means reconstructing past decisions and comparing them against your new algorithmic assessments to identify potential discrepancies or improvement areas.

Develop multiple testing layers that progressively validate different aspects of your workflow. Start with unit testing individual rule sets and decision logic components. Then move to integrated testing where you evaluate how different system modules interact. Finally conduct end to end workflow simulations that replicate complete underwriting processes from initial application to final risk assessment.

Pro Tip: Create a shadow mode testing environment where your new automated system runs parallel to existing manual processes without actually making live decisions.

Learn strategic approaches to insurance process optimization that can help you design more robust testing protocols. Focus on creating scenarios that challenge your system decision making capabilities and expose potential weaknesses.

Implement precise performance metrics to objectively measure workflow effectiveness. Track key indicators like decision accuracy rate processing speed consistency of risk assessment and comparative performance against manual underwriting benchmarks. Use statistical analysis to identify subtle variations and continuous improvement opportunities.

Pay special attention to your systems error handling and exception management capabilities. Design test scenarios that intentionally introduce data anomalies incomplete information and unexpected inputs to verify how your workflow responds. A robust automated system should gracefully manage uncertainties without breaking down or producing unreliable results.

Establish a continuous feedback loop that allows ongoing performance refinement. Create mechanisms for capturing and analyzing system performance data documenting any discrepancies and systematically updating your decision rules and validation processes.

As you complete this testing phase your digital underwriting platform will transition from a theoretical concept to a validated operational tool. The next stage involves gradual implementation and monitoring to ensure seamless real world performance.

Ready to Streamline Your Digital Underwriting Workflow?

Automating underwriting workflows sounds promising, but transforming complex processes into seamless, accurate, and auditable automation is challenging. You face hurdles with fragmented data sources, manual interventions, integration headaches, and compliance worries. The article breaks down how mapping data, configuring workflows, and connecting APIs can help—but putting these steps into action without the right technology can stall your progress or limit your impact.

What if you could automate underwriting with a proven, cloud-native insurance platform that supports every step mentioned? Insurance Business Applications (IBA) delivers with IBSuite, empowering you to automate risk assessment and workflow rules, integrate data sources effortlessly, and manage compliance—all out of the box. Leading insurers trust IBA to accelerate digital transformation and launch products faster.

See how IBSuite streamlines sales and underwriting with powerful API-first capabilities and flexible workflow design. Ready to move from theory to seamless automation? Book a demo today and experience a smarter way to modernize your underwriting. Your automated future starts with IBA. Learn more at ibapplications.com/book-a-demo.

Frequently Asked Questions

What data sources should I assess for digital underwriting?

To effectively implement a digital underwriting workflow, assess both internal systems like policy administration platforms and external data sources such as credit reporting agencies and property registries. Start by creating a comprehensive inventory that categorizes each source based on data type, update frequency, and reliability. This will ensure you have a complete understanding of your data landscape.

How can I configure workflows in my digital underwriting platform?

Begin by breaking down your existing underwriting process into distinct steps and identifying automation opportunities that could enhance efficiency. Use visual workflow tools to establish rules that route information and automate decision-making based on risk parameters. Aim to improve processing speeds by at least 30% by minimizing manual interventions.

What are the best practices for integrating external APIs in underwriting?

Prioritize incorporating APIs that provide reliable data formats and secure transmission methods. Start by identifying necessary APIs based on your mapped data sources and gradually expand your connections. Implement testing protocols to ensure integrations function smoothly and assess their impact on the overall underwriting performance within 60 days.

How can I create automated decision rules for underwriting workflows?

Document your underwriting criteria and translate them into clear decision rules that can be integrated into your automated system. Use conditional logic to categorize applications by complexity, allowing for instant approvals or flagging complex cases for further review. This structured approach can reduce human decision-making time by about 20%.

How do I test and verify the performance of my automated underwriting system?

Conduct thorough testing using varied scenarios that include multiple risk profiles to validate your automated processes. Implement unit testing for individual components followed by integrated and end-to-end testing. Aim to achieve a decision accuracy rate of over 90% compared to prior manual benchmarks before full deployment.

What should I consider regarding compliance in my digital underwriting workflows?

Ensure that your automated processes adhere to relevant regulatory requirements by documenting each decision pathway and maintaining clear audit trails. Regularly review your workflows for compliance and incorporate flexible systems that allow for updates as regulations change. This compliance focus can help mitigate potential legal risks.

Recommended

- Automation and Artificial Intelligence in P&C Insurance – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- 7 Steps to a Successful Insurance Process Checklist – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Claims Automation Step by Step: Enhance Processing Efficiency – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Insurance Digital Transformation Guide for Effective Change – Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System

- Understanding the Benefits of DM Automation

- Digital Payment Experience: Key Strategies and Future Trends